GSR Weekly Update - April 27th, 2026

S&P 500: 7,165.08 (+9.3%) | Gold: $4,740.90 (+6.9%) | DXY: 27.48 (-0.6%)

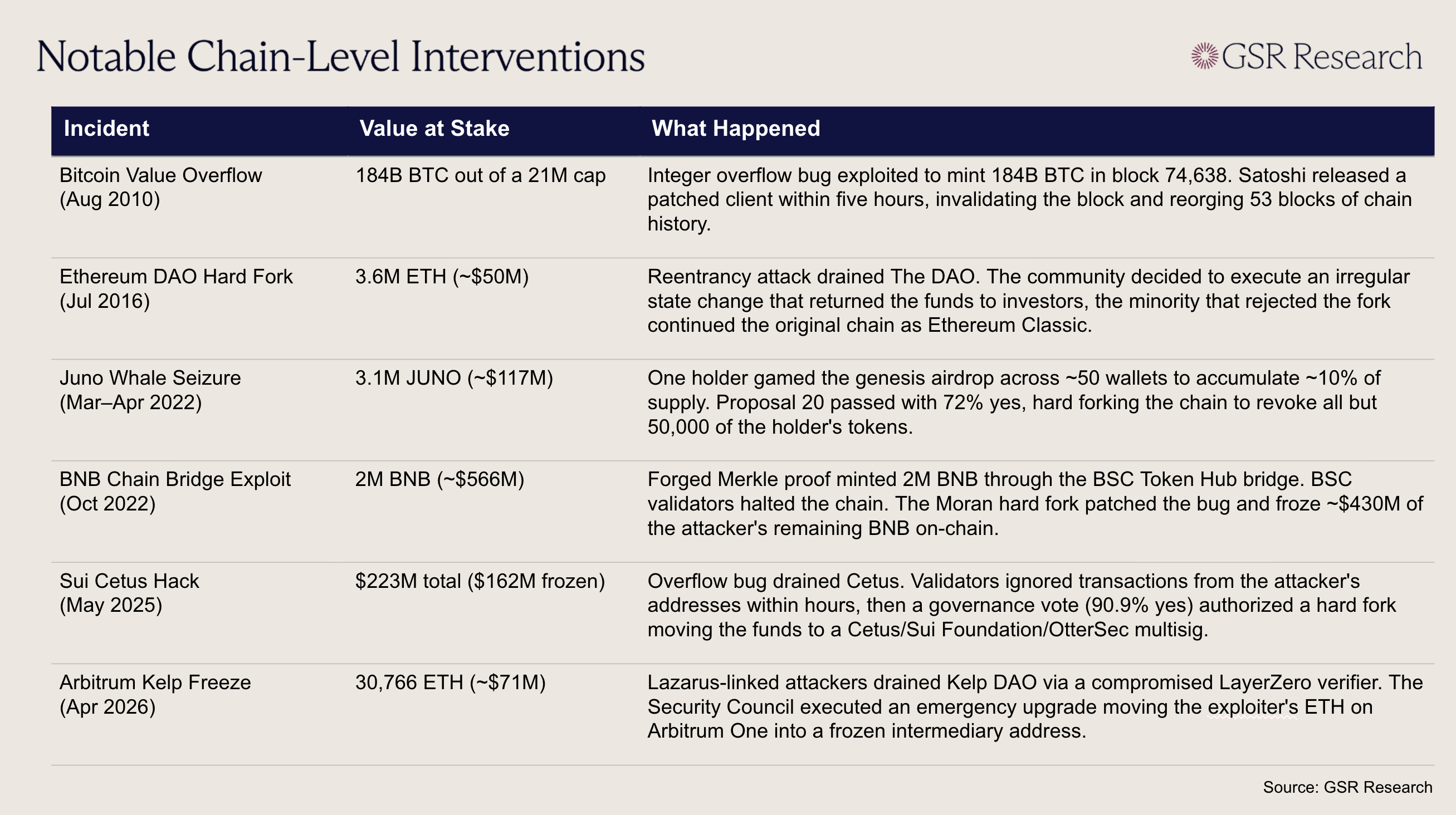

On April 21, Arbitrum's Security Council executed an emergency upgrade that moved 30,766 ETH (~$71 million) out of an Arbitrum One wallet linked to the Kelp DAO exploiter and into a frozen intermediary address. The wallet held the largest piece of stolen value still sitting onchain after attackers tied to North Korea's Lazarus Group minted 116,500 unbacked rsETH through a compromised LayerZero verifier on April 18. The freeze claws back roughly a quarter of the $292 million drained from Kelp, and is the first time a major L2 has used its emergency powers to reach into a user wallet at the protocol layer, with implications going far beyond the dollar figure recovered.

While there are numerous implications around Arbitrum’s actions, the mechanics of the freeze were straightforward. Arbitrum's 12-member Security Council holds emergency upgrade rights over the chain's contracts and can push changes without the standard delay. After receiving law enforcement input on the exploiter's identity, the council executed an upgrade that altered the state of the targeted address and routed its balance into a neutral wallet. No other accounts were touched and any further movement of the funds will necessitate a governance vote.

While token-level freezes by Circle and Tether happen all the time, Arbitrum’s actions were at the chain layer, upgrading the rollup itself rather than asking an issuer to blacklist a contract address. It’s worth pointing out that this is not a hidden capability. Arbitrum is currently a Stage 1 rollup, where the Security Council retains override authority. Every major L2 has the same capability, a metric which is openly tracked by L2Beat. Stage 2 would limit the council to intervening in the event of soundness errors only, and no rollup with meaningful TVL has reached that bar.

