GSR Weekly Update - June 1st, 2026

BTC: $73,395 (-3.8%) | ETH: $1,998 (-4.5%) | BTC Dom: 57.3% | Global Cap: $2.56T

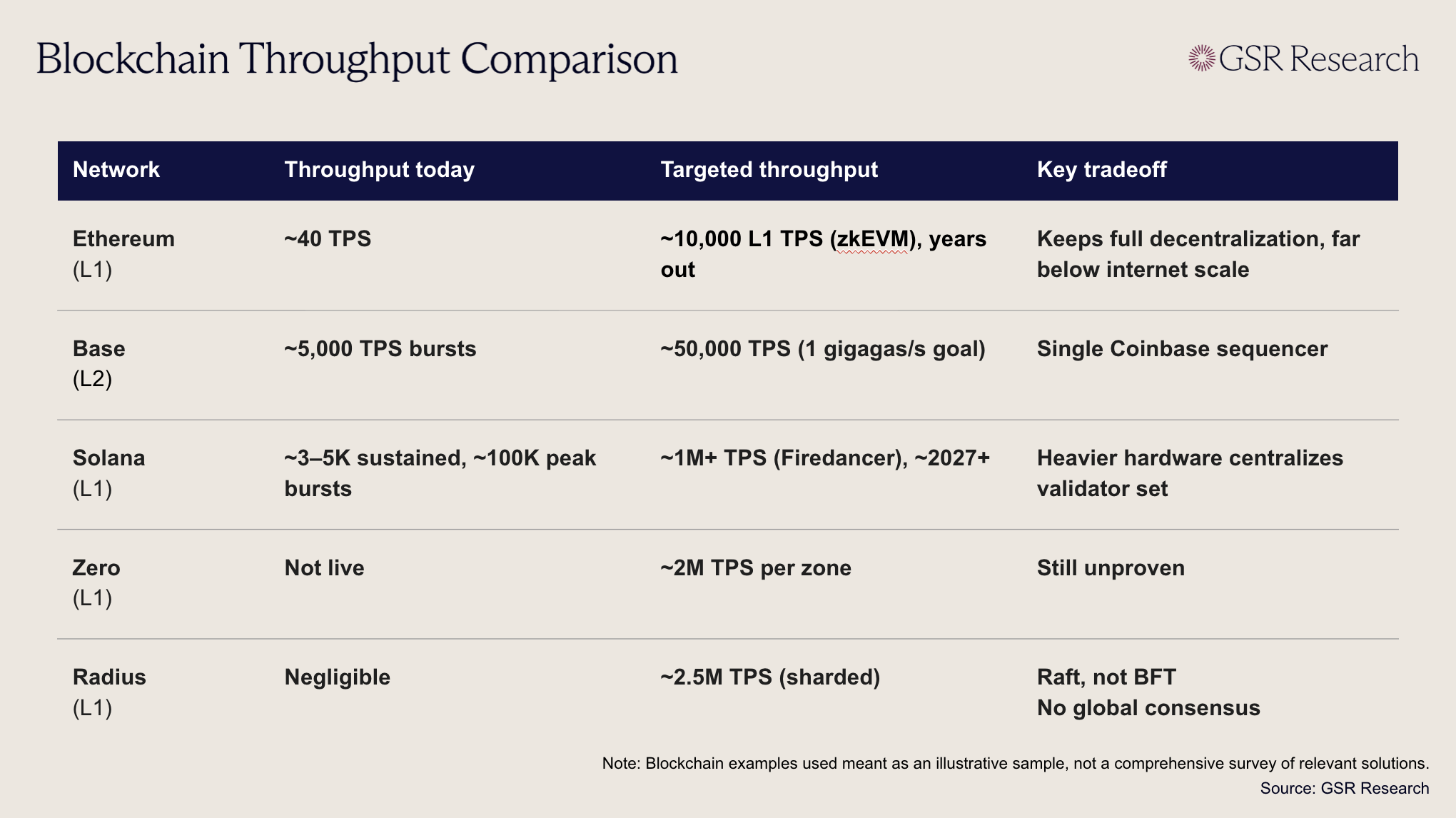

Cloudflare CEO Matthew Prince appeared on the Bankless podcast last week and dropped what might be the most striking demand signal the blockchain industry has received from outside its own walls. In brief, Cloudflare handles about 500 million HTTP requests per second, and Prince estimates that between 1% and 10% of those could be monetized through internet-native micropayments. Consequently, he needs a stablecoin payment rail capable of somewhere between 5 million and 50 million transactions per second. However, the highest claimed throughput his team has seen from any blockchain is around 2 million. His ask to the crypto industry was surprisingly direct: if you can build a chain that supports 5+ million TPS, call Cloudflare.

