GSR Weekly Update - April 13th, 2026

BTC: $70,892 (+6.0%) | ETH: $2,185 (+6.4%) | BTC Dom: 57.0% | Global Cap: $2.49T

Last week Morgan Stanley gate-crashed the spot Bitcoin ETF market with the launch of its first crypto fund, the Morgan Stanley Bitcoin Trust (MSBT). The ETF tracks the CoinDesk Bitcoin Benchmark Settlement Rate and utilizes Coinbase for digital asset custody, with BNY serving as both custodian and transfer agent. Morgan Stanley enters an already crowded field, competing with institutional heavyweights like BlackRock and crypto-native firms such as Grayscale. However, MSBT has deliberately stood out due to its pricing, launching the fund with a notably low annual fee of 0.14%. This move undercuts every Bitcoin ETF currently on the market, including Grayscale Mini at 0.15%, Bitwise and VanEck at 0.20%, and BlackRock and Fidelity at 0.25%. More importantly, it resets the benchmark for what investors should expect to pay for Bitcoin exposure.

In commodity-like ETF markets, when a credible issuer lowers the fee floor, competitors are forced to justify their pricing, whether through deeper liquidity, stronger distribution, or clearer product differentiation. For crypto-native firms like Bitwise, that could mean directing a portion of fees toward open-source development, whereas institutional players like BlackRock can lean on extensive sales and distribution networks. Historically, however, the firm that captures early momentum tends to accumulate the largest share of assets under management.

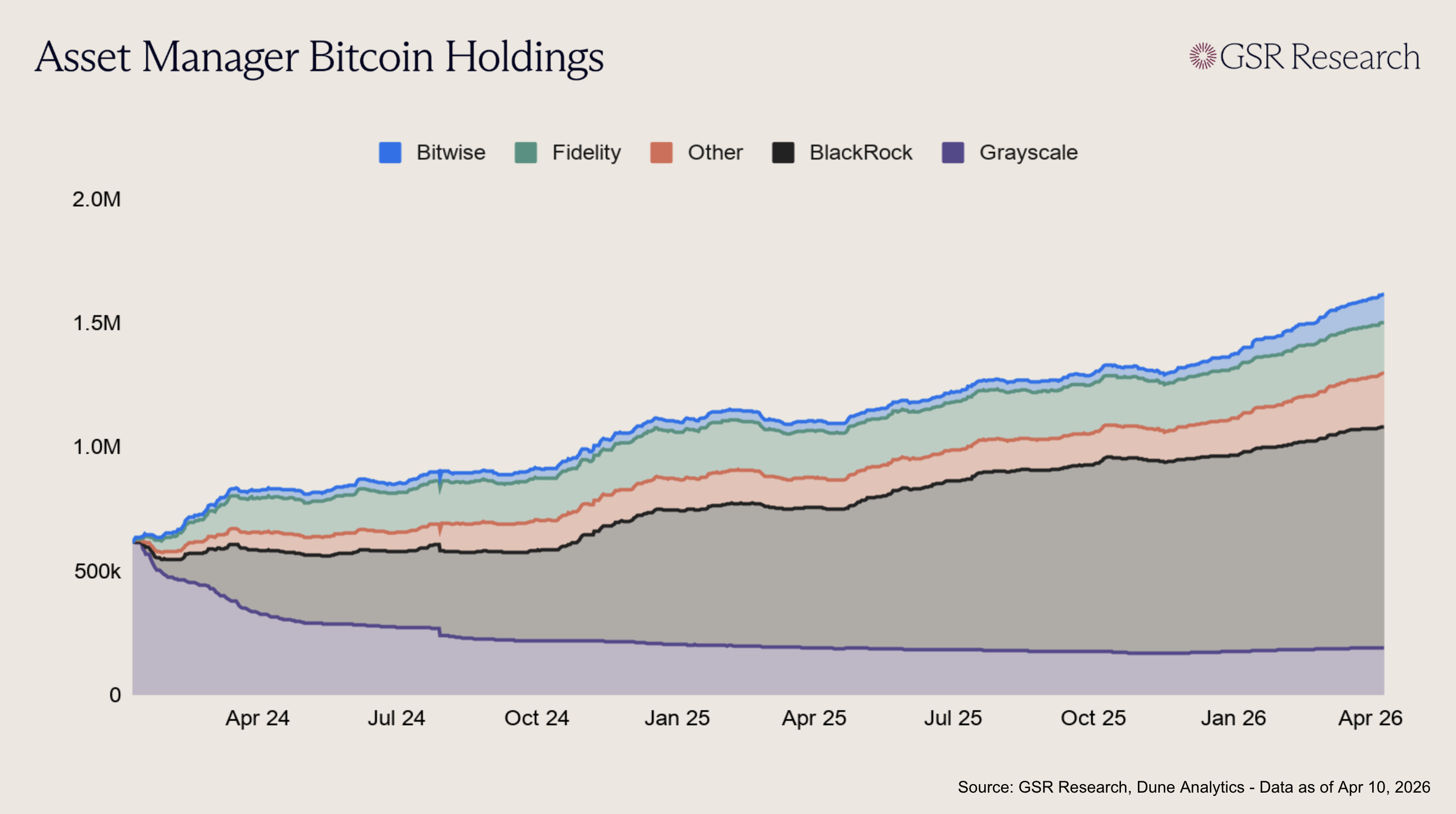

Since spot ETFs were approved in early 2024, asset manager holdings have grown from roughly 600,000 BTC to 1.5M+, making asset managers some of the largest BTC holders alongside corporate treasuries. While notional AUM has moved with Bitcoin’s price, underlying BTC holdings have climbed steadily.

