GSR Weekly Update - May 25th, 2026

BTC: $76,405 (-2.1%) | ETH: $2,096 (-4.1%) | BTC Dom: 58.1% | Global Cap: $2.64T

The recent months have been one of the rougher stretches for the Ethereum community in recent memory. At least nine senior Ethereum Foundation contributors have departed in 2026, with five leaving in May alone. The list includes protocol cluster leads Tim Beiko and Barnabé Monnot, veteran researchers Carl Beekhuizen and Julian Ma, and former co-executive director Tomasz Stańczak. Several exits followed a controversial internal mandate centered on CROPS (Censorship resistance, Open source, Privacy, and Security), which many perceived as deprioritizing growth and adoption. Dankrad Feist, formerly at the EF, publicly called for a new $1B+ organization economically aligned with Ethereum to fill the void. Even Bankless co-host and long-time ETH bull David Hoffman revealed he had sold all of his ETH, citing frustration with leadership he views as disinterested in growth.

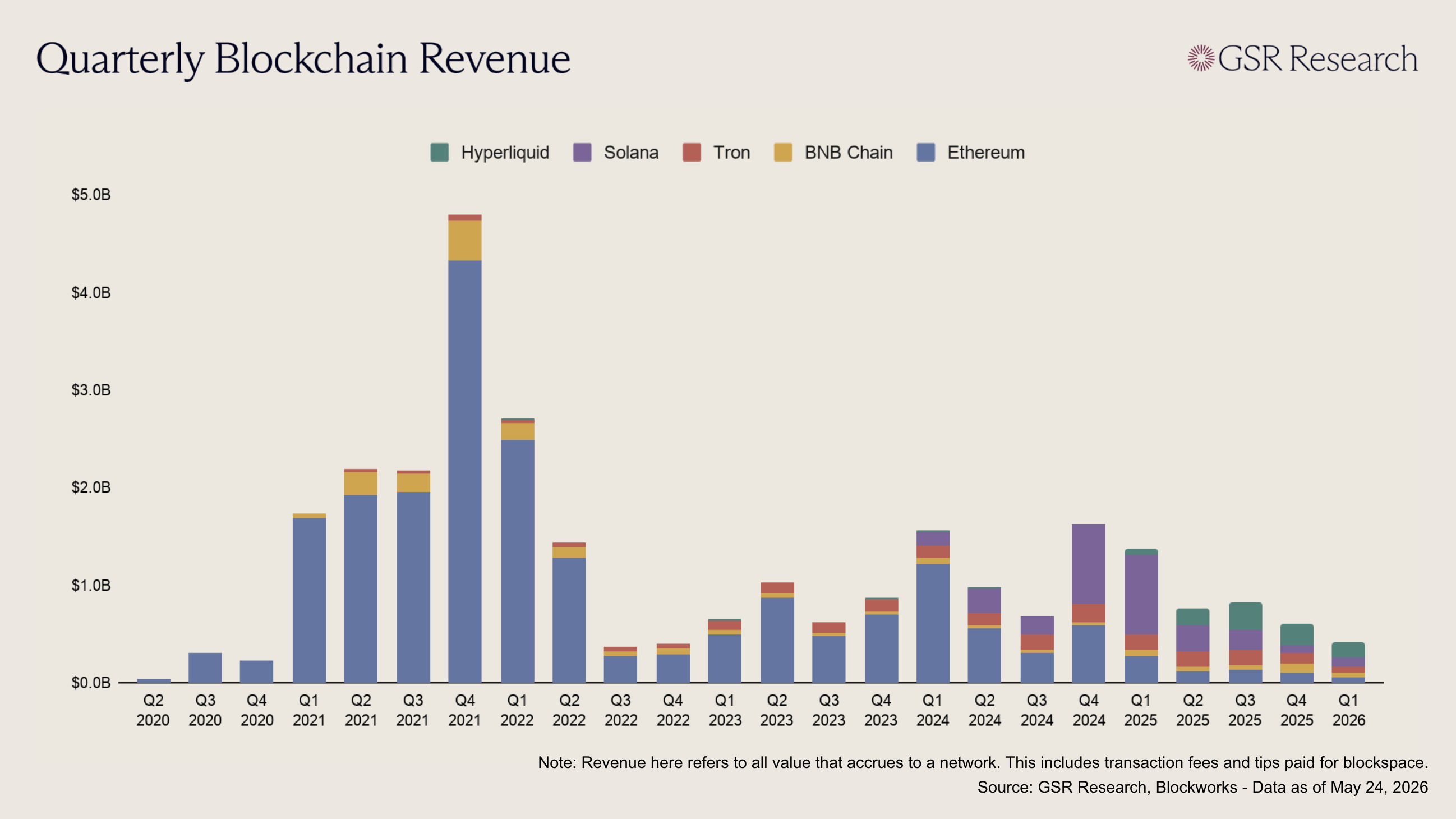

The market backdrop magnifies the negative sentiment within the Ethereum community. ETH is down roughly 30% year to date, and the ETH/BTC ratio hit 0.027 in May, its lowest since mid-2025. Network revenue, a proxy for willingness to pay for blockspace, tells a similar story: Ethereum dominated this metric during the 2021 bull run but has steadily ceded ground to chains like Solana, Tron, and Hyperliquid. Revenue doesn’t tell the full story, since chains are actively lowering fees to compete and attract more users, but the trendline still paints a picture of Ethereum losing ground to nimbler upstarts.

Vitalik Buterin stepped into the fray with a lengthy post on X outlining his personal vision for the foundation's future. He envisions the EF as "a smaller ship" that will sell less ETH and focus narrowly on CROPS rather than trying to steward the entire ecosystem. Vitalik stressed the foundation should be understood as "one node, with a defined purpose," not Ethereum's center. Relocating talented people into other roles outside of the EF, he argued, is in some sense necessary to allow important functions to attract outside capital and foster independent leadership.

