GSR Weekly Update - May 18th, 2026

BTC: $78,123 (-4.0%) | ETH: $2,186 (-6.9%) | BTC Dom: 58.2% | Global Cap: $2.69T

On May 14, the Senate Banking Committee advanced the Digital Asset Market Clarity Act in a 15-9 vote, clearing the biggest procedural hurdle the bill has faced to date. All thirteen Republicans on the committee voted in favor, joined by Democratic Senators Ruben Gallego and Angela Alsobrooks. The bipartisan crossover was especially notable as it marked the first time material Democratic support materialized for a comprehensive crypto market structure bill at the committee level.

The CLARITY Act answers the key regulatory issue that has defined crypto's legal struggles in the U.S. for years: which digital assets are commodities, which are securities, and who regulates them. The SEC retains jurisdiction over primary market fundraising and the initial sale of tokens to raise capital, while the CFTC takes over secondary market trading for assets classified as digital commodities. The bill also establishes a provisional registration regime that gives exchanges, brokers, and dealers a pathway to operate under CFTC oversight while permanent rules are written, and includes explicit protections for DeFi activities like running nodes and validating transactions.

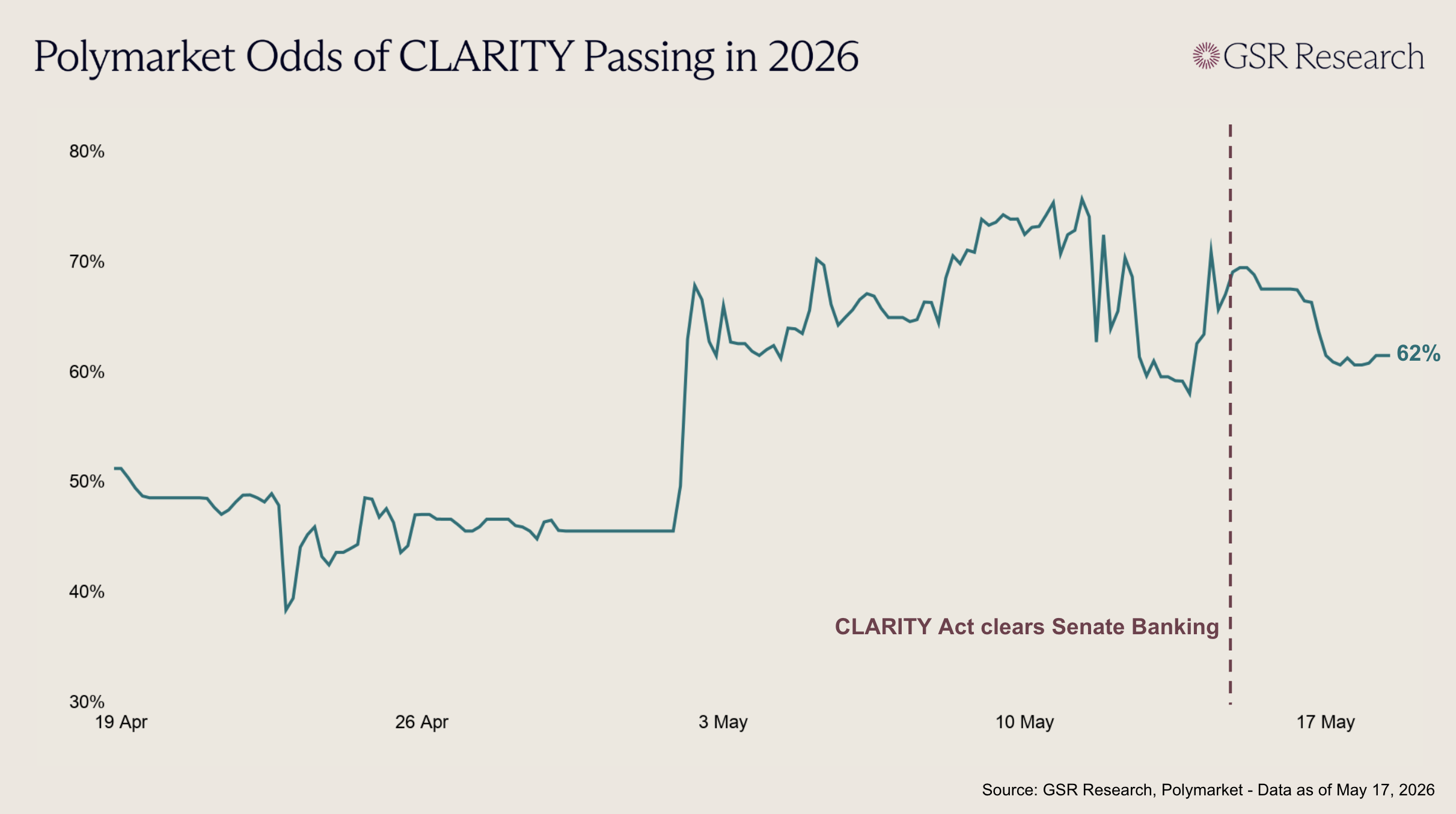

The committee vote, while significant, was the easier part of getting the bill passed. This was reflected in the Polymarket odds of the bill passing in 2026, which spiked following the vote, but soon settled back down. The bill now needs to be merged with the Senate Agriculture Committee's Digital Commodity Intermediaries Act, which passed on a party-line vote in January. Once reconciled, the merged text heads to the Senate floor, where it needs 60 votes to clear a filibuster. With 53 Republican seats, that means roughly seven Democrats need to cross over.

That math is where things get difficult. Gallego and Alsobrooks both explicitly qualified their committee votes as conditional. Gallego warned that he was "not afraid to vote no" on the floor if outstanding issues remain unresolved, and Alsobrooks described her vote as a commitment to keep negotiating in good faith. Their support does not carry over automatically.