While the Security Council acted within its authority, their actions did not come without some controversy. The freeze violates the principles of self-custody, credible neutrality, immutability, and censorship resistance that are foundational claims of public blockchains. Once a chain demonstrates both the willingness and the capability to override state, the threat model for every wallet on it has changed. Each precedent of discretionary intervention, however sympathetic the facts, erodes the strong property rights that crypto systems promise. Even a justified freeze may push users to reassess what neutrality means on an L2.

That critique is understandable, however, the Security Council’s move has largely been applauded by the industry. Letting a state-sponsored actor walk off with $71 million of stolen funds, or pretending the Security Council did not exist, would not have made Arbitrum more decentralized. The capability was publicly documented, the council is elected, and any release of the frozen ETH still requires a DAO vote. Using that capability transparently is more honest than maintaining a fiction of neutrality that was never truly present.

Ultimately, not every execution environment has to make the same tradeoffs. Rather than ideologically pressuring every blockchain to hew closely to the same cypherpunk ideals, mass adoption is more likely with a diversity of chains that choose different points in the spectrum between full immutability and discretionary intervention. Users can then opt into the type of environment they prefer. Credibly-neutral settlement remains available on Ethereum L1 and, eventually, on Stage 2 rollups, where the Security Council's reach is reduced to bug fixes only. A healthy ecosystem benefits from giving users a real choice about where they want to sit on it.

Polymarket and Kalshi, the two most dominant prediction market platforms, each announced plans to launch perpetuals within hours of each other last week. Bloomberg first reported that Kalshi planned to launch perps on the morning of the 18th, while Polymarket teased its own perp product directly on X just hours later. Kalshi and Polymarket have often used similar go to market strategies as they inevitably fight over the same target userbase, yet their dual announcements within hours of each other seemed coincidental at best. While the timing was notable, the bigger story is what comes next: these launches will mark the first time a platform brings regulated perpetual futures to market in the United States.

