GSR Weekly Update - June 15th, 2026

BTC: $64,117 (+3.6%) | ETH: $1,666 (+2.4%) | BTC Dom: 56.6% | Global Cap: $2.27T

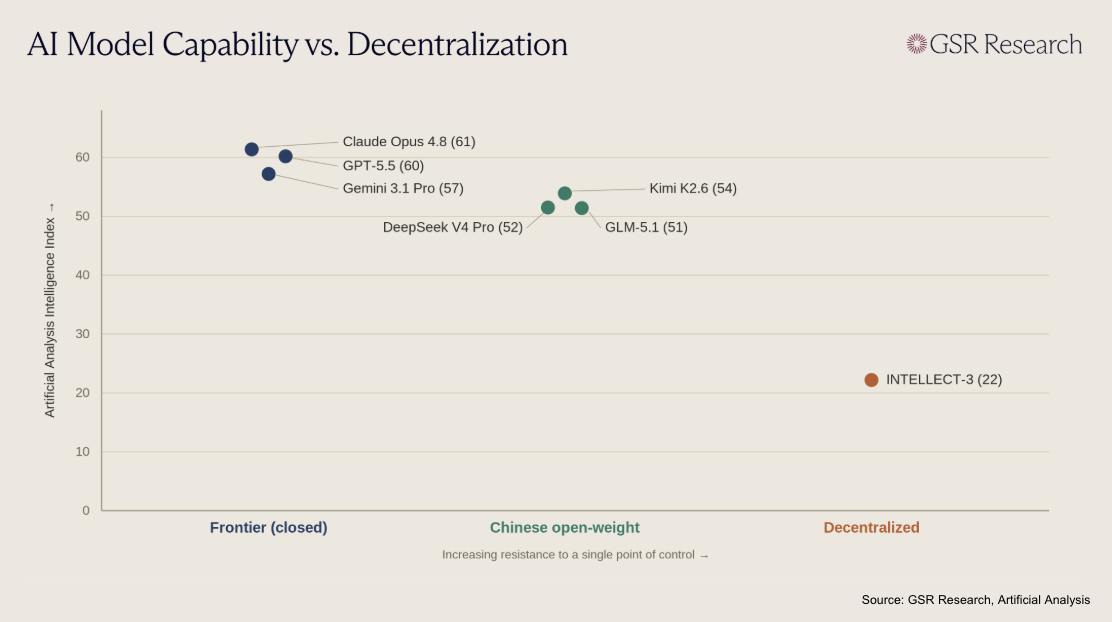

On June 12, Anthropic disabled its two most capable models, Fable 5 and Mythos 5, for every customer worldwide. Earlier that afternoon, US authorities had issued an export control directive that, citing national security, barred any foreign national from accessing the models, whether inside or outside the country. Unable to verify the nationality of every user, Anthropic had to switch both off altogether. The stated justification was a contested jailbreak the company calls narrow and no worse than what rivals already offer, a disagreement it voiced even as it complied. Whatever the merits, the episode cleanly illustrates a problem latent in AI for years. Frontier capabilities now run through a handful of private companies, each of which can be compelled, almost overnight, by its home government. It is also the clearest argument yet for crypto's decentralized AI efforts.

To see why this matters beyond Anthropic, consider the structure of the industry around it. The frontier today belongs to a small group of mostly American labs, and the only meaningful external check comes from a handful of Chinese labs, the likes of DeepSeek, Qwen, and Moonshot's Kimi, which release their models with open weights while trailing the leading edge by some months. That check is real, but thinner than it first appears. Open weights are published at the labs' discretion, on infrastructure they alone control, so the world keeps access only for as long as they choose to keep publishing, which could change for commercial or political reasons. The Fable order shows how flimsy this guarantee can be, showing governments can make a lab pull a model from the market, on nothing more than a letter sent on a Friday afternoon.

An alternative has been taking shape, assembled piece by piece over the past couple of years by a loose ecosystem of crypto-adjacent projects. The most striking progress has come in training, long assumed to be the labs' unassailable moat. Prime Intellect has post-trained a 106-billion-parameter model across distributed hardware, Nous Research recently completed one of the largest distributed pre-training runs yet attempted on volunteered GPUs coordinated through an on-chain network, and Gensyn works on verifying that computation done on machines no one controls was performed correctly.