The single biggest unresolved issue is the ethics provision. Democrats have demanded language restricting government officials from engaging in crypto activity that creates conflicts of interest, driven largely by President Trump and his family's extensive crypto ventures, including World Liberty Financial and the president's memecoin. An amendment proposed by Senator Van Hollen that would have addressed this in committee failed along party lines, and the issue was left to floor negotiations. Senator Gillibrand has stated plainly that the bill will not reach 60 votes without an ethics deal. White House adviser Patrick Witt signaled at Consensus Miami that provisions targeting the president specifically will not be tolerated, favoring instead rules that apply broadly across all officials. Finding language that satisfies Democrats without triggering a veto will likely prove to be the defining challenge of the next several weeks.

Ethics is not the only sticking point. Law enforcement groups argue the bill doesn't do enough to prevent illicit crypto transactions. Banking trade associations continue to argue against the existing stablecoin yield provisions even after an agreement on these finally allowed the bill to advance. And the legislative window is tight: if the bill doesn't clear the floor before the August recess, the midterm campaign season compresses the calendar so much that several senators have warned the next viable window could stretch to 2030.

If the CLARITY Act makes it through, the implications extend across the industry. Most immediately, assets that clear as digital commodities would shed the regulatory overhang of SEC enforcement, giving altcoins a structural re-rating. Tokens with active SEC litigation history stand to benefit the most: XRP led the market reaction to the committee vote, briefly clearing $1.54 before settling back down.

But the broader impact lies in what the bill would unlock structurally. Its explicit protections for non-custodial DeFi activities would remove the legal ambiguity that has pushed developers and capital offshore for years. For exchanges, a federal registration pathway under the CFTC would reduce reliance on today’s state-by-state patchwork for many trading-market activities, which has made it cheaper and simpler to operate overseas, potentially helping to onshore trading activity and volumes that migrated to offshore venues during the enforcement era. Banks would similarly gain a clear on-ramp for custody, settlement, and tokenized asset services. And on the most fundamental level, the CLARITY Act would replace regulation by enforcement with an actual statutory framework. That shift alone, even before the SEC and CFTC finish their rulemakings, would represent a meaningful change in how institutional capital evaluates the space.