The more interesting part was his technical vision, which laid out three pillars for making Ethereum "deeply impressive" in ways competitors cannot replicate. First, provably bug-free software through AI-assisted formal verification, an approach that seemed unrealistic until recently but is now on the cusp of feasibility. Second, "available chain consensus," a property unique to Ethereum among PoS chains: it provides both traditional BFT-style safety under network asynchrony and Bitcoin-like safety under synchrony up to 49% attackers. No other PoS chain offers both. Third, intermediary minimization, reducing dependence on centralized relayers and third-party infrastructure for basic operations like transaction inclusion and privacy, through proposals like FOCIL and EIP-8141. Executing on all three would make Ethereum highly secure, decentralized, private, and censorship resistant.

What Vitalik is articulating is, at its core, a bet on credible neutrality as Ethereum's durable competitive advantage. That bet is more compelling than Ethereum’s critics give it credit for. A common refrain among crypto commentators is that "blockspace is a commodity," but the fact that users consistently pay higher fees to transact on one chain over another suggests otherwise. Blockspace is differentiated by what sits on top of it: the apps, the assets, the liquidity, the other users. Credible neutrality is what attracts those things, because builders and institutions gravitate toward platforms they can trust won't be captured or co-opted. This is what builds network effects, and network effects are what create durable moats.

But credible neutrality is only one piece of it. Users want to be where the assets and apps are, but they also need to transact there affordably, quickly, privately, and with a decent experience. Ethereum still falls short on several of these fronts relative to newer competitors. The risk is that a nimbler chain builds sufficient network effects by executing well on fees, throughput, and UX today while promising credible neutrality tomorrow. Vitalik's vision is arguably the right one. Whether the ecosystem can execute on it before that window closes remains uncertain.