The other layers are filling in around it. Pluralis adds a further twist with its 'protocol learning', which splits a model's weights across participants so that no single party ever holds the complete set, giving contributors a stake while leaving the model with no switch for any one actor to flip. Venice and Near offer private or permissionless inference, and Vana is building a way for users to pool and own the data these systems train on. Individually each remains modest, but together they sketch a full pipeline, from data through training to inference, that runs on commodity hardware and answers to no single owner.

How credible is all this as a real counterweight to centralized AI? More credible than a year ago, certainly, given the recent progress, though still some way from displacing the incumbents. Its strongest point is structural. A model whose weights already sit on thousands of independent machines is far harder to recall globally by an export order, and the claim that frontier-scale compute requires a hyperscaler is weakening. The harder question is whether the decentralized stack can match the labs on raw quality, where the incumbents keep real and demonstrated advantages. For several years it has consistently been the same handful of well-funded labs pushing the frontier forward, on the back of concentrated capital, deep research talent, and training infrastructure others cannot match. Distributed training is closing the compute gap, but matching the labs' funding, talent, and infrastructure all at once is far harder, and the open networks remain a step or two behind for now.

None of this points to decentralized AI unseating the major labs any time soon. The likelier outcome, in our view, is coexistence, with the labs still setting the frontier and producing the strongest individual models while an open, on-chain layer grows alongside them and supplies what the centralized stack cannot: access that no single government can revoke. The two may also combine more directly. Ensemble approaches that pool models that make different mistakes have long been known to beat any alone, a point the Fable order's timing drove home. On the same day the models were pulled, OpenRouter reported that its Fusion tool, which runs a prompt through a panel of models and synthesizes their answers, had a panel of cheaper models come within a point of Fable 5 on a deep-research benchmark at half the cost.

The result comes with caveats, resting on one benchmark and adding the cost and latency of running several models, but it points to near-frontier capability being assembled from a collection of models rather than any single lab. That reframes crypto's role, less a bid to win the capability race than a counterweight to it, a hedge against access being revoked. After Fable, a capable model that cannot be switched off may simply be worth more to some users than a better one that can.