Prince’s comments come amid an ongoing evolution in the way information is consumed online, which is creating a void that blockchain payments could be uniquely suited to fill. As AI agents take over a growing share of web traffic, the advertising model that has funded the internet for three decades is collapsing, because agents don't click on ads. Prince, alongside Coinbase and others, is developing x402, a payment protocol that would let AI agents make stablecoin micropayments whenever they access monetized content. Each individual transaction is a fraction of a cent, but at Cloudflare's volume those fractions add up to a potentially large enough size to replace advertising for significant portions of the web. Conventional payment rails would struggle to support this use case. Visa's flat per-transaction fees make sub-cent payments unworkable. A high-throughput blockchain settling stablecoins is, in Prince's estimation, the only viable path.

Cloudflare’s call to action underscores an uncomfortable reality for the industry. Blockspace seems abundant today. A raft of high-performance L1 and L2 protocols have been built promising to end the industry’s scalability woes. Those chains’ blocks sit mostly empty today, with transaction fees across many of these reaching all-time lows of late. The industry zeitgeist has for some time called for shifting builder focus away from infrastructure and towards creating useful applications to fill the empty blockspace that already exists instead. But now that Cloudflare is coming along with an application and arguably more demand than the industry has ever received, it appears existing solutions come up short. It turns out the kind of blockspace needed to support internet-scale throughput still hasn’t been built.

A natural question arises here: what kind of architecture could meet Cloudflare’s needs? Ethereum's ZK-based endgame targets around 10,000 TPS on L1, a big jump from today's ~40 but still two to three orders of magnitude short. Base’s recent Azul upgrade brings the network within an order of magnitude of its ‘gigagas’ target, but even once it reaches the latter its throughput for payments is expected to peak at around 50,000 TPS. Solana consistently processes low thousands of TPS, and has reached a peak ceiling of over 100,000. The network’s core developers are aiming to achieve over 1 million TPS in the coming years, but that would still fall short. Layer Zero's Zero, targeting 2 million TPS per zone through a multi-core ZK architecture with lightweight validators on consumer-grade hardware, is among the most ambitious designs we've seen that still aims for genuine blockchain-grade decentralization. But even Zero only approaches the lower bound of what Prince says he needs.

The projects claiming numbers above 2 million TPS sacrifice key blockchain properties to get there. Radius, which was born out of research on payments systems at MIT and the Federal Reserve, advertises 2.5 million TPS through independent sharding, with each shard running a three-node Raft consensus cluster. However, this architecture looks more like a distributed database than a decentralized blockchain. It may achieve impressive numbers, but arguably trades away the properties blockchains exist to provide: decentralized consensus, permissionless participation, censorship resistance, and the resulting freedom from needing to trust, and pay rent to, any single intermediary.

The tradeoff between decentralization and scalability is well-worn territory for the industry, but the internet-scale demands of the likes of Cloudflare put it back into sharp relief. The guarantees that make blockchains worth building on for payments, the ones that prevent vendor lock-in, rent extraction, unilateral rule changes, and single points of failure, are exactly the properties that become hardest to preserve as you push throughput toward internet scale. What the industry needs is faster settlement with those trust properties intact. Whoever solves it could seize what might be one of the defining opportunities of the industry's next decade.

The WSJ recently published a stablecoin-focused piece titled Stablecoins Are Private Money. That’s Why They’re a Risk to the Economy, in which chief economist Greg Ip argued that stablecoins, as a representation of the return of private money, pose an imminent risk to the broader economy. His framing is deliberately simple: private monetary issuance failed before, stablecoins are private monetary issuance now, and even new regulation cannot eliminate the risk of runs, fragmentation, or broader financial contagion. The problem is that this argument treats “private money” as the danger itself, rather than asking the more important questions of what backs the liability, how transparent the issuer is, what redemption rights exist, and how the instrument behaves under stress. Bank deposits are private money too. Money-market funds are private money too. The modern dollar system already runs on private liabilities layered on top of public money, and Stablecoins are not a break from that model, but a new version of it built on top of blockchain settlement.