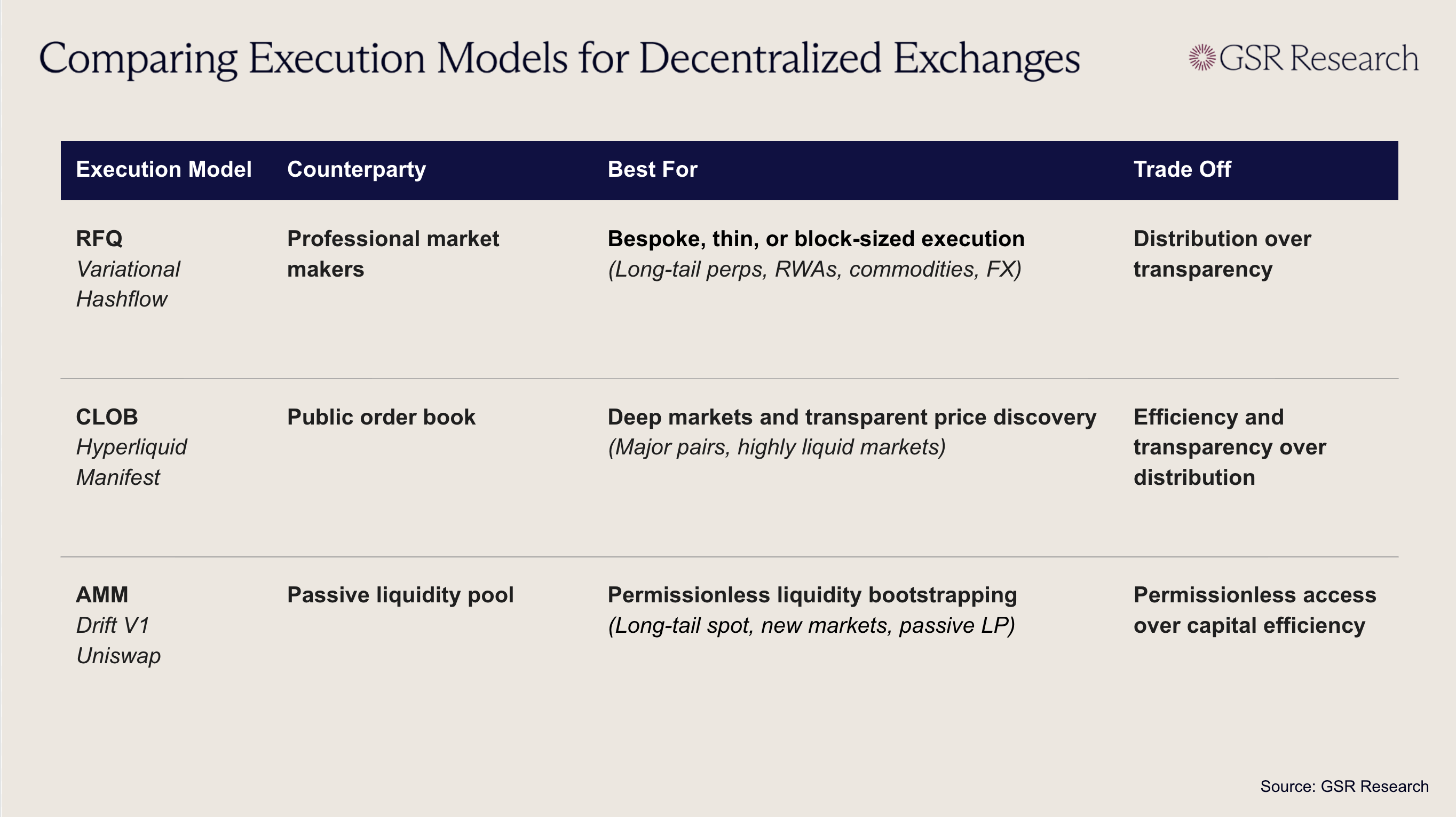

On May 20th Variational announced a $50M raise at an undisclosed valuation for their Series A, reigniting discussion around one of the most important market structure debates in DeFi. Variational is a request-for-quote (RFQ) derivatives exchange designed to bring hundreds of real-world markets onchain without bootstrapping a fresh order book for every asset. The product differs meaningfully from central limit order book (CLOB) products like Hyperliquid or Lighter, where traders interact with a public book that has buyers, sellers, and market makers all continuously compete on price. RFQ models like Variational have users request quotes directly from professional market making firms, who then source and hedge liquidity across CEXs, DEXs, OTC venues, and for certain assets, even traditional markets like the CME or NYSE.

Variational’s raise immediately revived the RFQ versus CLOB debate on X, with protocols, market makers, and influential investors weighing in. RFQ proponents argued that order books work well for BTC, ETH, SOL, as well as a small number of highly liquid markets, but are increasingly inefficient as exchanges scale into longer-tail assets. Outside the top assets, order books often become thin, subsidy-dependent, and fragile during volatility. Additionally, RFQ models solve the cold start problem by letting dealers quote just-in-time and hedge on the primary venue as flow arrives, which is closer to how many institutional markets already work.

CLOB proponents were quick to point out that RFQ models in crypto are often less competitive than their TradFi equivalents. In traditional markets, RFQs are usually sent to multiple dealers and benchmarked against deep external markets. In crypto, the user is often facing one market maker, who, after getting filled on a quote, will just hedge exposure on a CLOB. RFQs are better products for quick access, but do not create the same public, competitive price discovery as onchain order books do. CLOBs also have a stronger DeFi-native argument as public liquidity is readable, composable, and usable by other smart contracts. Vaults, liquidators, structured products, and trading bots can all interact with visible onchain depth in ways that are obfuscated by RFQ models that execute through private quotes.

Holistically, there is no perfect structure, as both models serve different purposes. RFQ models do maintain a distribution advantage, and are best suited for long-tail RWAs, commodities, FX pairs, and products where natural onchain liquidity does not yet exist. On the other hand, CLOBs are superior when it comes to composability and price discovery. They are more efficient in dense, high-turnover markets where continuous two-sided liquidity exists natively. Variational made a purposeful choice when selecting a RFQ system as they sacrificed native on-venue price competition in exchange for broader listings, faster market creation, and the ability to import liquidity from the deepest underlying venues rather than trying to rebuild every market from scratch. Variational’s bet is that the next wave of onchain growth will come from importing existing offchain liquidity into crypto rails, while Hyperliquid, Lighter, and other CLOBs aim to make the order book itself a programmable onchain primitive.