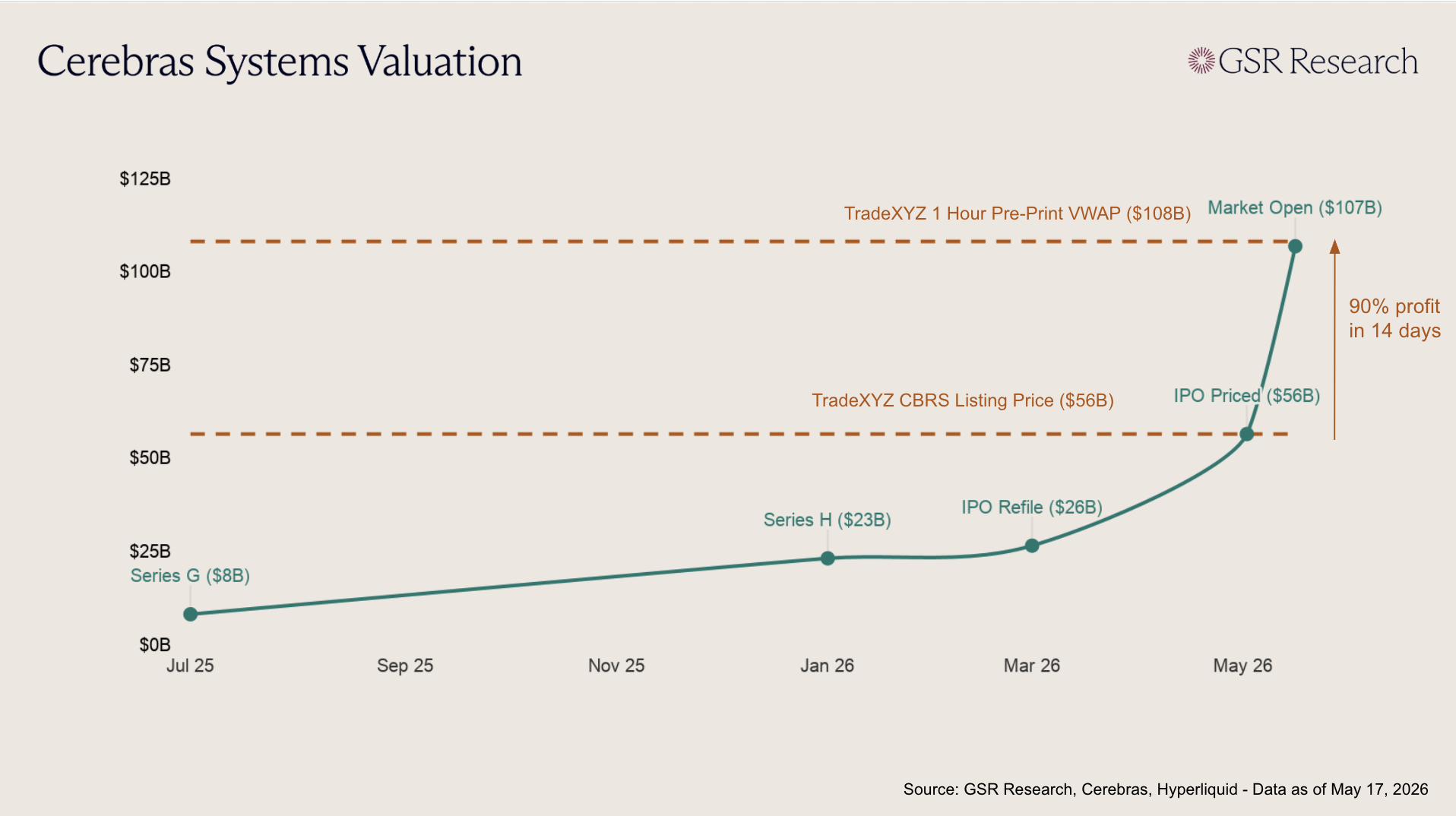

On May 14, Cerebras, an AI chipmaker, began trading on Nasdaq after raising $5.55B in the largest U.S. tech IPO since Uber. Despite pricing its IPO at $185, well above its already-raised range of $150 to $160, Cerebras opened on Nasdaq at $350, highlighting a familiar TradFi dynamic where underwriters often underprice hot offerings, institutional demand overwhelms supply, and retail investors are left buying the stock at a much higher valuation once public trading begins. However, TradeXYZ’s CBRS market gave traders 24/7 synthetic exposure before the listing, processing more than $200M of pre-open volume with usable liquidity and a 62 bps median spread. The pre-IPO perp market first listed on TradeXYZ on May 1st, allowing traders to lock in 90% profits in the 2 weeks leading up to the listing. By the launch window, TradeXYZ’s one-hour pre-print VWAP was just 1.2% above Nasdaq’s eventual $350 opening print. The pre-market pricing closely matching the opening print despite the stock opening far above its IPO level suggests that TradeXYZ could increasingly become a trusted venue for non-crypto investors seeking pre-IPO price discovery.

TradeXYZ’s markets have replaced what was once a fragmented and highly gated price discovery process with a continuous public order book. While traditional pre-IPO exposure still depends on brokered secondaries, SPVs, large minimums, delayed settlement, transfer restrictions, and opaque reference prices, TradeXYZ’s pre-IPO perps give traders constant liquid exposure to the most desired private companies prior to public listings. Cerebras was an ideal test case as the IPO was heavily oversubscribed and inaccessible to most participants. With several other private giants, including SpaceX, Anthropic, OpenAI, and Databricks moving toward eventual public listings, repeated oversubscription dynamics could turn pre-IPO price discovery into one of crypto’s most durable innovations.