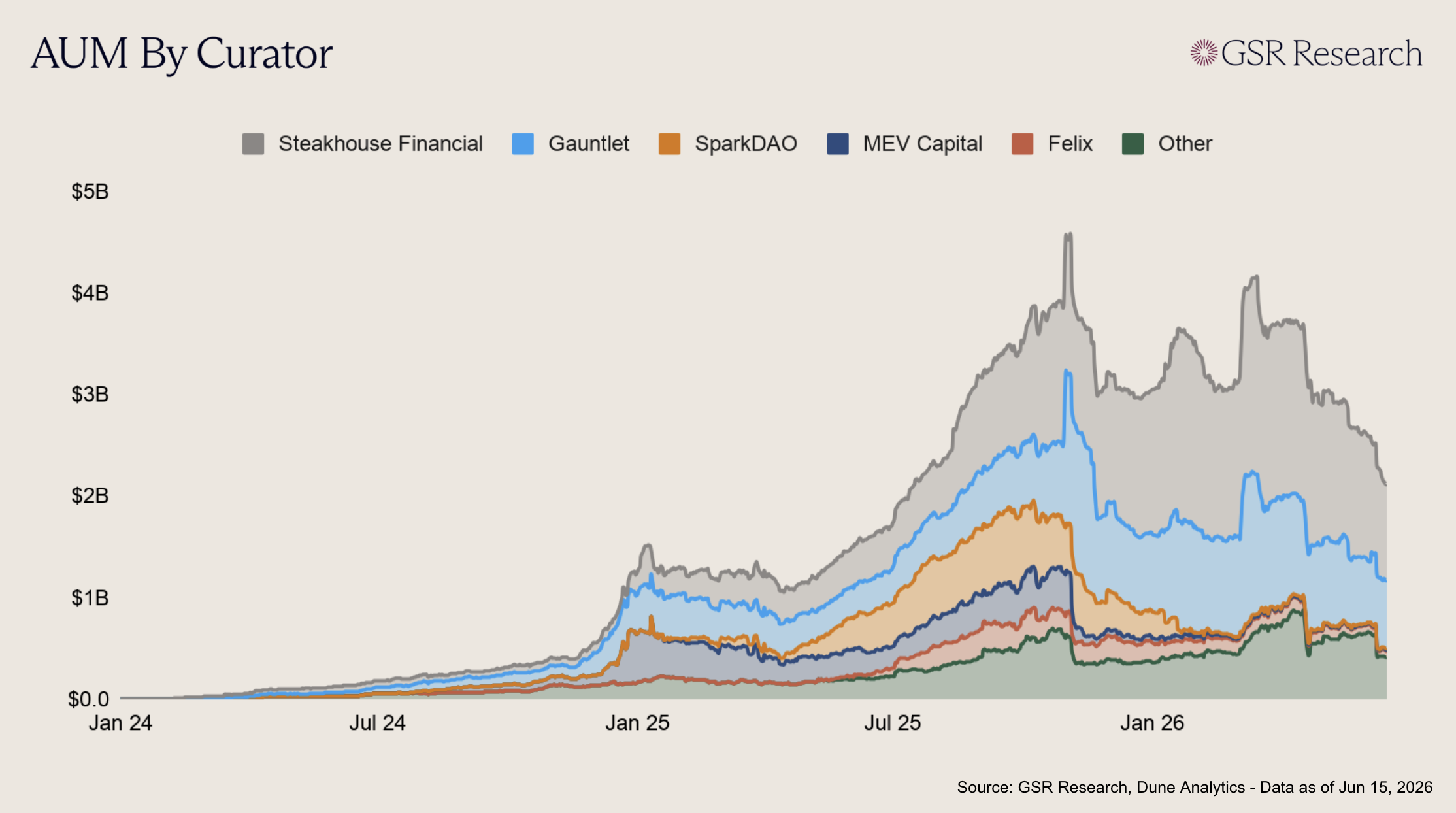

Morpho announced a $175M financing round last week, with the raise co-led by Paradigm, a16z crypto, and Ribbit, with participation from Apollo Funds, Circle Ventures, VanEck, Ledger Cathay, Wintermute Ventures, SBI Group, and several other strategic investors. The round was among the largest ever announced by a DeFi protocol, and stands out even more given that it closed during a still-muted market environment. Notably, it was not structured as a conventional equity round, as investors agreed to purchase MORPHO at the token’s average monthly price, which ended up near a $2B fully diluted valuation. The token sale aligns with Morpho’s broader restructuring over the past year, as Morpho Labs recently became a wholly owned subsidiary of the Morpho Association, with the project moving toward a one-asset model centered around the MORPHO token.

A $175M raise is unusual for a lending protocol that already has a live token, so what is the potential being underwritten by investors here? Morpho’s product is not its code, but its onchain credit, liquidity, distribution, curation, and institutional trust. The contracts can be replicated, but Morpho’s vault network, exchange integrations, institutional relationships, curator ecosystem, and first-mover advantages are difficult to surpass. The team isn’t raising to maintain a codebase, but to become the default credit backend for crypto and traditional financial institutions.

Morpho already has more than $11B in deposits and is used across a growing set of major institutions and platforms, including Coinbase, Kraken, Binance, Bitwise, Galaxy, Anchorage Digital, and FORGE. The Coinbase partnership in particular has given Morpho access to one of the largest retail and institutional distribution channels in crypto, with Coinbase announcing a new high yield USDC vault powered by Morpho just 2 days after the protocol announced its raise. Unlike existing Morpho products available to Coinbase users, including the core USDC vault that lends against safe-haven assets like BTC and ETH at predefined LTV ranges, the high yield vault takes more risk to achieve higher returns. Curated by Steakhouse, the vault lends USDC against a broader, more dynamic collateral set (including Ethena-powered assets), and hit roughly $90M in TVL in less than a day after launching. The new high-yield USDC vault on Coinbase is an illustrative example of why Morpho’s moat is less about protocol design and more about onchain asset management infrastructure.