Across BTC ETFs, BlackRock has emerged as the clear leader despite charging the highest fees. Fidelity has secured a strong second position, while Grayscale’s legacy trust (GBTC) has steadily shed BTC holdings and rotated capitalinto cheaper products. Still, even as GBTC holdings shrank, total ETF holdings continued to rise, indicating the category isn’t just reallocating a fixed pool of Bitcoin, but consistently attracting net new demand.

MSBT’s launch is unlikely to reshape the leaderboard overnight. BlackRock’s IBIT already exceeds $56B in assets, and that scale brings a liquidity and spread advantage. While the 11 bps fee gap versus MSBT matters for long-term holders, liquidity is also a real cost for large allocators. In the near term, Morgan Stanley’s pricing is more likely to compress fees across the category than to meaningfully erode BlackRock’s dominance. At 14 bps, a new clearing price for core Bitcoin beta is emerging.

Still, MSBT’s primary advantage is not its low cost, but the fact its issuer is a major, bank-affiliated asset manager with a large wealth platform and established distribution pipelines into advisory and intermediary channels. Unlike BlackRock, Morgan Stanley has over 16,000 financial advisors on its platform pushing this new product to market.

Morgan Stanley’s new fund arrives as Bitcoin is increasingly cemented as a portfolio asset on Wall Street. Over the past two years, the discussions around Bitcoin have shifted from questioning its legitimacy, to debating its utility in portfolios to now: determining what allocation is appropriate.

BlackRock has framed 1-2% as reasonable within a traditional 60/40 portfolio, while Morgan Stanley’s own guidance suggests 2-4% for more aggressive, growth-oriented investors. Fidelity and Bitwise have reached a similar conclusion from different angles: Bitcoin can enhance portfolio construction at low allocations, with Fidelity highlighting the impact of even small exposures and Bitwise’s research suggesting positions in the 2-3% range historically improving outcomes.

This underscores the importance of ETF wrappers. If institutional consensus is that Bitcoin belongs in small, risk-budgeted sleeves, implementation needs to be frictionless, auditable, liquid, and easy to rebalance. For most allocators, that makes ETFs much cleaner solutions than direct custody. Additionally, it makes fee compression more important than it first appears. When recommended allocations are only 1% to 4%, the product that offers the cheapest credible implementation is easier to defend in a model portfolio and easier to scale across a wealth platform.

The overarching question is where competition goes next. As spot Bitcoin exposure becomes cheaper and more standardized, differentiation is likely to shift away from plain beta and toward actively managed ETFs. The broader ETF market has already been moving in this direction, and crypto appears to be following the same path. Covered-call Bitcoin ETFs from firms like Global X, Grayscale, and Roundhill are early examples, not competing on purity of exposure but on reshaping Bitcoin’s volatility into income-oriented, portfolio-friendly outcomes. Morgan Stanley’s move could accelerate both trends at once by driving tighter fee compression in passive products and faster experimentation in active strategies.

Over time, the market is likely to split into two distinct camps: low-fee core products like MSBT that serve as foundational exposure, and higher-fee, actively managed ETFs for income generation, volatility management, and more tailored outcomes. This shift has the potential to turn digital assets from speculative trading tools into core portfolio sleeves by simplifying asset selection, incorporating yield sources like staking, and navigating cycles through active positioning. In practice, many investors are not looking for a market cap-weighted proxy dominated by Bitcoin. They are looking for more intentional exposure that better reflects how the crypto is actually used.

On April 6, Polymarket announced what it described as its biggest infrastructure change since launch. The upgrade includes a rebuilt trading engine, an upgraded CTF Exchange V2 smart contract with a new central limit order book, and support for EIP-1271, an Ethereum standard that allows smart contract wallets like Safe to sign orders directly on the platform. Alongside these changes, Polymarket is introducing a new collateral token called Polymarket USD, a 1:1 USDC-backed wrapper that replaces the bridged USDC.e the platform had been using on Polygon. The collateral migration is part of a trend that has been building over the past year of major crypto applications launching their own branded stablecoins.