Key parts of Ip’s argument rests on a particular reading of economic history and the free-banking era in the U.S., yet his claims are contested at best. The U.S. free-banking era is often invoked as proof that privately issued money inevitably becomes chaotic, however that period was not a clean experiment in laissez-faire banking. State rules forced many banks to issue notes against government bond collateral, and those bonds often became illiquid or impaired, particularly as Civil War risk rose. Many banks were also restricted from branching, leaving them geographically concentrated and vulnerable to local shocks. The problem was not private issuance, but bad collateral rules, fragmented bank structures, and poor regulatory design. Additionally, successful private note systems in established countries like Scotland and Canada challenge the “private money failed, public money saved us” story. It’s not that private money cannot work, but that reserve quality, diversification, redemption mechanics, and market discipline determine whether it will.

Ip also compares stablecoins to money-market funds that can “break the buck,” but this analogy only goes so far. The Reserve Primary Fund broke the buck in 2008 because it held Lehman commercial paper, a credit-sensitive asset that collapsed when confidence disappeared. In fairness, this is a risk, which is exactly why modern regulated stablecoin frameworks are designed to prevent them. The GENIUS Act requires payment stablecoin issuers to maintain 100% reserve backing with liquid assets like U.S. dollars, short-term Treasuries, and similar high-quality instruments, while also requiring public monthly reserve disclosures. That does not make stablecoins risk-free, but it makes them far closer to narrow banks than to prime money-market funds reaching for yield.

Ip’s “singleness” critique is more serious, yet still overstated. His argument is that for money to function properly, one dollar must always equal one dollar regardless of where it is held, who issued it, or what rail it moves across. Stablecoins can trade a few basis points away from par, and USDC’s 2023 depeg during the Silicon Valley Bank collapse showed that even large stablecoins can face confidence shocks when reserve banking partners fail. However, that episode also undercut the idea that traditional bank dollars are perfectly singular. SVB depositors did not experience seamless dollar certainty until public authorities intervened. The practical question is not whether stablecoins are metaphysically identical to Fed liabilities at every instant, which they obviously are not. The question is whether they are reliable enough to function as digital dollars across exchanges, payments companies, remittance corridors, DeFi protocols, and corporate settlement flows. On that standard, the market’s behavior is already answering yes.

The claim that less than 1% of stablecoin use is for real-economy payments is also more fragile than it sounds. Even if most activity still comes from trading and financial settlement, that is true of ordinary dollars as well. Securities settlement, repos, FX, and financial market plumbing dwarf consumer payments in the traditional system. More importantly, stablecoin payments data is still early and methodologically messy. The Kansas City Fed estimate behind the “less than 1%” line is based on assumptions about supply usage, not a full census of global payments activity, while BCG and Allium estimate real-economy stablecoin payments reached $350B to $550B in 2025. Payments are not yet the dominant use case, but they are also no longer immaterial.

The illicit-finance argument has the same issue. Chainalysis says stablecoins represented 84% of illicit crypto transaction volume in 2025, but that mostly reflects the fact that stablecoins have become crypto’s dominant transaction medium. The more important denominator is total activity, where illicit transactions remain below 1% of attributed crypto volume. Stablecoins are used by bad actors because they are useful, liquid, global dollar instruments. Traditional payment rails face similar issues with illicit flows, and in both cases that’s a fixable challenge for enforcement to handle. It’s not, however, an indictment of stablecoins as a payment instrument.

The better conclusion is that stablecoins should be judged issuer by issuer and reserve by reserve, not dismissed because they are private. Transparent, tightly reserved, redeemable stablecoins are fundamentally different from opaque offshore liabilities or undercollateralized experiments. Ip is right that private money can be fragile, but wrong to imply that fragility is inherent to stablecoins as a category. Issuer trust will be determined by reserve quality, redemption access, transparency, and regulation, not by nostalgia for a monetary system that was never as purely public as its defenders pretend.

Crypto extended its losing streak to a third straight week and opened June in the red, with BTC sliding from roughly $76,400 to around $73,300 and total market cap easing from $2.64T to about $2.5T as sentiment dropped into Extreme Fear. The weakness ran counter to traditional markets, where over the same holiday-shortened week the S&P 500 booked its ninth consecutive weekly gain, its longest streak since 2023, the Dow closed above 51,000 for the first time, and the Nasdaq capped the month up more than 8% on blowout AI-linked earnings from the likes of Snowflake and Dell.