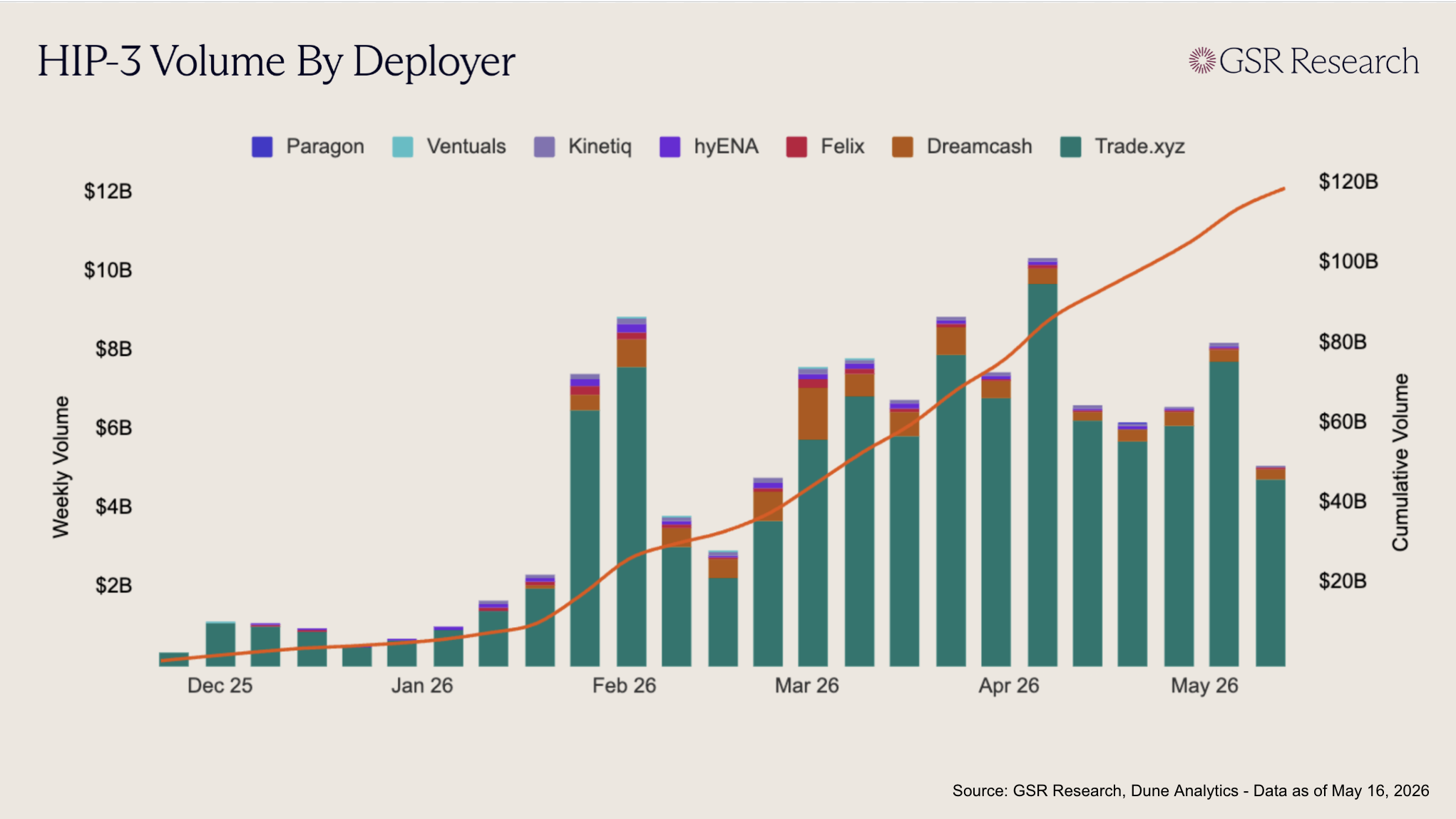

TradeXYZ’s success with Cerebras helps further cement its lead in Hyperliquid’s HIP-3 ecosystem. TradeXYZ has maintained a dominant market share by listing markets that decentralized exchanges have historically not offered, including equities, commodities, FX, indices, and now, pre-IPO contracts. Instead of competing on major pairs, TradeXYZ has targeted traditional markets that remain closed, fragmented, or unavailable outside normal trading hours. The attached chart shows how dominant that strategy has been. TradeXYZ has contributed over $104B of the $118B in cumulative HIP-3 volumes, or more than 88%. They achieved this by bringing always-on access to markets traders already cared about but could not previously trade in a unified account.