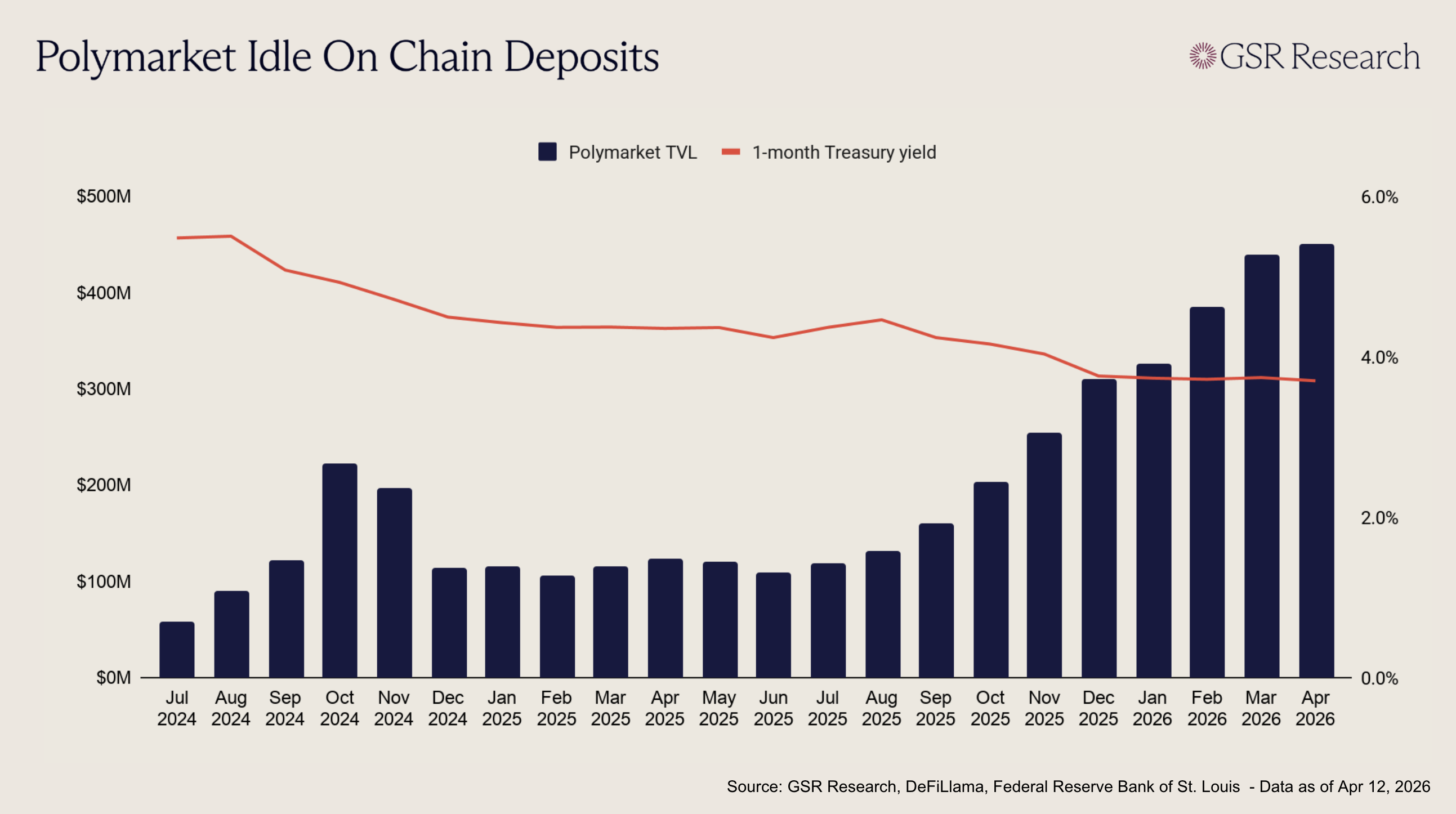

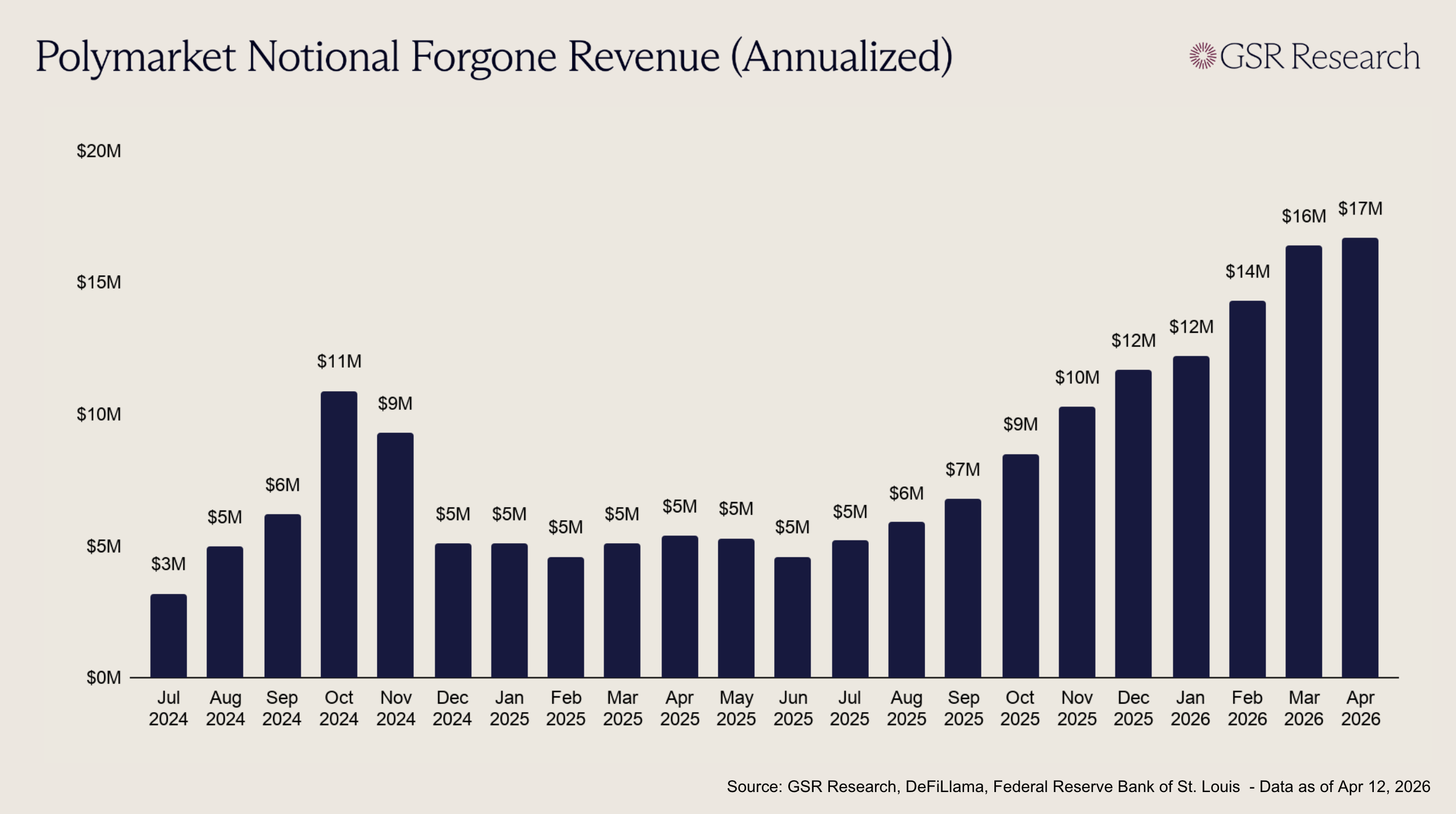

Polymarket USD is not a new stablecoin in any meaningful issuance sense. It is a thin wrapper around USDC, giving Polymarket direct control over settlement flows and collateral behavior without taking on the regulatory burden of reserve management. The immediate motivation is partly technical, as moving off bridged USDC.e eliminates dependency on Polygon's bridge infrastructure and the associated smart contract risk. However, the longer-term decision is driven by the platform’s economics. Polymarket has maintained a TVL that has averaged roughly $350 to $450 million over recent months, representing a substantial pool of idle USDC that generates interest for Circle rather than for the platform or its users. At a 4% annualized yield, that translates to somewhere between $14 and $18 million per year in forgone revenue. By wrapping deposits into its own token, Polymarket positions itself to capture a portion or all of that yield, whether through direct reserve management, revenue-sharing arrangements, or future integrations with yield-bearing infrastructure. That is yield that Polymarket could capture directly as revenue, or potentially pass on to users as rewards, mitigating their opportunity cost of locking up capital in a prediction market while awaiting its resolution.

Polymarket is far from the first platform to make this calculation. Hyperliquid launched USDH in September 2025 through a governance-driven process that saw proposals from the likes of Paxos, Ethena, and Agora before Native Markets ultimately won the ticker. Half of USDH's reserve yield is directed to Hyperliquid's Assistance Fund for HYPE buybacks. At the time of the announcement, Dragonfly partner Omar Kanji estimated that migrating Hyperliquid's roughly $5.5 billion in USDC deposits could redirect over $220 million annually away from Circle. Phantom launched its CASH stablecoin the same month as the foundation of a broader consumer payments