Coinbase spent years navigating legislative hurdles and judicial challenges in an attempt to offer regulated perpetuals domestically and compete with offshore giants like Binance. After realizing that the path to domestic approval would be long and arduous, Coinbase flipped their focus internationally, launching Coinbase International Exchange in May of 2023. This allowed all of their non-U.S. traders to access standard perpetual contract trading, but Coinbase saw limited success as international perps were a market already saturated by every major offshore exchange. Even after securing FCM approval, Coinbase would still have to rely on an awkward workaround, using CFTC self-certification to launch “perpetual-style” futures for U.S. users in July 2025. While these contracts use hourly funding and trade 24/7, they still carry five-year expirations and remain hampered by restrictive leverage caps that fall far short of the multiples common on global platforms.

Polymarket and Kalshi’s launches will come during a much friendlier policy window, yet they have had their fair share of regulatory struggles themselves. Kalshi spent most of 2023 and 2024 fighting the CFTC over election contracts, and is currently battling multiple states over cease and desist orders. Polymarket paid a $1.4 million penalty to the CFTC in 2022 for operating an unregistered binary-options platform, and was temporarily forced offshore before finding its way back into the U.S. through a $112M derivatives exchange and clearinghouse acquisition. At that time Kalshi was already operating as a CFTC-designated contract market and later won permission in January 2025 to offer intermediated futures trading.

The CFTC did not open a formal public consultation on perpetual contracts until April 2025. However in March 2026, Chairman Michael Selig stated that a U.S. framework for crypto perps was coming "in the very near future." While a definitive federal rule is yet to be codified, Polymarket and Kalshi’s launch announcements are seemingly in anticipation of positive regulatory news. Polymarket’s perp announcement was undated, but an X post from Kalshi earlier in the month suggests that the platform would be launching “timeless” perpetuals this Monday, April 27th.