Despite sitting in the middle of the debate, AMMs have largely been left out of the broader RFQ vs CLOB discussion, likely because most perp DEXs have moved away from pure vAMMs toward order books, hybrid AMMs, or oracle-priced LP pools, as pure vAMMs are hard to manage under toxic flow and large directional OI. Additionally, they suffer with professional-size derivatives flow, capital efficiency, and assets that depend on external benchmarks. For perps, AMMs are no longer a dominant execution model, but a capital layer that can sit underneath CLOB systems when passive liquidity is useful. Even Hyperliquid, the strongest CLOB-native perp venue, still relies on HLP as a passive liquidity layer. While HLP functions as a pooled market-making and liquidation backstop rather than a pure AMM, it illustrates the importance of passive capital even in high-volume orderbooks.

Additionally, spot AMMs remain the simplest way to bootstrap permissionless liquidity, especially for long-tail tokens, and passive LP strategies. They also preserve one of DeFi’s most important design principles: any asset can launch a market without needing a market maker, dealer relationship, or centralized listing process.

Each model serves its specific purpose best. AMMs remain the default for permissionless spot liquidity, RFQs are a distribution layer for assets where traders want exposure before native liquidity exists, and CLOBs dominate the most liquid, reflexive trading markets. The debate on X was framed as a winner-take-all stakes, yet the market has already moved toward a hybrid structure. Use RFQ to launch sparse markets and import depth, use CLOBs once liquidity is dense enough for public competition, and use AMMs where permissionless liquidity matters more than execution quality.