product, built on Stripe's Open Issuance platform that allows businesses to create and manage their own stablecoins. MetaMask introduced mUSD through the same infrastructure. MegaETH launched USDm in partnership with Ethena, using reserve yield to subsidize sequencer operating costs rather than charging traditional sequencer fees. In each case, a platform with significant user deposits concluded that stablecoin economics should accrue to the application layer rather than the issuer.

The logic behind this trend is straightforward. If an application controls the user experience and stablecoins are simply sitting as collateral on the platform, the platform is effectively providing Circle or Tether with free, sticky deposits. For applications housing hundreds of millions in stablecoin deposits, the opportunity cost of not owning that yield is substantial, and wrapping USDC into a branded token is the simplest way to capture it.

The risk, however, is fragmentation. Each platform-branded stablecoin functions within its own domain but has limited utility outside of it. Polymarket USD is not accepted on Hyperliquid, USDH is not accepted on Polymarket, and users exiting any of these platforms must swap back into USDC or USDT before moving capital elsewhere. Those swaps require liquidity that may not always be deep or cheap, particularly for newer tokens with thin markets. Stablecoins derive much of their value from network effects. The more merchants, exchanges, and DeFi protocols that accept a given stablecoin, the more useful it becomes and the more users it attracts. A proliferation of app-specific tokens risks diluting those effects, creating a landscape where USDC and USDT remain the de facto standards for inter-platform settlement while branded tokens serve as captive collateral within individual applications. The question is whether any of these app-specific stablecoins can grow beyond their home platforms, or whether they will remain confined to the walled gardens where their issuers can compel usage.

