GSR Weekly Update - February 17th, 2026

BTC: $67,508 (-1.6%) | ETH: $1,955 (-3.3%) | BTC Dom: 56.4% | Global Cap: $2.39T

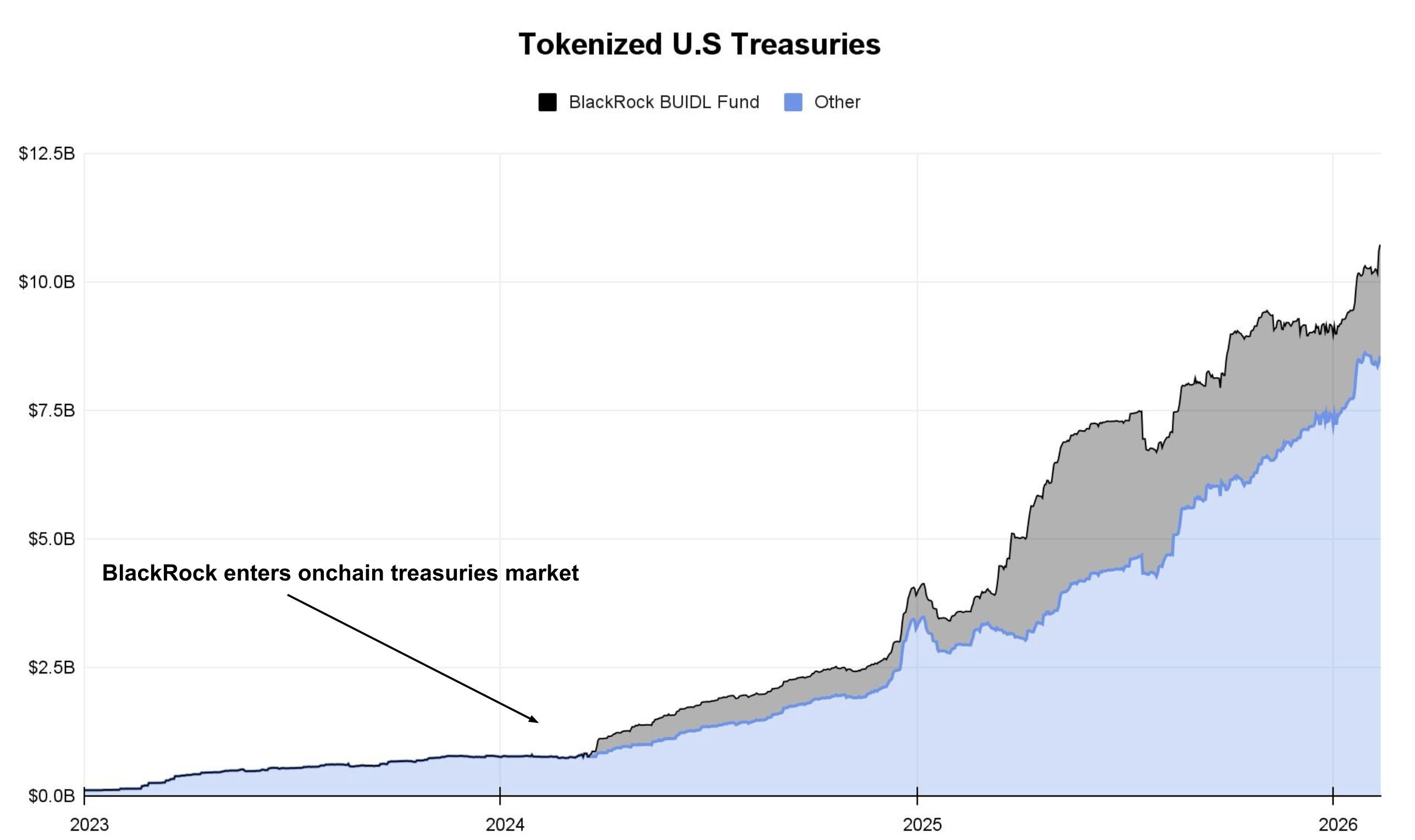

On Wednesday, BlackRock, Securitize, and Uniswap Labs announced the strategic integration of BlackRock’s tokenized money market fund, BUIDL, into UniswapX, enabling onchain trading for the fund. It was simultaneously revealed that BlackRock had purchased an undisclosed amount of Uniswap’s native token, UNI. This marks BlackRock’s biggest foray into DeFi yet, representing a major milestone for the fledgling trend of institutional DeFi adoption as the world’s largest asset manager has now formally entered the space.