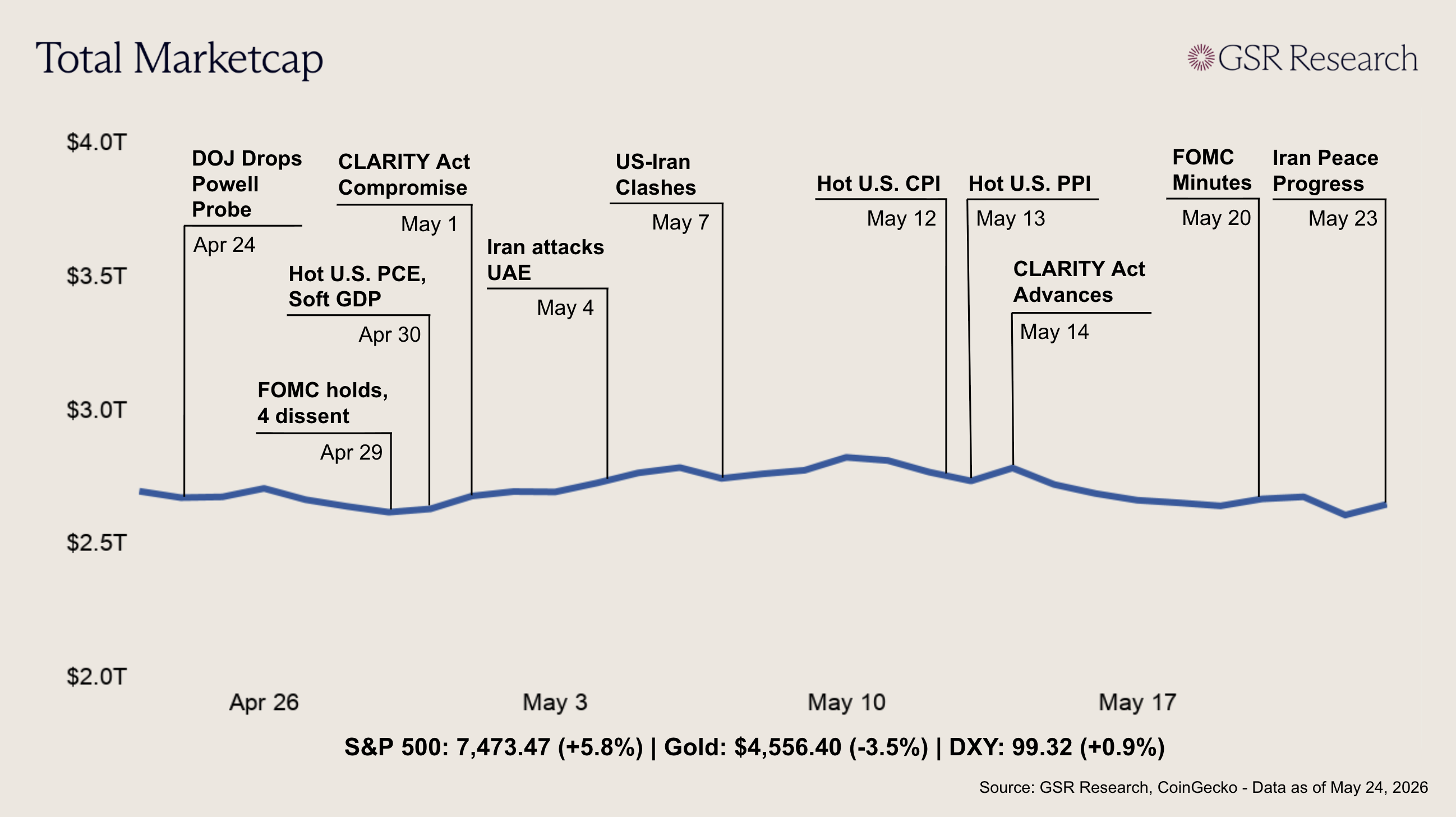

Crypto markets fell for a second straight week as the Federal Reserve's hawkish shift accelerated, driving BTC to its lowest level in over a month before a sharp weekend bounce on Iran peace deal headlines. BTC opened near $78,000 and drifted lower through midweek, briefly catching a bid after NVIDIA's blowout earnings on Wednesday, then dropped to roughly $74,200 on Friday as macro selling intensified. Trump's announcement of progress on an Iran peace agreement pulled the price back to approximately $77,000 over the weekend, but total crypto market cap still declined from $2.7T to roughly $2.6T.