The market is already responding to this coordination problem. Two weeks ago, The Better Money Company raised $10 million from a16z crypto to build a stablecoin clearinghouse that enables 1:1 swaps between compliant stablecoins at par, with guaranteed pricing and predictable settlement. Paxos, Bridge, MoonPay, MetaMask, and Phantom have all signaled intent to join the network. The clearinghouse model borrows directly from 19th-century American banking, when thousands of private banks each issued their own notes that were nominally worth a dollar but traded at varying discounts depending on the size, reputation, and distance from the issuing bank. Clearinghouses solved that problem by standardizing exchange. Whether a similar institution can scale fast enough to keep pace with stablecoin proliferation remains an open question, but the parallel is instructive, the last time the financial system faced this kind of fragmentation, the solution was not fewer issuers but better infrastructure connecting them.

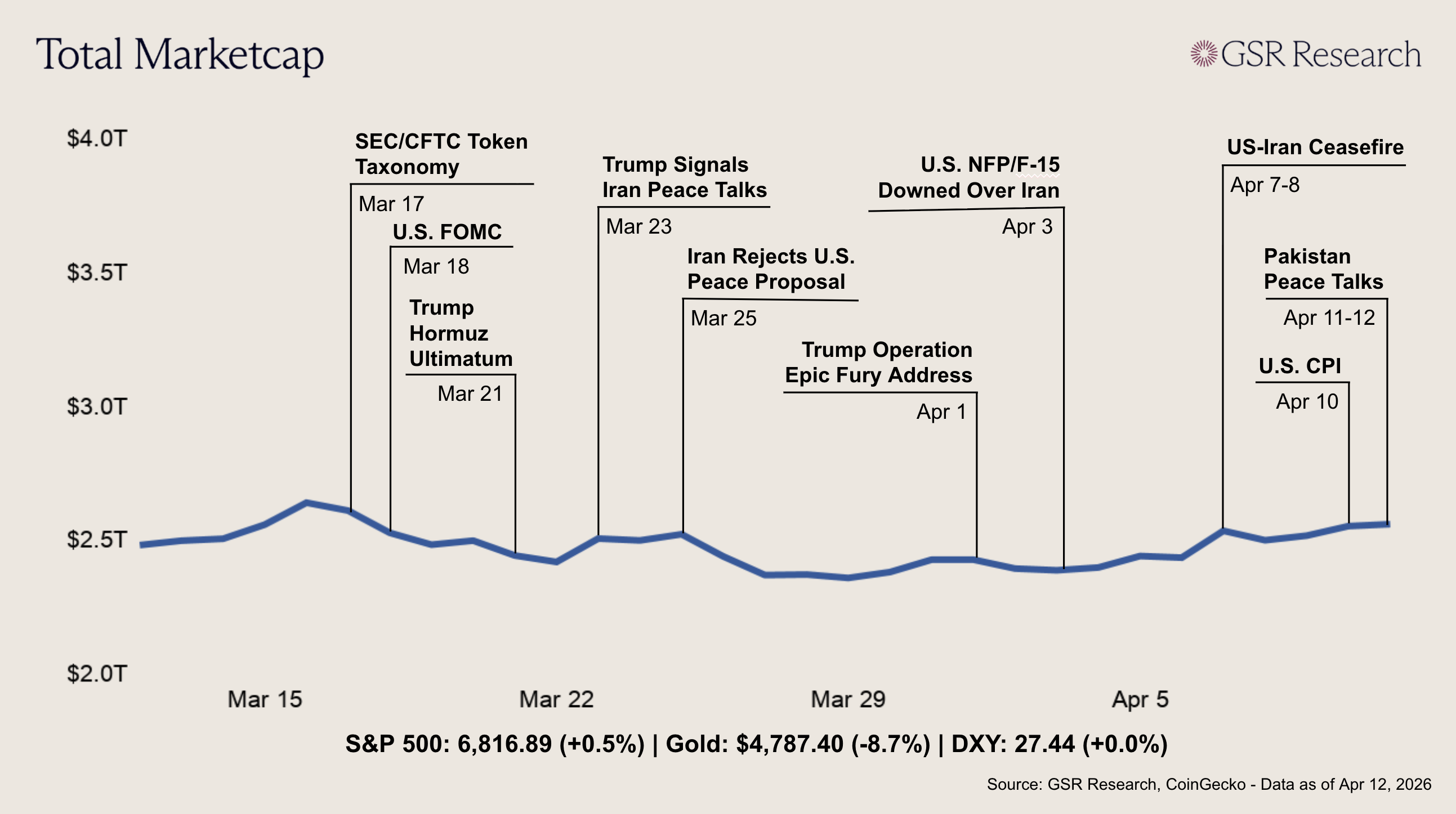

Crypto markets rallied early in the week on ceasefire euphoria before giving back most of the gains over the weekend as peace talks collapsed. The total crypto market cap opened near $2.39T, with BTC around $67,300. The turning point came Tuesday evening when the U.S. and Iran announced a two-week ceasefire brokered by Pakistan's Prime Minister, contingent on Iran reopening the Strait of Hormuz. Risk assets rallied across the board, BTC broke above $70,000 for the first time since March 26 and the S&P 500 gapped higher. Brent crude cratered roughly 15% in a single session to below $92, and the dollar index fell over 1% to a four-week low. However, the ceasefire's credibility was tested within hours as Netanyahu declared Lebanon excluded from the agreement and launched strikes on Hezbollah, prompting Iran to accuse the U.S. and Israel of violating three clauses. Despite the truce, actual Strait transit remained tightly controlled by the IRGC, with only around 17 vessels crossing daily versus roughly 130 before the war. Markets largely looked past the early cracks, and the S&P 500 closed the week at 6,817, up 3.9% for its best performance since November.