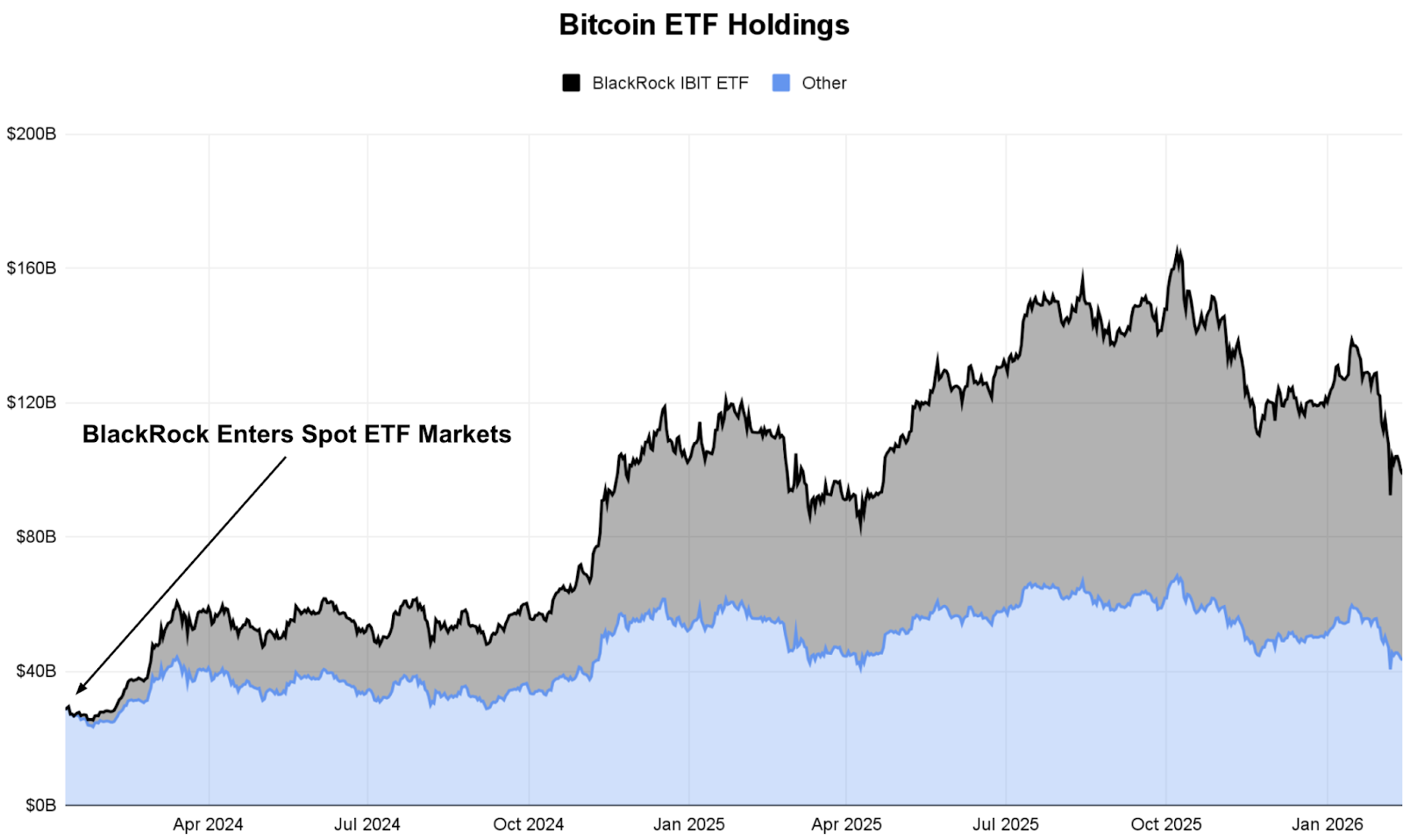

If we can draw any conclusions from BlackRock’s previous efforts in digital assets, it’s that the firm has been remarkably successful at identifying areas of growth and opportunity early. It has been extremely adept at timing its entrance and helping to drive explosive growth where it gets involved. When BlackRock first announced their entrance into the tokenized money market fund space with their BUIDL fund in early 2024, the total market sat at under $750M. Today, BlackRock’s BUIDL fund alone manages more than $2B. In less than 2 years, the tokenized money market space has increased more than 14x and sits close to $11B AUM. The same story applies to US spot Bitcoin ETFs. BlackRock entered the market as soon as ETF trading was approved for Bitcoin in January 2024. Since then, total ETF AUM has climbed from $25B to over $100B in roughly 2 years, with BlackRock’s IBIT leading the charge having accumulated more AUM than all of its competitors combined.

Source: RWA.xyz - Data as of Feb 16, 2026

Source: Dune Analytics - Data as of Feb 16, 2026

While it’s too early to tell whether institutional DeFi will follow the same trajectory, BlackRock’s involvement is at the very least a highly encouraging sign. Institutional DeFi as a narrative has been around for some time, but attempts in this area have never quite gotten meaningful adoption. Early efforts date back to Aave’s permissioned Arc protocol, which launched in early 2022, but failed to gain traction. We’ve seen numerous other experiments and pilots over the years. One includes the Monetary Authority of Singapore’s ‘Project Guardian’, where the likes of JPMorgan, DBS Bank, and SBI Digital trialed the use of permissioned versions of Uniswap and Aave. In another example, Societe Generale’s digital asset unit FORGE borrowed DAI from MakerDAO by putting up tokenized bonds as collateral. However, most of these have been one-off proofs of concept, with very little in the way of enduring initiatives.