Morpho’s vault architecture lets curators package lending strategies into risk-managed products, choosing collateral, borrowers, markets, and parameters while plugging into shared liquidity. This has allowed Morpho to become more than a lending venue, as it has evolved into an onchain asset-management layer, where exchanges, wallets, asset managers, and custodians can offer credit products without building the entire lending stack themselves. For Coinbase, that means embedded borrow and yield products. For asset managers, it represents a seamless way to offer curated lending vaults. For institutions like Apollo, it may eventually mean tokenized private credit serving as collateral inside onchain markets.

This raise marks a clear shift in how DeFi is being financed. Morpho could not successfully raise the largest-ever DeFi round as just a lending app. Credit is one of the largest profit pools in financial services, and Morpho is increasingly positioned as the shared infrastructure layer connecting wallets, exchanges, asset managers, custodians, and institutional borrowers. Even in the midst of a bear market, major crypto and TradFi investors are willing to underwrite large size into protocols that could become a future backend for global credit.

Despite the major vote of confidence in DeFi that this investment represents at a particularly delicate period for the space, it also underscores some of the challenges with decentralized governance the space continues to face. To generate the nearly 90M MORPHO tokens necessary for the $175M investment, Morpho governance approved MIP-131 roughly 6 weeks prior to the raise announcement, which allocated 150M MORPHO to the Morpho Association for a 2026 to 2030 strategic support program covering research, development, ecosystem growth, institutional expansion, and partnerships. The proposal passed unanimously, but with relatively low governance participation, and some forum questions around how the tokens would be deployed went largely unanswered. When Morpho later announced the $175M round, critics argued that the DAO had not been sufficiently warned that the allocation could underpin a major token sale.

The Association asked the DAO for tokens to fund development and growth, received those tokens, and sold a portion OTC to long-term investors to fund development and growth. There is nothing inherently inconsistent about the financing logic. It also would have been unrealistic to explicitly telegraph a major investment round inside the DAO proposal itself, as no serious investor wants a deal front-run before commitments are finalized. However, the governance process itself was not as robust as it could have been. MIP-131 effectively authorized the use of up to 150M MORPHO, worth roughly $300M at the later financing valuation, through a proposal whose core rationale was only a few lines long. It described a broad strategic support program, but did not clearly explain that the tokens could be sold to investors as part of a major OTC financing. The vote then passed with just 22 voters, only 8 of whom had an economic stake of $5 or more, and the Association did not substantively answer the one participant who asked questions on the proposal draft.