Incumbents are no longer just paying attention, but are actively engaging with regulators on concerns with decentralized exchanges. CME and ICE, the owner of the NYSE, have reportedly pushed U.S. regulators to scrutinize Hyperliquid, citing concerns around anonymous trading, manipulation, and sanctions evasion. This is clear recognition that Hyperliquid, primarily through TradeXYZ, is beginning to make significant impact in markets legacy exchanges care about. Onchain venues increasingly look less like esoteric exchanges and more like competing market infrastructure as they facilitate meaningful volume in equities, commodities, oil-linked contracts, and pre-IPO price discovery.

The irony is that CME, NYSE, and other incumbents are all moving toward the same endpoint themselves: 24/7 trading, tokenized assets, instant settlement, and digital collateral. Their objection is not necessarily to the always-on market structure itself, but to that market structure growing outside regulated exchange and clearing rails. The recent Cerebras IPO shows why the pressure is likely to increase. TradeXYZ did not democratize ownership of a private company, but it gave traders a better way to price one before listing. If the same structure works for future IPO candidates like SpaceX, OpenAI, or Anthropic, pre-IPO perps could represent one of the most consequential crypto-native wedges into traditional capital markets.

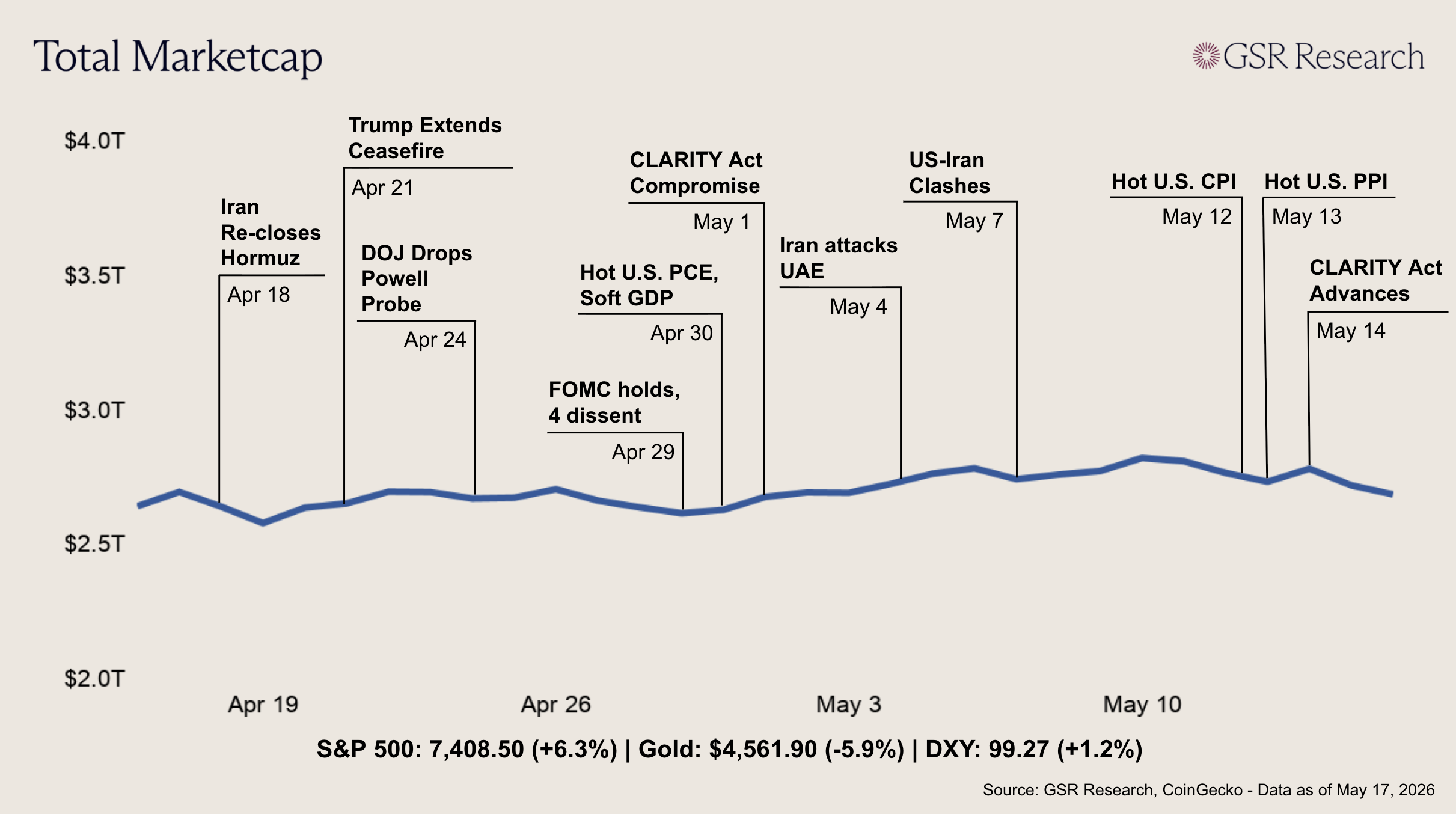