Much of the volatility traced back to the on-again, off-again US-Iran talks. Sentiment soured midweek as the two sides traded missile strikes and Brent crude briefly topped $96, before reports of a 60-day memorandum to extend the ceasefire and reopen the Strait of Hormuz sent crude to a nearly 19% monthly loss, its worst since 2020. That optimism unwound once Trump's Friday "final determination" meeting ended without a decision, leaving the framework unsigned. The standoff flared again beginning this week, with the US striking Iranian military sites over the weekend after Tehran downed a US drone and Iran's Revolutionary Guard claiming a retaliatory hit on a US air base Monday, though Trump downplayed the exchange and said Iran still wanted a deal.

The week's April PCE report gave buyers little to work with, with headline inflation at a three-year high of 3.8% and the Fed firmly on hold. Attention now turns to Friday's May jobs report, where payrolls are expected to slow materially, which could reshape a rate-path debate that has lately leaned toward a hike. Crypto policy returns to focus as Congress reconvenes, with comment periods on the GENIUS Act's stablecoin rules on the Treasury side closing June 2 and the Senate restarting its push on the Clarity Act market structure bill. Markets will also watch whether the ceasefire can hold and look ahead to Chair Warsh's first FOMC meeting on June 16-17.

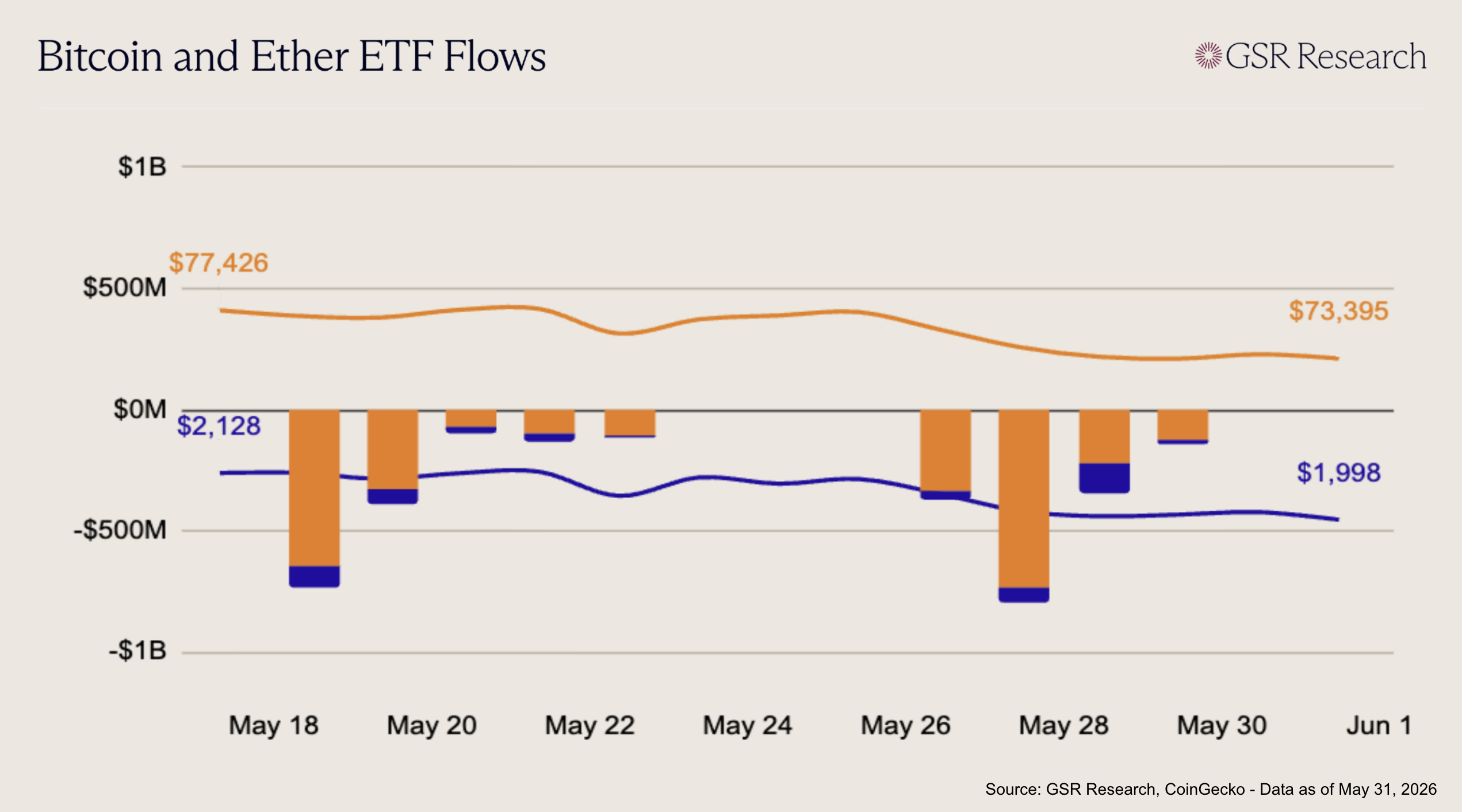

Bitcoin ETFs just posted their first ever two week stretch of exclusively negative daily net flows since launch, breaking the prior record of eight straight outflow days set in February 2025. After last week’s five consecutive outflow sessions, selling continued through the holiday-shortened week with four more negative prints: -$334M on May 26, -$733M on May 27, -$223M on May 28, and -$125M on May 29. That left BTC ETFs down roughly -$1.42B for the week, following about -$1.26B the prior week. The heaviest pressure came from IBIT, which lost -$966M across the four sessions, while FBTC, GBTC, BITB, and BTC also contributed meaningfully.

Ether ETFs also logged a second consecutive all-negative week, with no positive sessions to break the outflow trend. Redemptions continued on May 26 (-$35M), May 27 (-$67M), May 28 (-$121M), and May 29 (-$18M), bringing the weekly total to roughly -$242M after about -$216M of outflows the prior week. The largest pressure again came from ETHA, which lost -$188M across the four sessions, while FETH, ETHE, and ETH added to the drag. Unlike BTC, ETH’s negative streak has been even more persistent, running every session from May 12 through May 29 in the data provided. The consistency of the redemptions points to a broad and sustained lack of institutional demand, with ETH continuing to show weaker flow resilience even as BTC absorbs the larger absolute dollar outflows.