The week's economic data underscored the stagflationary environment building since the war began. FOMC minutes from the March meeting, released Wednesday, confirmed an 11-to-1 hold at 3.50-3.75%, with Governor Miran as the lone dissenter pushing for a cut. The minutes revealed a deepening tension, with several participants warning that higher energy prices could warrant renewed tightening while others argued a prolonged conflict could weaken the labor market. Some members raised the possibility of rate hikes for the first time since the easing cycle began in September 2024. Friday's March CPI provided the first real look at the war's inflationary impact, headline inflation jumped to 3.3% year-over-year from 2.4% in February, driven by a 10.9% spike in energy costs, though core CPI came in soft at 2.6% year-over-year, below the 2.7% forecast, suggesting the pressure remains concentrated in energy. Hours later, the University of Michigan's preliminary consumer sentiment reading plunged to a record low of 47.6, with one-year inflation expectations surging to 4.8%. The survey director noted that 98% of interviews were conducted before the ceasefire with respondents overwhelmingly concerned over the Iran conflict.

The rally unraveled over the weekend. Vice President Vance and a U.S. delegation traveled to Islamabad on Saturday for direct talks with Iran. By Sunday, Vance departed without a deal, citing Iran's refusal to commit to ending its nuclear weapons program. Hours later, Trump announced that the U.S. Navy would blockade all ships entering or leaving the Strait of Hormuz, later clarifying the action would target only vessels transiting to and from Iranian ports. With equity markets closed, crypto again served as one of the few liquid venues for expressing macro views. BTC dropped from above $73,000 to around $70,600, with $73 million in leveraged positions liquidated. Oil futures on Hyperliquid jumped 7%, with WTI registering $1.53 billion in volume to become the platform's third-most-traded instrument. By Monday morning, Brent had crossed back above $102 and S&P 500 futures pointed to declines of roughly 1%.

The coming week will be defined by the Hormuz blockade. How Iran responds to U.S. naval interdiction of its ports will determine whether the fragile ceasefire, set to expire April 22, survives or gives way to a new phase of escalation. Meanwhile, the IEA's coordinated emergency petroleum reserve releases, in place since the war began, are approaching their practical limits, with JPMorgan estimating that pre-closure barrels will be fully exhausted from the global supply chain by around April 20. If the Strait does not meaningfully reopen before those buffers run out, the supply gap could widen sharply, putting further upward pressure on oil and reinforcing the stagflationary dynamics that are keeping the Fed sidelined. Markets are pricing virtually no chance of a rate cut at the April 28-29 FOMC meeting, and attention is increasingly turning to whether the next move could be a hike.