Crypto markets gave back ground last week as a pair of hot inflation prints all but eliminated 2026 rate cut hopes, with a historic Fed leadership transition layered on top. A constructive US-China summit in Beijing and progress on the CLARITY Act in the Senate provided some support but were not enough to overcome inflation-driven pessimism. BTC opened the week near $81,200, briefly tested $82,000 on Thursday after the CLARITY vote, and then rolled over to finish around $78,000 on Sunday. Total crypto market cap fell from roughly $2.81T to $2.7T over the week.

The inflation prints did most of the damage. April CPI on Tuesday came in at 3.8% YoY versus 3.7% consensus, the highest reading since May 2023, with energy alone accounting for over 40% of the monthly increase as the Hormuz blockade pushed into its tenth week. Wednesday's PPI was the bigger shock at 1.4% MoM versus 0.5% consensus, the largest monthly print since March 2022, and 6% YoY. Trade services jumped 2.7%, a sign that tariff costs are now flowing meaningfully into producer and distributor margins. CME FedWatch now shows 0.4% odds of cuts through 2026 as of May 18, with rate hike odds now at 44%.

The Fed handover landed against that backdrop. The Senate confirmed Kevin Warsh as chair on Wednesday in a 54-45 vote, the closest margin in the modern era. Powell's term as chair officially ended on Friday, though he will remain on the Board of Governors for the near-term. Warsh was Trump's pick to deliver faster cuts, but the back-to-back inflation surprises have boxed him in ahead of his first FOMC meeting on June 16-17. Elsewhere, the Trump-Xi summit in Beijing produced a "constructive strategic stability" framework and a joint commitment to keeping the Strait of Hormuz open, though no major trade breakthrough emerged. Focus now turns to the FOMC minutes and NVIDIA earnings on Wednesday, along with any early signals from Warsh on his policy stance heading into the June meeting.