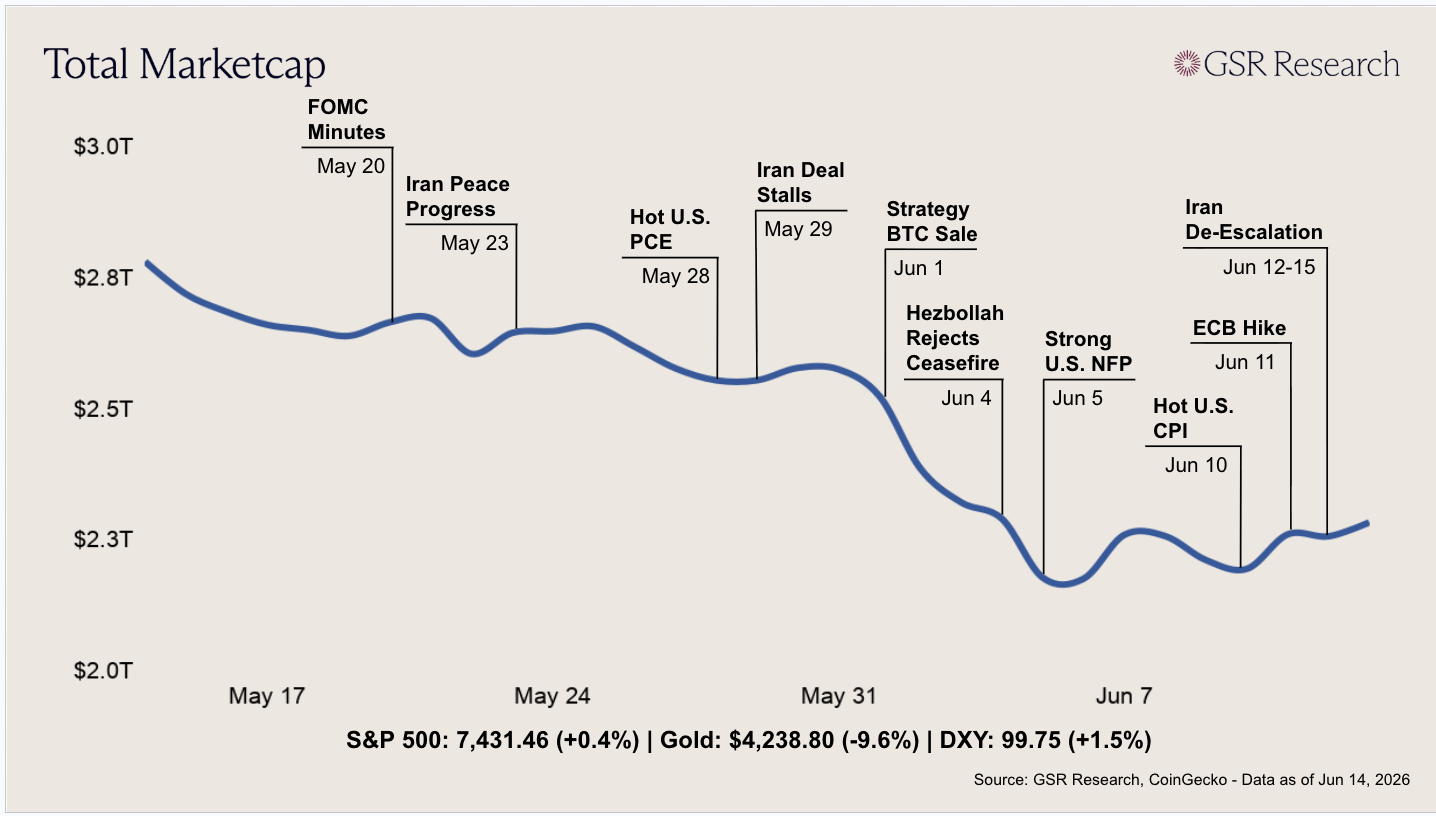

Crypto spent most of the week drifting, caught between a run of hot inflation data and the approach of Kevin Warsh's first meeting as Fed chair. Total market cap opened near $2.23T and eased to around $2.11T by Wednesday as the May inflation print landed, with Bitcoin slipping toward $60,000 and Ether near $1,600. Crypto fell throughout the week while equities rose on Middle East de-escalation hopes, with digital assets again trading as the high-beta end of the risk trade.

Inflation was the main theme for most of the week. May U.S. CPI rose 0.5% on the month and 4.2% over the year, its fastest in about three years, and producer prices the next day climbed 1.1% against expectations closer to 0.7%. Crypto barely reacted, largely because core CPI was far tamer at 2.9%, with energy accounting for most of the increase as the Middle East war kept gasoline high. Markets took the mix as hawkish but not alarming. A hold in the 3.50% to 3.75% range looks all but certain on Wednesday and futures still lean toward hikes rather than cuts being more likely by the end of the year. The ECB, facing the same energy-driven inflation, raised rates for the first time since 2023.

Sentiment improved as the week wore on. On Friday, President Trump said he had called off planned strikes on Iran, and cheaper gasoline was already showing up in sentiment, with the University of Michigan's preliminary June reading bouncing to 48.9 from May's record low. Those hopes firmed over the weekend, and today the US and Iran announced a framework agreement to end the war and reopen the Strait of Hormuz, with a formal signing due Friday in Switzerland. Crypto has rallied on the news, with Bitcoin back above $65,000 and total market cap climbing past $2.24T. Beyond the bounce, the deal begins to unwind the energy shock behind the week's inflation scare and much of the Fed's hawkish lean, leaving Warsh's decision Wednesday as the next test of whether the rally holds.