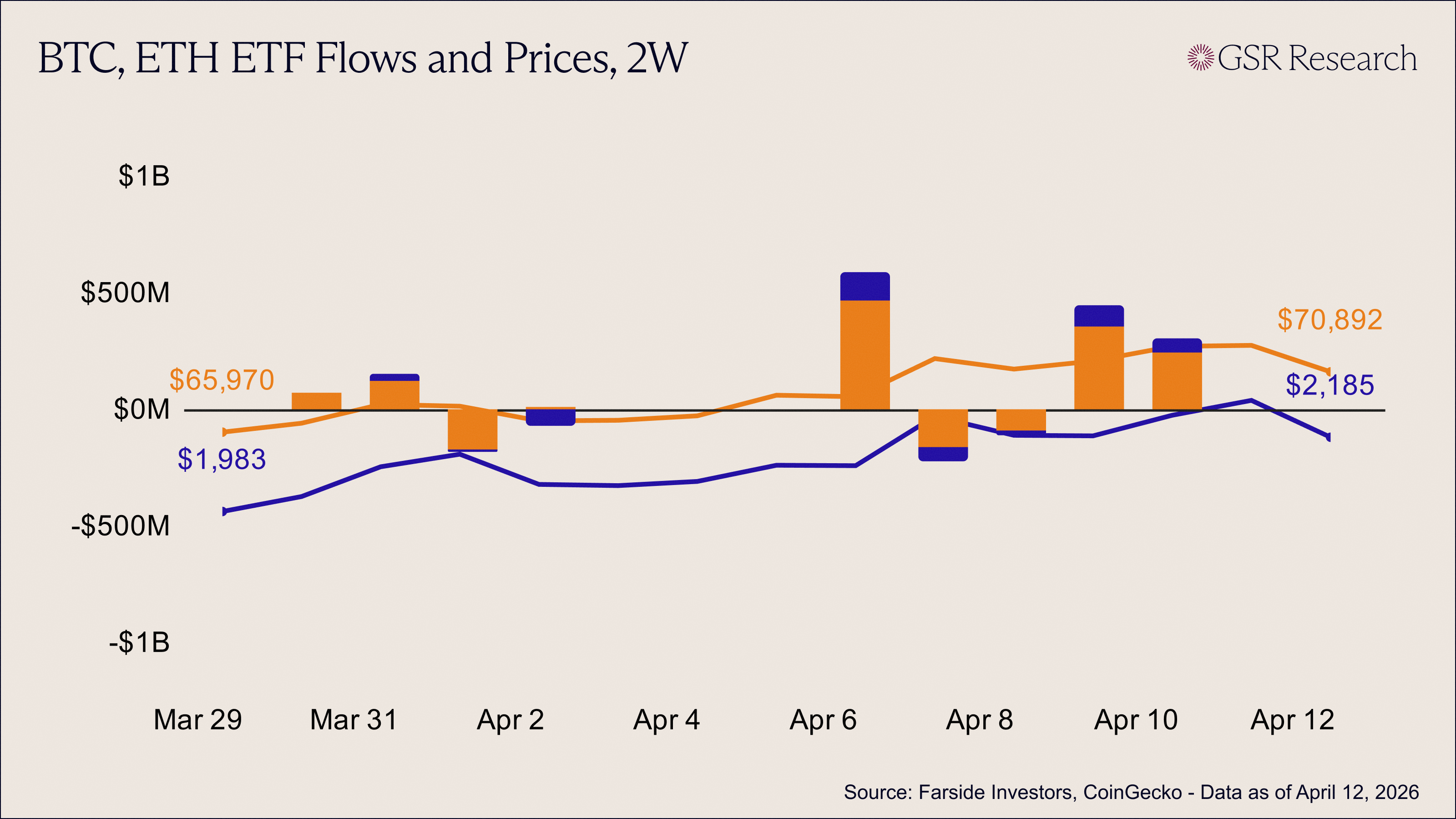

ETF flows this week marked a clear shift back toward strength after the choppy, indecisive conditions seen in the start of April. U.S. spot Bitcoin ETFs began the period on unstable footing, with outflows on Apr 7 (-$159M) and Apr 8 (-$94M), extending the prior week’s weakness. However, sentiment turned decisively midweek, with a sharp reversal on Apr 9 (+$358M) followed by another strong session on Apr 10 (+$240M), more than offsetting earlier redemptions and pushing the weekly net firmly positive. This rebound was broadly driven by renewed demand in IBIT and FBTC, with additional support from smaller issuers, signaling a return of institutional bid after the late-March liquidation phase.

Ether ETFs followed a similar trajectory but with more volatility and less consistency. After a strong inflow day on Apr 6 (+$120M), flows quickly reversed on Apr 7 (-$65M) and remained mixed through Apr 8 (-$19M). Like BTC, ETH saw a meaningful recovery into the back half of the week, with inflows returning on Apr 9 (+$85M) and Apr 10 (+$65M). Despite this rebound, the overall flow profile remained more fragile, with earlier losses only partially offset and continued evidence of uneven participation across issuers. Relative to BTC, ETH still appears more sensitive to shifts in sentiment, with less sustained follow-through on positive days.

Price action reflected the improving flow backdrop, particularly in the latter half of the week. Bitcoin rallied from $68.9k on Apr 6 to a peak near $73.1k on Apr 11 before pulling back slightly to $70.9k on Apr 12, marking a solid weekly advance before mild profit taking. Ether followed with a similar pattern, climbing from $2,108 to $2,285 at the highs before retracing to $2,185. While both assets benefited from renewed ETF inflows, the late-week pullback suggests that conviction remains somewhat tentative. Still, the ability to reclaim higher levels alongside strong inflow days points to improving market structure after the prior period of sustained outflows.