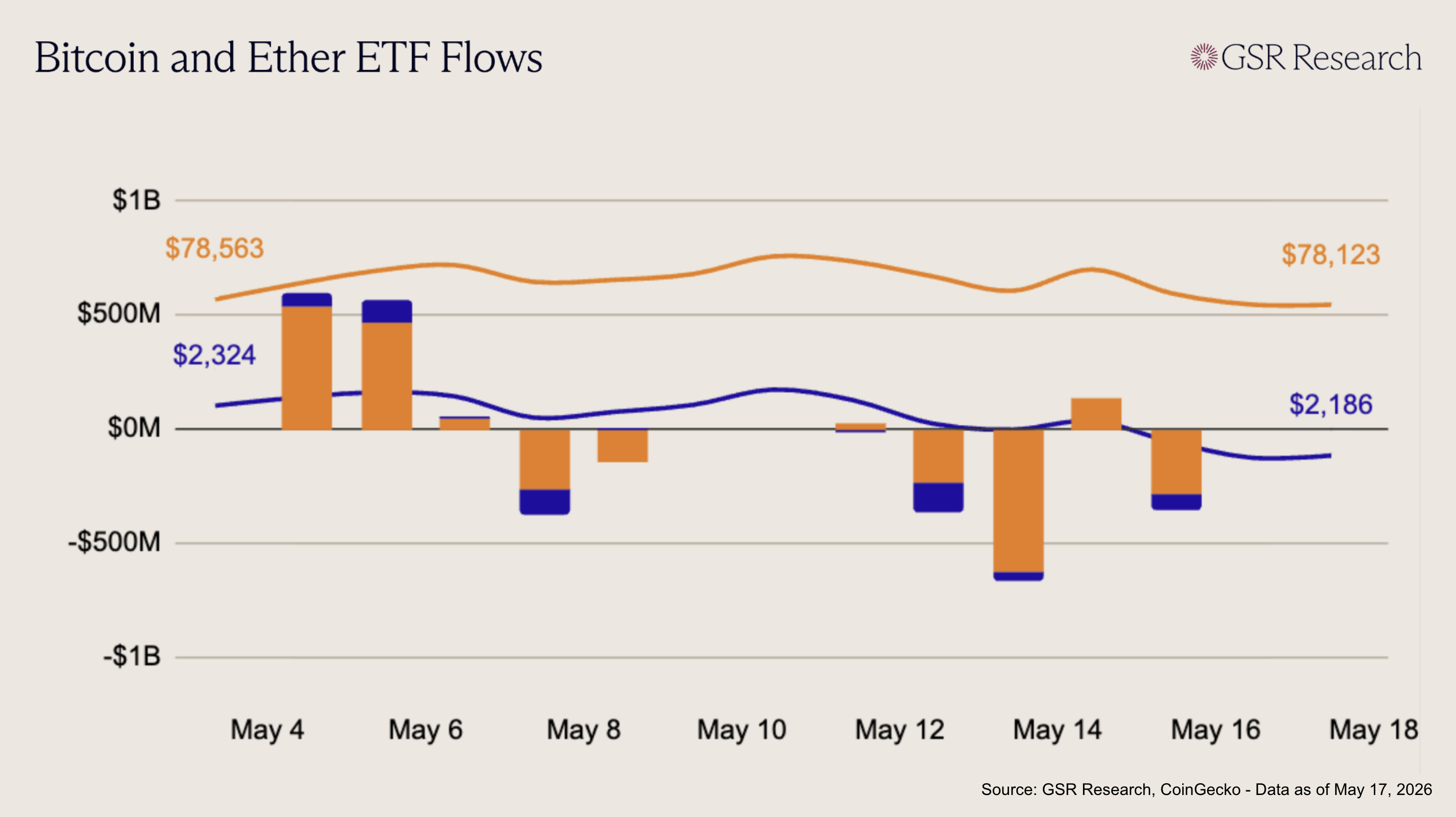

U.S. spot Bitcoin ETFs saw a decisive shift back toward outflows this week, with the brief stabilization on May 11 (+$27M) quickly overwhelmed by sustained redemptions through the rest of the period. Flows turned sharply negative on May 12 (-$233M), then accelerated into a major drawdown on May 13 (-$630M), the largest outflow day of the week and a clear signal of broad institutional de-risking. While May 14 briefly interrupted the selling with a positive print (+$131M), the rebound lacked follow-through, with redemptions returning on May 15 (-$290M). Overall, BTC ETFs finished the week down roughly -$995M, marking a sharp deterioration from the prior week’s more balanced flow profile.

Ether ETFs were even more consistently negative, with every session this week closing in outflow territory. The week opened with modest redemptions on May 11 (-$17M), but pressure intensified quickly on May 12 (-$131M), driven primarily by heavy withdrawals from ETHA and FETH. Outflows persisted through the back half of the week, with continued selling on May 13 (-$36M), May 14 (-$6M), and May 15 (-$66M). Unlike BTC, ETH did not see any meaningful rebound day to offset the drawdown, underscoring a more persistent lack of institutional demand. Across the week, ETH ETFs lost roughly -$255M, reinforcing the weaker relative flow profile and highlighting how ETH remains more vulnerable as broader demand softens.