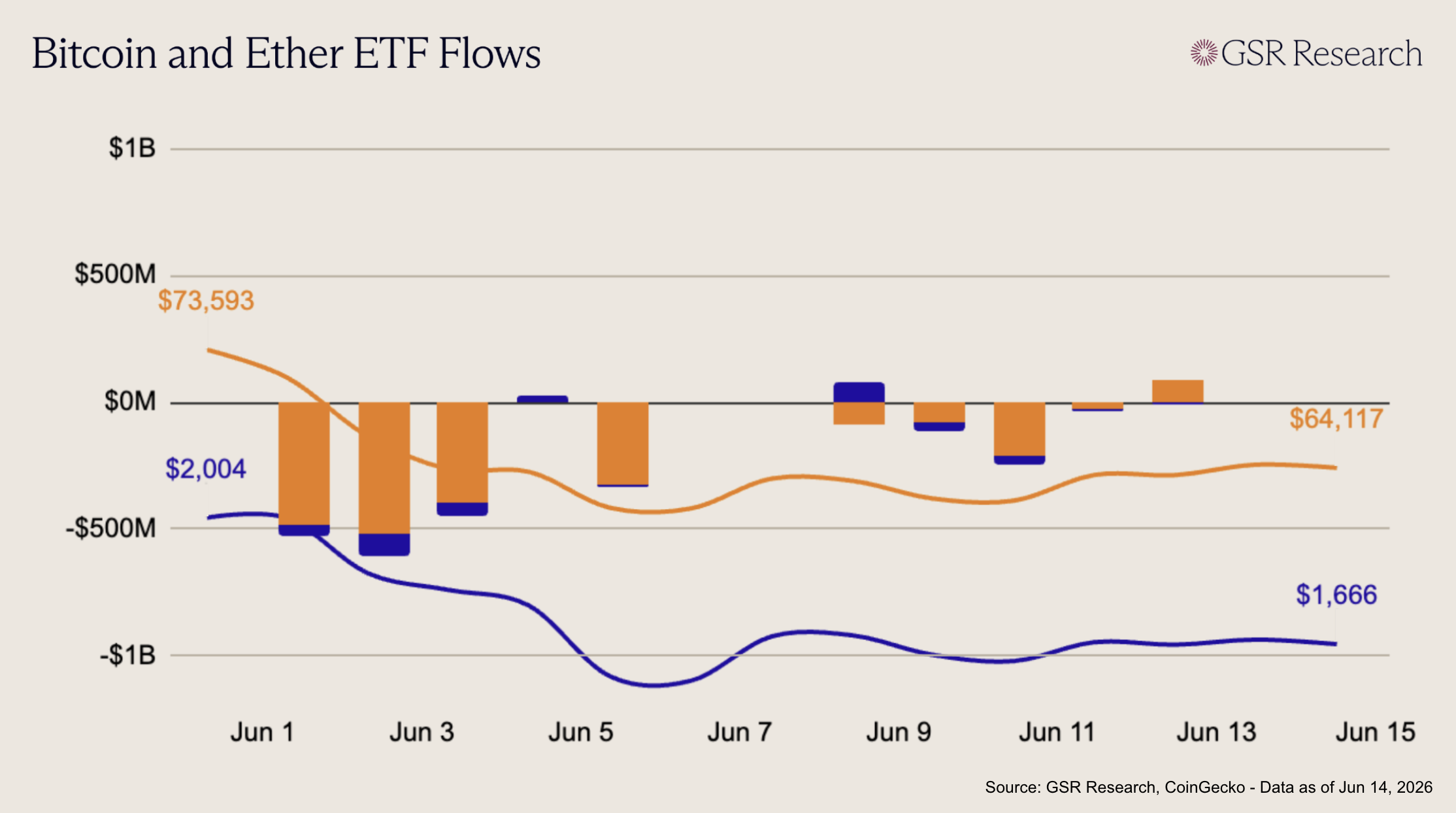

U.S. spot Bitcoin ETFs remained under pressure this week, though the pace of redemptions moderated into the close. The week opened with four consecutive negative sessions: -$91M on Jun 8, -$77M on Jun 9, -$214M on Jun 10, and -$23M on Jun 11, driven primarily by continued withdrawals from IBIT, which lost roughly -$355M across the five sessions. GBTC also added to the drag with a notable -$88M outflow on Jun 10, while FBTC provided some partial offset, finishing the week modestly positive. A stronger Friday print (+$86M on Jun 12) broke the run of daily outflows, but it was not enough to reverse the weekly bleed. Across the week, BTC ETFs lost roughly -$319M, indicating that demand remains impaired even as the scale of selling has eased from the prior redemption cycle.

Ether ETFs showed a more balanced but still slightly negative flow profile. The week began with a strong inflow on Jun 8 (+$82M), led by broad participation across ETHA, ETHB, and FETH, suggesting some initial stabilization after the prior stretch of weakness. However, that momentum faded quickly, with four consecutive outflow sessions following: -$41M on Jun 9, -$36M on Jun 10, -$16M on Jun 11, and -$5M on Jun 12. The selling was less severe than BTC in absolute terms, but the inability to sustain Monday’s inflow left ETH ETFs down roughly -$15M for the week. Overall, ETH flows appear closer to stabilization than BTC, but the repeated failure to build on positive sessions shows that institutional demand remains tentative.