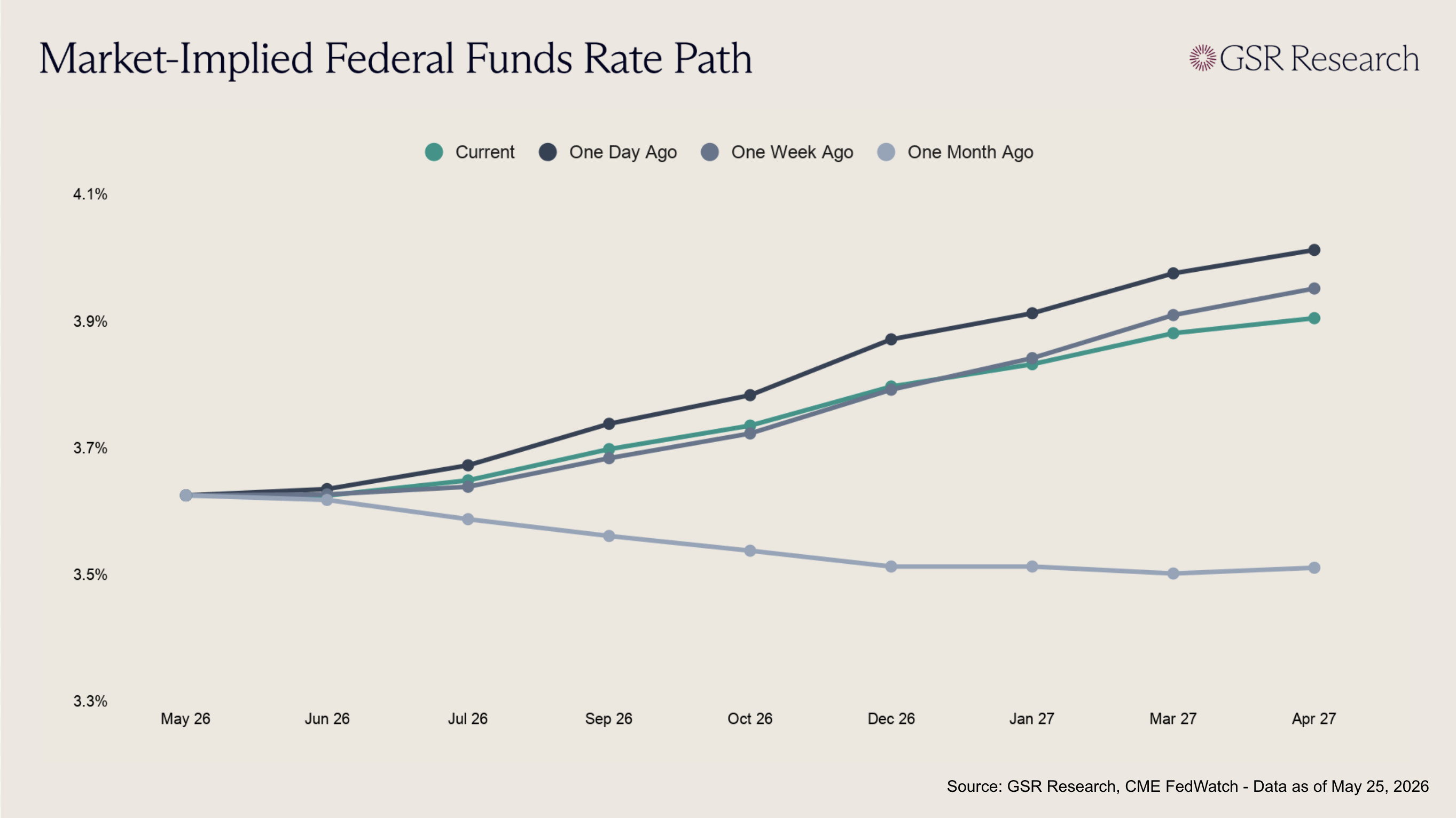

Wednesday's release of the April FOMC minutes set the week's tone, and it was clearly hawkish. A majority of policymakers indicated that some tightening would likely become appropriate if inflation stays persistently above target, and many wanted to strip the easing bias language from the post-meeting statement entirely. CME FedWatch shifted to show 54% odds of a rate hike at the December meeting, up from 44% the prior week. Governor Waller reinforced the message on Friday in a Frankfurt speech, warning that he can no longer rule out hikes and calling current talk of cuts "crazy," a notable pivot given that he had backed 75 basis points of easing as recently as late 2025. NVIDIA's record $81.6B revenue beat on Wednesday briefly lifted sentiment, but the stock slipped after hours and the positive spillover into crypto faded quickly, underscoring how firmly macro has been driving price action.

Friday concentrated several catalysts. The final Michigan consumer sentiment reading came in at 44.8, a new all-time low, with long-run inflation expectations surging to 3.9% from 3.5%. Kevin Warsh was formally sworn in as Fed chair that same morning, inheriting a committee that is leaning hawkish while Trump told a rally audience hours later that rates would come down "very quickly." BTC broke below $75,000 as the sentiment data compounded the ongoing selloff, before reversing sharply on Saturday after Trump said a peace memorandum with Iran had been "largely negotiated," including a proposed 60-day ceasefire extension and the reopening of the Strait of Hormuz. Brent crude ended the week down more than 6% as markets priced in reduced geopolitical risk. Focus now turns to Warsh's first FOMC meeting on June 16-17 and whether the Iran framework holds together into a lasting agreement.