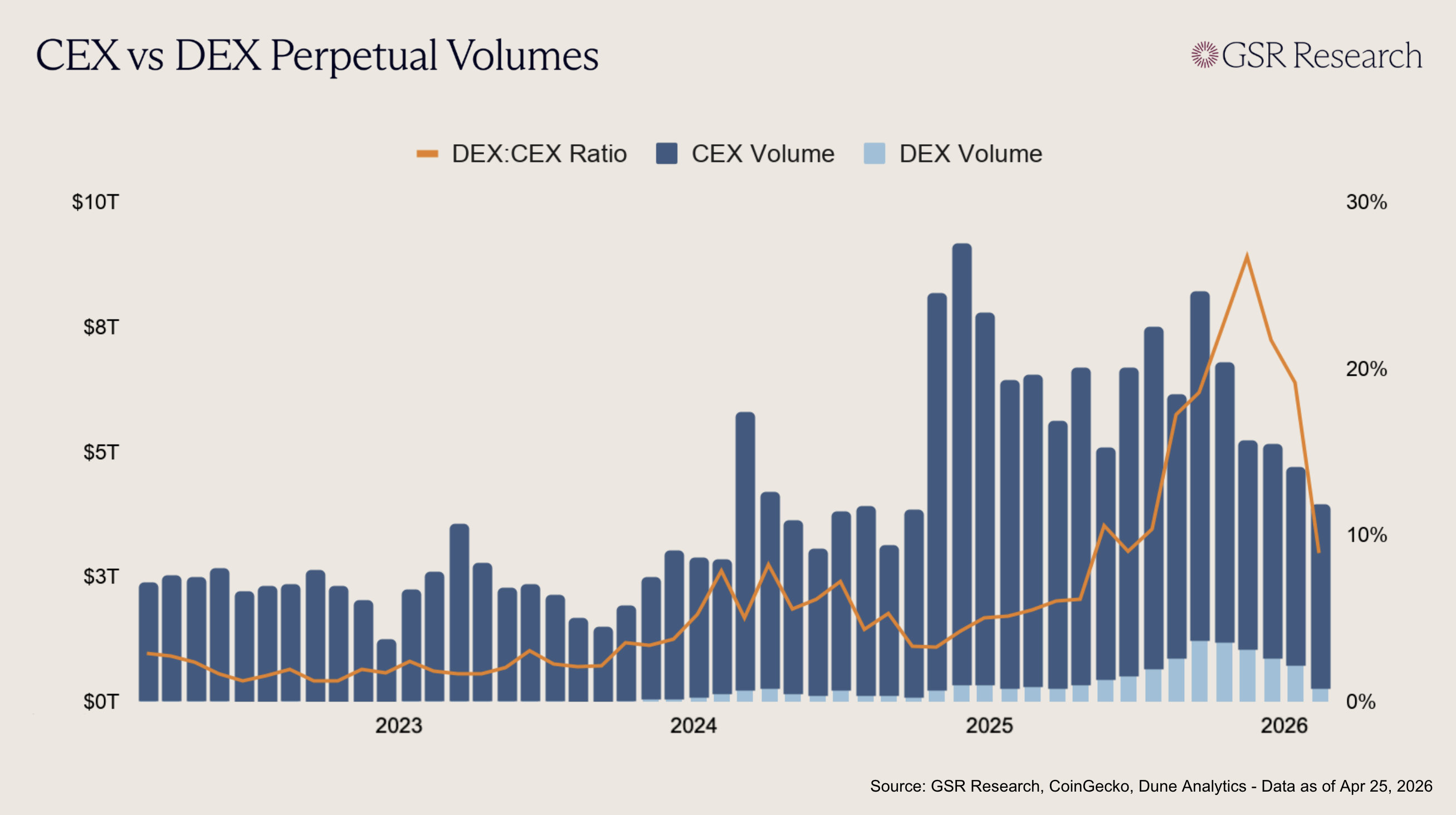

Kalshi and Polymarket are entering perps in the pivotal moment of a larger fight between centralized and decentralized exchanges. While centralized exchanges have dominated perpetual futures ever since their creation by BitMEX in 2016, decentralized platforms have recently been acquiring a higher percentage of total volume, particularly since the launch of Hyperliquid in November 2024. In the year following Hyperliquid’s launch in November 2024, decentralized exchanges would go from doing less than 4% to over 25% of CEX volumes. Decentralized volumes peaked during late 2025 due to attention around token launches for major DEXs like Aster and Lighter, but have since been in a downward trend, with the ratio now sitting under 10% once again. Decentralized exchanges mounted a formidable challenge to the centralized behemoths like Binance, but with volumes crashing post-TGE, their long-term viability is being questioned once again. Now, with the launch of Polymarket and Kalshi perps, as well as Hyperliquid’s upcoming HIP-4 deployment, full-stack CEXs and DEXs will once again compete for the same target userbase. The defining conflict of the next era will be the race between centralized and decentralized exchanges to build the first true "Super-App" of finance.