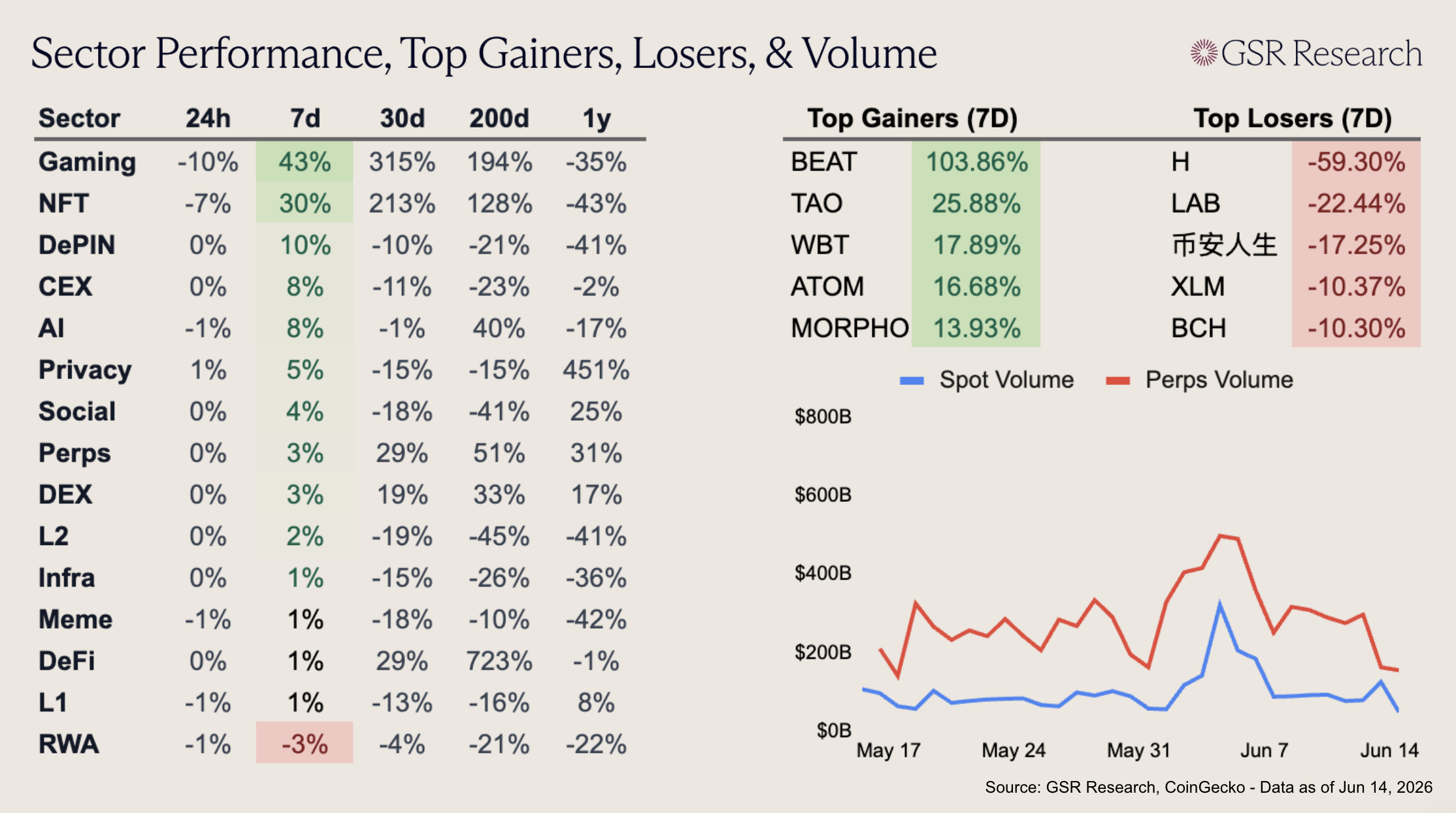

Gaming and NFT sharply outperformed again this week, up 43% and 30%, respectively, with both sectors driven by BEAT’s (+103.86%) continued rise. DePIN also outperformed, up 10%, as TAO (+25.88%) rallied after Anthropic took Fable 5 and Mythos 5 offline to comply with a U.S. export-control directive, reinforcing the decentralized AI narrative. CEX rose 8% as WBT (+17.89%) saw rising retail demand and record perps open interest, while ATOM (+16.68%) gained after Robinhood re-listed the token after several years of absence. MORPHO (+13.93%) rounded out the top gainers following their $175m funding round co-led by Paradigm, a16z crypto, and Ribbit.

Performance outside the leaders was more mixed, with RWA the only sector in the red, down 3%, as Stellar’s XLM (-8.28%) continued to give back part of its DTCC-driven rally. H (-59.30%) was the week’s biggest loser after a private-key compromise drained more than $30m and forced the project to halt bridge activity. LAB (-22.44%) also retraced. BCH (-10.30%) rounded out the top losers after a technical breakdown and forced long liquidations left the token struggling to hold the $200 level.

Click here to download the PDF of the report

This material is provided by GSR (the “Firm”) solely for informational purposes. It is not intended to be advice or a recommendation to buy, sell or hold any investment mentioned. Investors should form their own views in relation to any proposed investment.

It is intended only for sophisticated, institutional investors and does not constitute an offer or commitment, a solicitation of an offer or commitment, or any advice or recommendation, to enter into or conclude any transaction (whether on the terms shown or otherwise), or to provide investment services in any state or country where such an offer or solicitation or provision would be illegal. The Firm is not and does not act as an advisor or fiduciary in providing this material.

This material is not an independent research report, and has not been prepared in accordance with any legal requirements by any regulator (including the FCA, FINRA or CFTC) designed to promote the independence of investment research.

This material is not independent of the Firm’s proprietary interests, which may conflict with the interests of any counterparty of the Firm. The Firm may trade investments discussed in this material for its own account, may trade contrary to the views expressed in this material, and may have positions in other related instruments. The Firm is not subject to any prohibition on dealing ahead of the dissemination of this material.

Information contained herein is based on sources considered to be reliable, but is not guaranteed to be accurate or complete. Any opinions or estimates expressed herein reflect a judgment made by the author(s) as of the date of publication, and are subject to change without notice. The Firm does not plan to update this information.

Trading and investing in digital assets involves significant risks including price volatility and illiquidity and may not be suitable for all investors. The Firm is not liable whatsoever for any direct or consequential loss arising from the use of this material. Copyright of this material belongs to GSR. Neither this material nor any copy thereof may be taken, reproduced or redistributed, directly or indirectly, without prior written permission of GSR.

Please see here for additional Regulatory Legal Notices relevant to US, UK and Singapore.