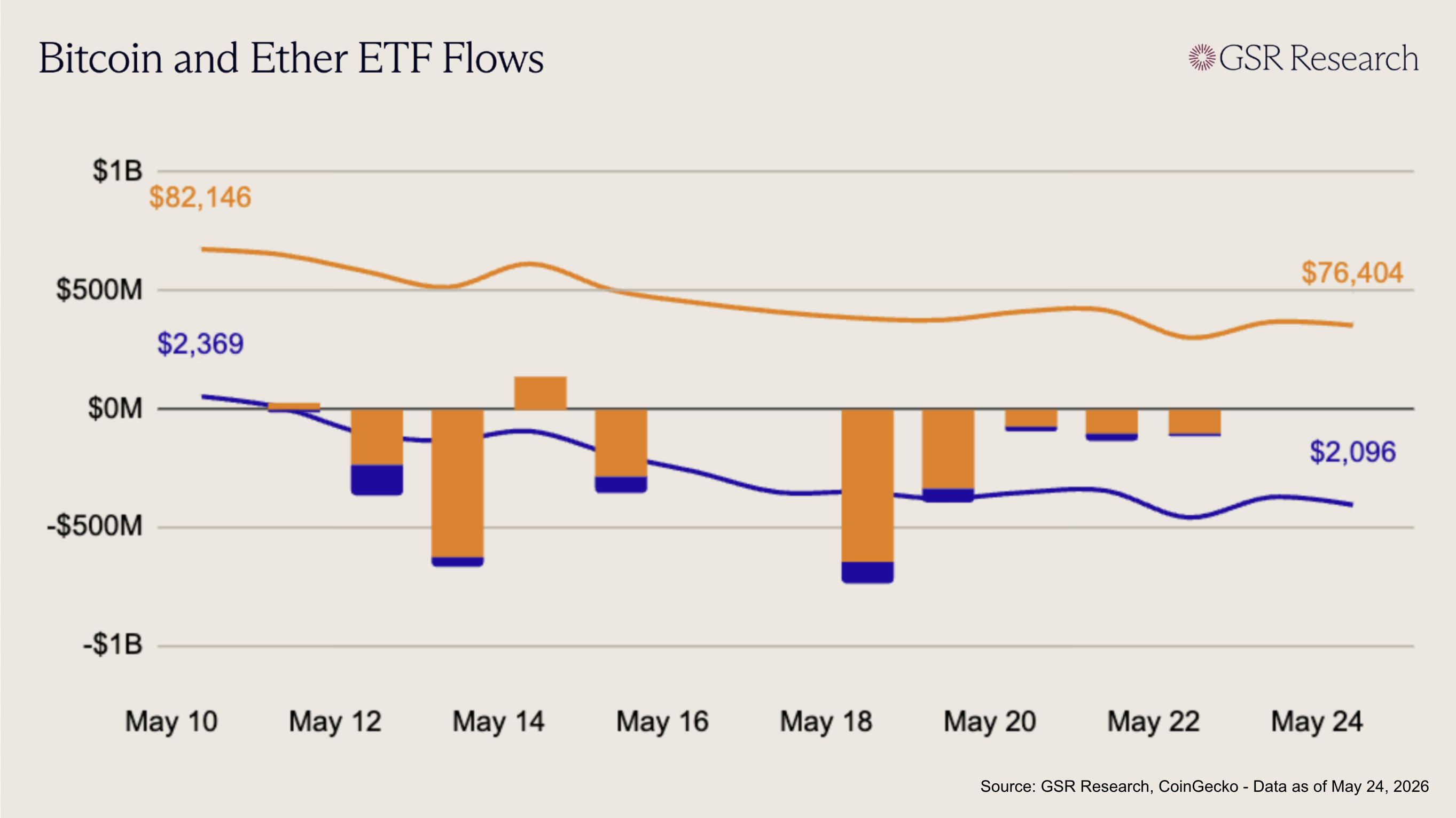

U.S. spot Bitcoin ETFs saw another decisively negative week, with outflows persisting across every session and no meaningful rebound to offset the drawdown. Redemptions started aggressively on May 18 (-$649M), driven primarily by heavy outflows from IBIT, ARKB, and FBTC, then continued on May 19 (-$331M) as IBIT alone shed more than $325M. While the pace of selling slowed midweek, flows remained negative on May 20 (-$71M), May 21 (-$101M), and May 22 (-$105M), showing that institutional demand failed to re-emerge even after the initial liquidation wave. Across the five sessions, BTC ETFs lost roughly -$1.26B, marking a clear continuation of the prior week’s risk-off positioning and one of the weakest weekly flow profiles in recent months.

Ether ETFs also remained under pressure, though the magnitude of selling was smaller than BTC. Flows were negative every day of the week, beginning with a sizable May 18 outflow (-$86M), followed by continued redemptions on May 19 (-$62M), May 20 (-$28M), May 21 (-$33M), and May 22 (-$7M). The selling was concentrated largely in ETHA and FETH, while secondary products provided little offsetting demand. Unlike prior weeks where ETH occasionally saw sharp but brief rebound inflows, this week offered no positive sessions at all, leaving total ETH ETF outflows at roughly -$216M.