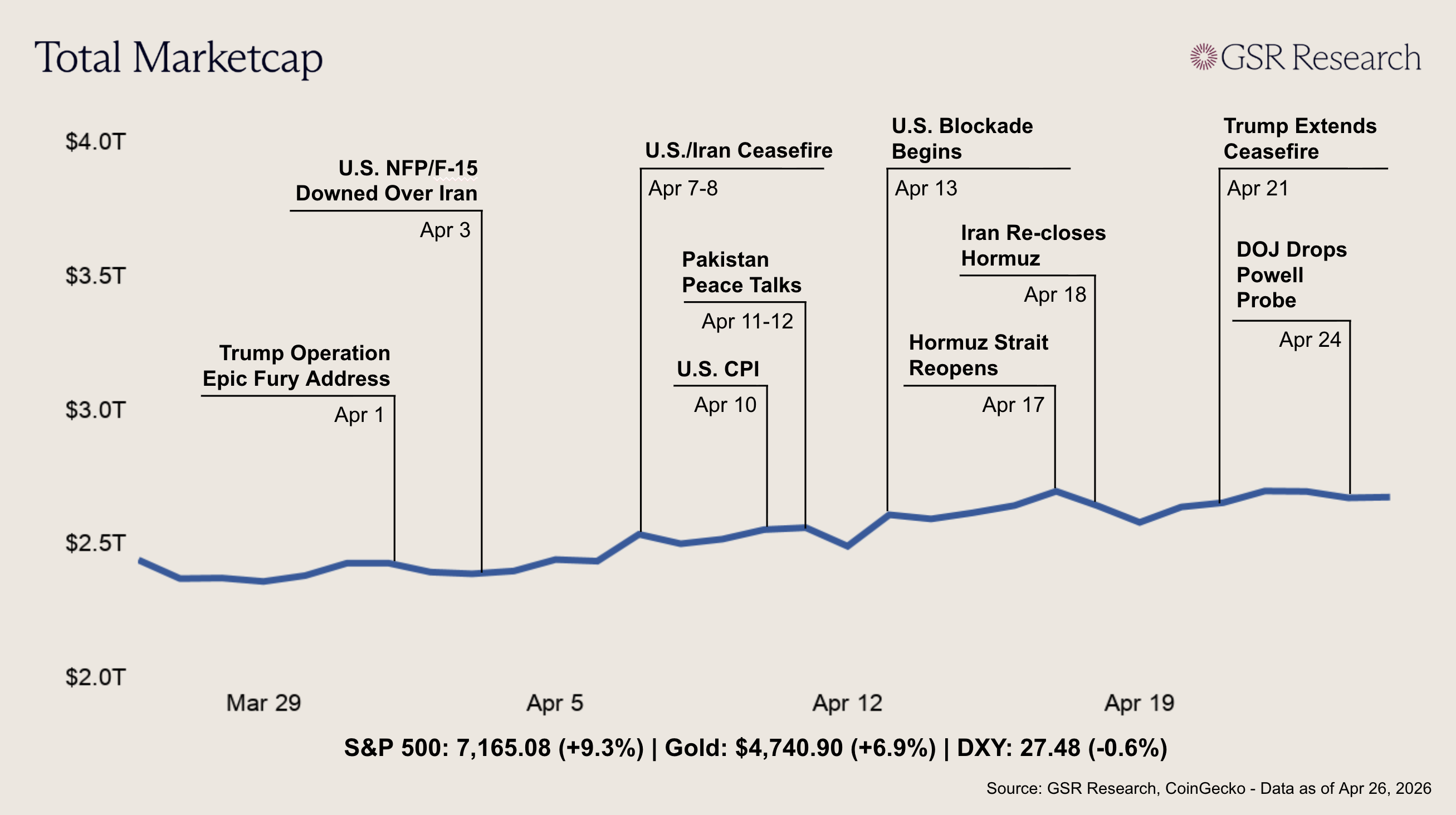

Crypto markets and equities both rallied to multi-month highs after Trump's indefinite extension of the U.S.-Iran ceasefire, holding most of those gains even as peace talks crumbled again over the weekend. The total crypto market cap opened near $2.55T with BTC around $75,300 as the U.S. naval blockade of Iranian ports remained in place. March retail sales released Tuesday came in at +1.7% MoM, the largest gain in over three years, though most of the strength came from a 15.5% jump in gas station sales. Sentiment turned decisively Tuesday evening when President Trump posted on Truth Social that he would extend the U.S.-Iran ceasefire indefinitely, citing Tehran's "seriously fractured" government and a request from Pakistani mediators. Risk assets gapped higher Wednesday: BTC pushed to an intraday high near $79,500, its strongest level since January 31, while the S&P 500 closed at a record 7,138 (+1.05%) and the Nasdaq at a record 24,658 (+1.64%). Strategy disclosed a $2.54B BTC buy, its largest since 2024, lifting its holdings to 815,061 BTC.