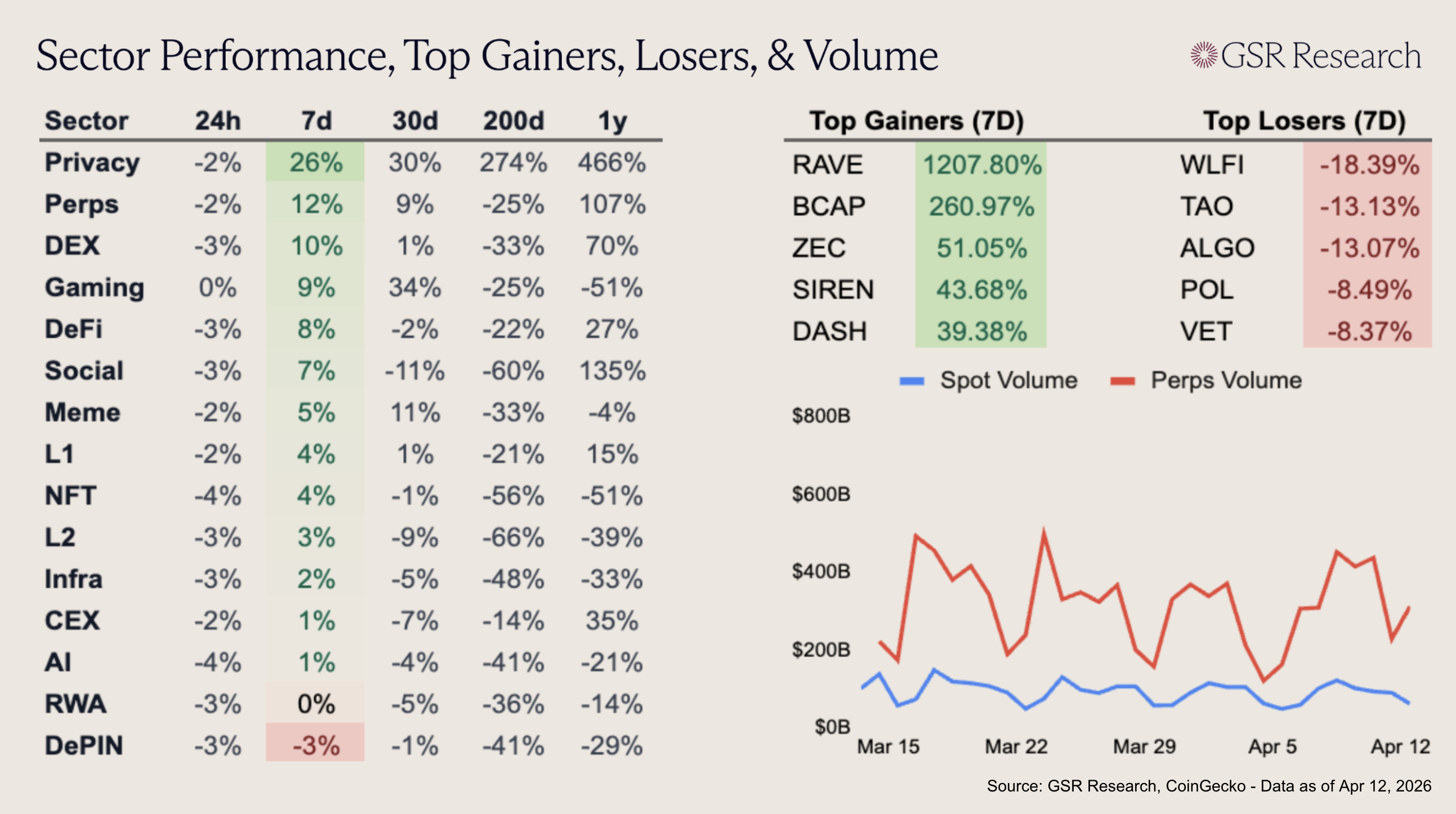

With a softening in broader macro conditions the altcoin sector gained this week, with almost all categories in the green. A renewed focus on data privacy, surveillance concerns, AI-driven tracking, and censorship-resistant assets drove capital rotation into the privacy sector this week, with Zcash rallying 51%. Perps are also double digits, as Hyperliquid and Lighter gained 13% and 11% respectively.

Bittensor was among the week’s worst performers, with the AI-focused network dropping 13%. Covenant AI, which operates 3 major Bittensor subnets including SN3 (Templar), announced they were leaving the network over a dispute with Bittensor co-founder Justin Steeves (known as “Const”). Templar fell from nearly $500M FDV to under $200M within a few hours of the announcement, with TAO selling off in Tandem.

Download the PDF of the full report here.

This material is provided by GSR (the “Firm”) solely for informational purposes. It is not intended to be advice or a recommendation to buy, sell or hold any investment mentioned. Investors should form their own views in relation to any proposed investment.

It is intended only for sophisticated, institutional investors and does not constitute an offer or commitment, a solicitation of an offer or commitment, or any advice or recommendation, to enter into or conclude any transaction (whether on the terms shown or otherwise), or to provide investment services in any state or country where such an offer or solicitation or provision would be illegal. The Firm is not and does not act as an advisor or fiduciary in providing this material.

This material is not an independent research report, and has not been prepared in accordance with any legal requirements by any regulator (including the FCA, FINRA or CFTC) designed to promote the independence of investment research.

This material is not independent of the Firm’s proprietary interests, which may conflict with the interests of any counterparty of the Firm. The Firm may trade investments discussed in this material for its own account, may trade contrary to the views expressed in this material, and may have positions in other related instruments. The Firm is not subject to any prohibition on dealing ahead of the dissemination of this material.

Information contained herein is based on sources considered to be reliable, but is not guaranteed to be accurate or complete. Any opinions or estimates expressed herein reflect a judgment made by the author(s) as of the date of publication, and are subject to change without notice. The Firm does not plan to update this information.

Trading and investing in digital assets involves significant risks including price volatility and illiquidity and may not be suitable for all investors. The Firm is not liable whatsoever for any direct or consequential loss arising from the use of this material. Copyright of this material belongs to GSR. Neither this material nor any copy thereof may be taken, reproduced or redistributed, directly or indirectly, without prior written permission of GSR.

Please see here for additional Regulatory Legal Notices relevant to US, UK and Singapore.