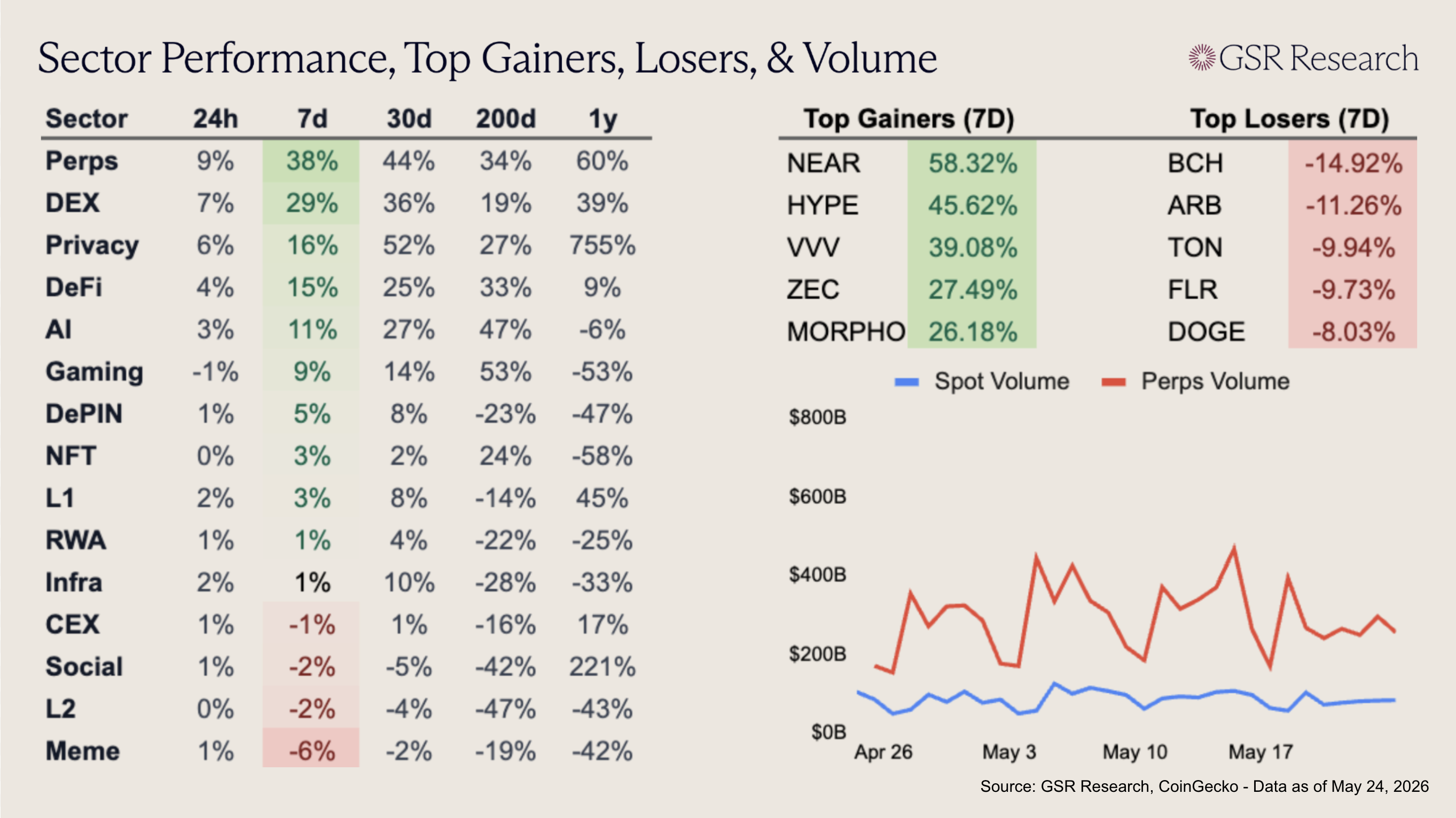

After the sharp selloff last week, alts have quickly rebounded, with many sectors up double-digit percentages. Perps were the category leader, up 38% thanks to rallies in HYPE (+45.62%) and Lighter (+25.3%). The two recent U.S. spot ETF listings, increased trading activity, as well as attention around TradeXYZ pre-IPO markets all contributed to HYPE’s recent move through $60. Hyperliquid’s rapid price appreciation ignited renewed interest in several other perp protocols, with Lighter, Aster, and Genius all rallying in tandem. Solely as a result of sharp rallies in perp protocol tokens, decentralized exchange projects took the number 2 spot on the week.

Despite two of the five top gainer spots belonging to AI projects, the category is only up 11% on the week. Rallies in Near (+58.32%) and Venice AI (+39.08%) were contrasted by selloffs in LINK (-3.7%), ICP (-2.9%), and KITE (-6.5%). The meme sector was hit the hardest this week, down 6% from top loser DOGE (-8.03%), as well as PEPE (-5.4%), and SHIB (-4.9%).

Click Here to Download The PDF of the Report

This material is provided by GSR (the “Firm”) solely for informational purposes. It is not intended to be advice or a recommendation to buy, sell or hold any investment mentioned. Investors should form their own views in relation to any proposed investment.

It is intended only for sophisticated, institutional investors and does not constitute an offer or commitment, a solicitation of an offer or commitment, or any advice or recommendation, to enter into or conclude any transaction (whether on the terms shown or otherwise), or to provide investment services in any state or country where such an offer or solicitation or provision would be illegal. The Firm is not and does not act as an advisor or fiduciary in providing this material.

This material is not an independent research report, and has not been prepared in accordance with any legal requirements by any regulator (including the FCA, FINRA or CFTC) designed to promote the independence of investment research.

This material is not independent of the Firm’s proprietary interests, which may conflict with the interests of any counterparty of the Firm. The Firm may trade investments discussed in this material for its own account, may trade contrary to the views expressed in this material, and may have positions in other related instruments. The Firm is not subject to any prohibition on dealing ahead of the dissemination of this material.

Information contained herein is based on sources considered to be reliable, but is not guaranteed to be accurate or complete. Any opinions or estimates expressed herein reflect a judgment made by the author(s) as of the date of publication, and are subject to change without notice. The Firm does not plan to update this information.

Trading and investing in digital assets involves significant risks including price volatility and illiquidity and may not be suitable for all investors. The Firm is not liable whatsoever for any direct or consequential loss arising from the use of this material. Copyright of this material belongs to GSR. Neither this material nor any copy thereof may be taken, reproduced or redistributed, directly or indirectly, without prior written permission of GSR.

Please see here for additional Regulatory Legal Notices relevant to US, UK and Singapore.