The rally cooled briefly Thursday after reports that Iran's parliament speaker had resigned from the negotiating team pushed Brent back above $105. Friday brought the week's most consequential procedural development: U.S. Attorney Jeanine Pirro abandoned the DOJ's criminal probe of Fed Chair Powell, removing the precondition Senator Tillis had set for advancing Kevin Warsh's confirmation. A blowout Intel earnings report (+24%) carried the S&P 500 and Nasdaq to fresh closing records of 7,165 and 24,837. Iran-related friction returned over the weekend after Trump cancelled an envoy trip to Pakistan and Iranian FM Araghchi left Islamabad without meeting U.S. officials, sending Brent to $107 by Sunday. BTC nonetheless held its gains, tagging $79,500 again early Monday before failing at $80,000 and easing back to $77,800. Focus now turns to Wednesday's FOMC decision, Big Tech earnings, and Thursday's Q1 GDP and PCE prints.

U.S. spot Bitcoin ETFs continued to attract consistent demand, with multiple strong inflow days punctuating the week. After a solid start on Apr 20 (+$238M), flows briefly softened on Apr 21 (+$12M) before re-accelerating midweek (+$336M on Apr 22 and +$223M on Apr 23). Even the weaker Friday print (+$14M on Apr 24) held in positive territory, highlighting persistent institutional allocation despite the day-to-day volatility.

Ether ETFs extended their recent recovery but showed more fragility and variance across sessions. The week opened with solid inflows (+$68M on Apr 20 and +$43M on Apr 21), followed by a strong midweek print (+$96M on Apr 22). However, this momentum was interrupted by a sharp outflow on Apr 23 (-$76M), before partially stabilizing into the end of the week (+$23M on Apr 24). While the aggregate trend remains positive, the choppier profile relative to BTC suggests that ETH demand is still more tactical and less consistent, with flows more sensitive to short-term positioning shifts.