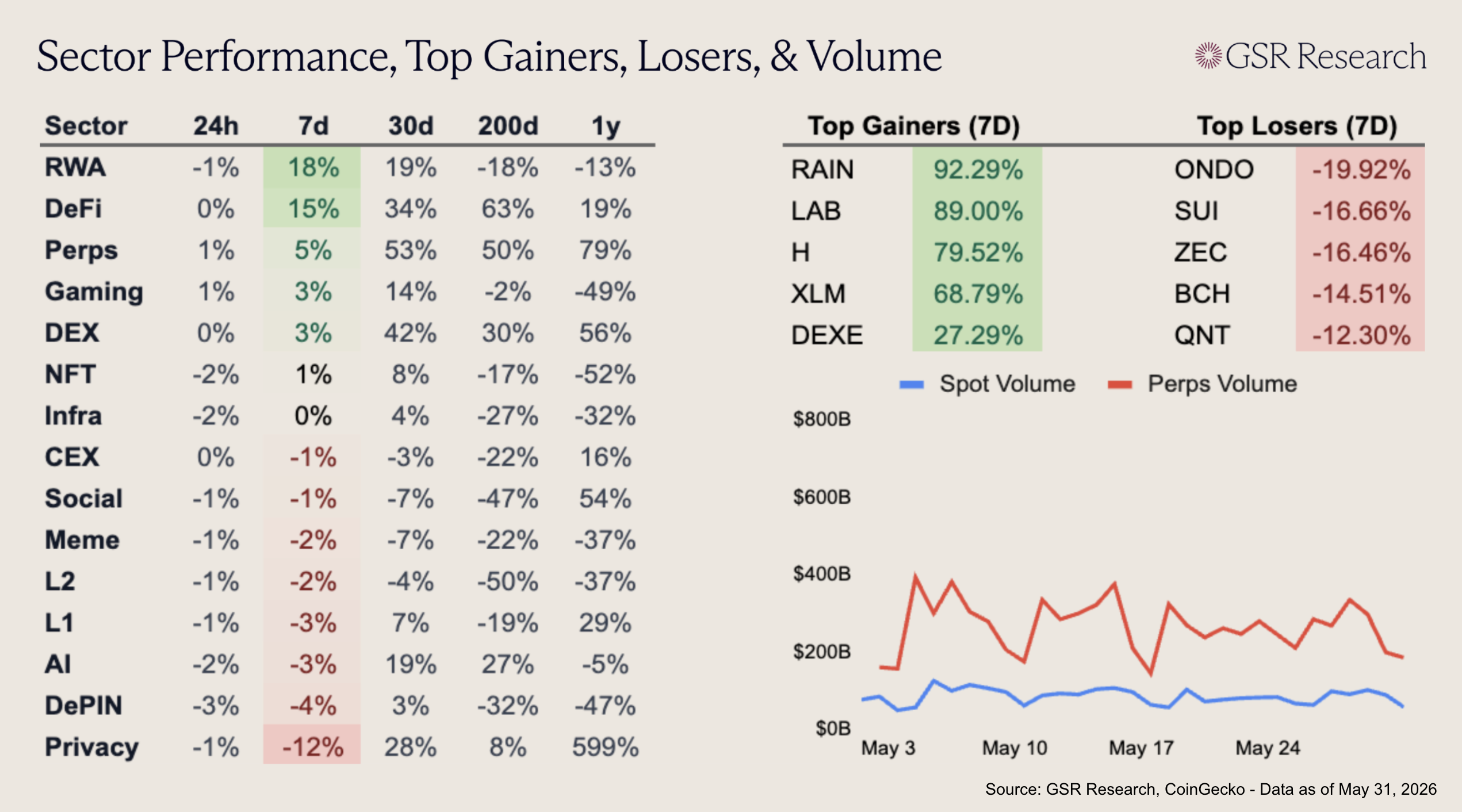

Despite the selloff in the broader market, several sectors and tokens outperformed this week, with RWA and DeFi up double-digit percentages. Prediction market protocol Rain (+92.29%) rallied following news of its $100 million commitment to support the launch of Rain V2 ahead of the FIFA World Cup. XLM (+68.79%) also pumped after a report stated that the DTCC planned to connect its tokenized securities platform to Stellar, reinforcing the token’s RWA narrative.

Broader performance was narrow, with most sectors flat to down on the week. Privacy was the clear laggard, down 12% as ZEC (-16.46%) retraced after a volatile late-May rally, with roughly $10m of liquidations weighing on the token. SUI (-16.66%) was also among the top losers after the network suffered a nearly six-hour outage caused by a software bug, its second major downtime event of the year. ONDO (-19.92%) was the week’s biggest loser, weighing on RWA at the margin despite the sector’s overall strength. The selloff was driven in part by a key-person shock after Ondo confirmed the unexpected passing of founder Nathan Allman, with longtime president Ian De Bode stepping in as CEO.

Click Here to Download The PDF of the Report

This material is provided by GSR (the “Firm”) solely for informational purposes. It is not intended to be advice or a recommendation to buy, sell or hold any investment mentioned. Investors should form their own views in relation to any proposed investment.

It is intended only for sophisticated, institutional investors and does not constitute an offer or commitment, a solicitation of an offer or commitment, or any advice or recommendation, to enter into or conclude any transaction (whether on the terms shown or otherwise), or to provide investment services in any state or country where such an offer or solicitation or provision would be illegal. The Firm is not and does not act as an advisor or fiduciary in providing this material.

This material is not an independent research report, and has not been prepared in accordance with any legal requirements by any regulator (including the FCA, FINRA or CFTC) designed to promote the independence of investment research.

This material is not independent of the Firm’s proprietary interests, which may conflict with the interests of any counterparty of the Firm. The Firm may trade investments discussed in this material for its own account, may trade contrary to the views expressed in this material, and may have positions in other related instruments. The Firm is not subject to any prohibition on dealing ahead of the dissemination of this material.

Information contained herein is based on sources considered to be reliable, but is not guaranteed to be accurate or complete. Any opinions or estimates expressed herein reflect a judgment made by the author(s) as of the date of publication, and are subject to change without notice. The Firm does not plan to update this information.

Trading and investing in digital assets involves significant risks including price volatility and illiquidity and may not be suitable for all investors. The Firm is not liable whatsoever for any direct or consequential loss arising from the use of this material. Copyright of this material belongs to GSR. Neither this material nor any copy thereof may be taken, reproduced or redistributed, directly or indirectly, without prior written permission of GSR.

Please see here for additional Regulatory Legal Notices relevant to US, UK and Singapore.