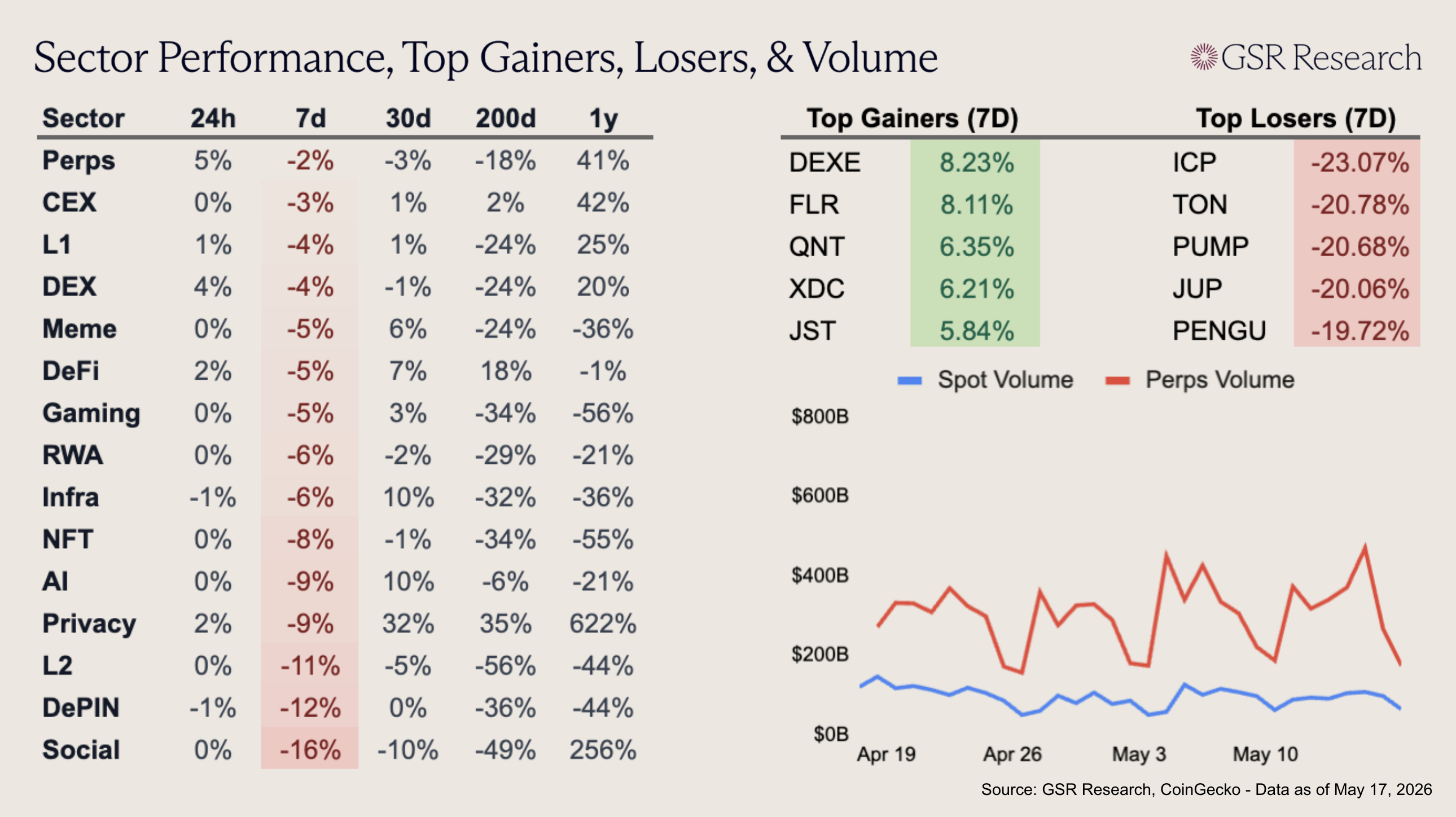

It’s been a brutal week for altcoins, with all sectors in the red and most erasing their gains from the prior week. Social was hit the hardest, down 16% due to losses in PUMP (-20.68%) and ZORA (-23.13%). DePIN followed closely behind, down 12% as Bittensor (-19.51%) and Filecoin (-16.4%) sold off. Layer-2s were also hit hard, down 11% after losses in Arbitrum (-18.1%), Optimism (-19.2%), and Starknet (-19.6%).

TON (-20.78%) was among the top losers this week, wiping out its prior-week gains. The demand for TON has dissipated faster than expected, especially considering the recent announcement that Telegram is taking a leading role in the chain’s development. Jupiter (-20.06%) also sold off after rallying due to favorable news the week before. The recently announced partnership between Securitize, Jupiter, and Jump to launch tokenized equities on Solana has failed to provide much resilience for the token’s performance.

Click Here to Download The PDF of the Report

This material is provided by GSR (the “Firm”) solely for informational purposes. It is not intended to be advice or a recommendation to buy, sell or hold any investment mentioned. Investors should form their own views in relation to any proposed investment.

It is intended only for sophisticated, institutional investors and does not constitute an offer or commitment, a solicitation of an offer or commitment, or any advice or recommendation, to enter into or conclude any transaction (whether on the terms shown or otherwise), or to provide investment services in any state or country where such an offer or solicitation or provision would be illegal. The Firm is not and does not act as an advisor or fiduciary in providing this material.

This material is not an independent research report, and has not been prepared in accordance with any legal requirements by any regulator (including the FCA, FINRA or CFTC) designed to promote the independence of investment research.

This material is not independent of the Firm’s proprietary interests, which may conflict with the interests of any counterparty of the Firm. The Firm may trade investments discussed in this material for its own account, may trade contrary to the views expressed in this material, and may have positions in other related instruments. The Firm is not subject to any prohibition on dealing ahead of the dissemination of this material.

Information contained herein is based on sources considered to be reliable, but is not guaranteed to be accurate or complete. Any opinions or estimates expressed herein reflect a judgment made by the author(s) as of the date of publication, and are subject to change without notice. The Firm does not plan to update this information.

Trading and investing in digital assets involves significant risks including price volatility and illiquidity and may not be suitable for all investors. The Firm is not liable whatsoever for any direct or consequential loss arising from the use of this material. Copyright of this material belongs to GSR. Neither this material nor any copy thereof may be taken, reproduced or redistributed, directly or indirectly, without prior written permission of GSR.

Please see here for additional Regulatory Legal Notices relevant to US, UK and Singapore.