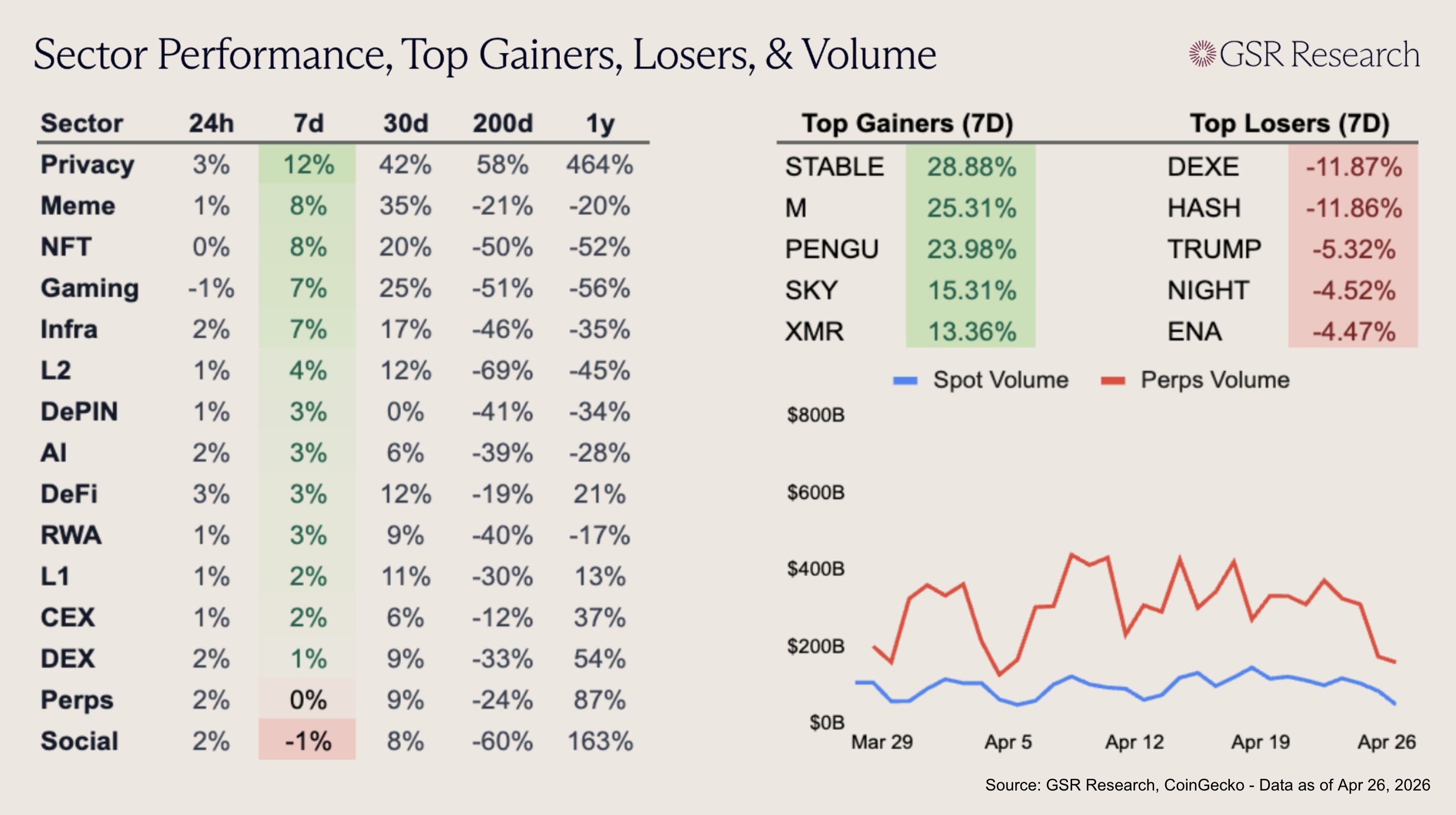

Privacy is the top performing sector on the week, up 12% due to rallies in Monero (+13.36%) and Zcash (+10.4%). Zcash rallied after the privacy-focused L1 secured a Robinhood listing on the 23rd, while Monero surged following the "MoneroRun 2026" community audit, which triggered a supply squeeze as users withdrew their XMR from centralized exchanges into self-custody to celebrate the protocol’s 12th anniversary. The meme, NFT, and gaming sectors have also outperformed on 7d and 30d timelines, defying the perception that their respective narratives have cooled.

Perps traded flat on the week following news of Kalshi and Polymarket’s entrances to the sector. While perpetual exchange tokens remain top performers on the 1y and 200d timelines, recent performance has suffered after several high-profile TGEs lead to the departure of mercenary capital and a subsequent drop in trading volume.

Download the PDF of the full report here.

This material is provided by GSR (the “Firm”) solely for informational purposes. It is not intended to be advice or a recommendation to buy, sell or hold any investment mentioned. Investors should form their own views in relation to any proposed investment.

It is intended only for sophisticated, institutional investors and does not constitute an offer or commitment, a solicitation of an offer or commitment, or any advice or recommendation, to enter into or conclude any transaction (whether on the terms shown or otherwise), or to provide investment services in any state or country where such an offer or solicitation or provision would be illegal. The Firm is not and does not act as an advisor or fiduciary in providing this material.

This material is not an independent research report, and has not been prepared in accordance with any legal requirements by any regulator (including the FCA, FINRA or CFTC) designed to promote the independence of investment research.

This material is not independent of the Firm’s proprietary interests, which may conflict with the interests of any counterparty of the Firm. The Firm may trade investments discussed in this material for its own account, may trade contrary to the views expressed in this material, and may have positions in other related instruments. The Firm is not subject to any prohibition on dealing ahead of the dissemination of this material.

Information contained herein is based on sources considered to be reliable, but is not guaranteed to be accurate or complete. Any opinions or estimates expressed herein reflect a judgment made by the author(s) as of the date of publication, and are subject to change without notice. The Firm does not plan to update this information.

Trading and investing in digital assets involves significant risks including price volatility and illiquidity and may not be suitable for all investors. The Firm is not liable whatsoever for any direct or consequential loss arising from the use of this material. Copyright of this material belongs to GSR. Neither this material nor any copy thereof may be taken, reproduced or redistributed, directly or indirectly, without prior written permission of GSR.

Please see here for additional Regulatory Legal Notices relevant to US, UK and Singapore.