We began seeing some more dedicated efforts in 2025, amidst a more welcoming regulatory environment. In one notable instance, Apollo Global Management partnered with Morpho and Drift to integrate its tokenized private credit ACRED fund into DeFi lending markets, enabling holders to use it as collateral to borrow USDC and add leverage to their positions. Also worth mentioning is Plume’s launch of its RWA-focused layer 2, which bakes compliance into the protocol and allows tokenized funds from the likes of Wisdom Tree, Hamilton Lane, and Invesco, among others, to be used in DeFi across DEXs, lending markets, and vaults. Despite these efforts, institutional DeFi activity remains relatively muted.

BlackRock’s emphatic entry into the space thus comes at a time when the sector is struggling to find its footing. Hopes are high that the asset management giant’s efforts can help it get off the ground. BlackRock’s purchase of UNI tokens is a promising sign of conviction, marking one of the first times a company of its stature purchases a crypto token outside of the majors, and signaling that the company is willing to have a direct financial stake in the DeFi ecosystem. Just days after the BlackRock and Uniswap announcement, Apollo Global and Morpho announced they entered into a cooperation agreement whereby they will collaborate to support Morpho’s lending markets. The partnership also contains a provision for Apollo to acquire up to 90 million MORPHO tokens over the course of 4 years, representing 9% of Morpho’s total supply and roughly $125M at current prices. In just a week, then, we saw two significant incursions into DeFi from major institutional players, going beyond mere proofs of concept through the commitment of capital and skin in the game. We’re optimistic they could catalyze a new chapter of growth for the space.

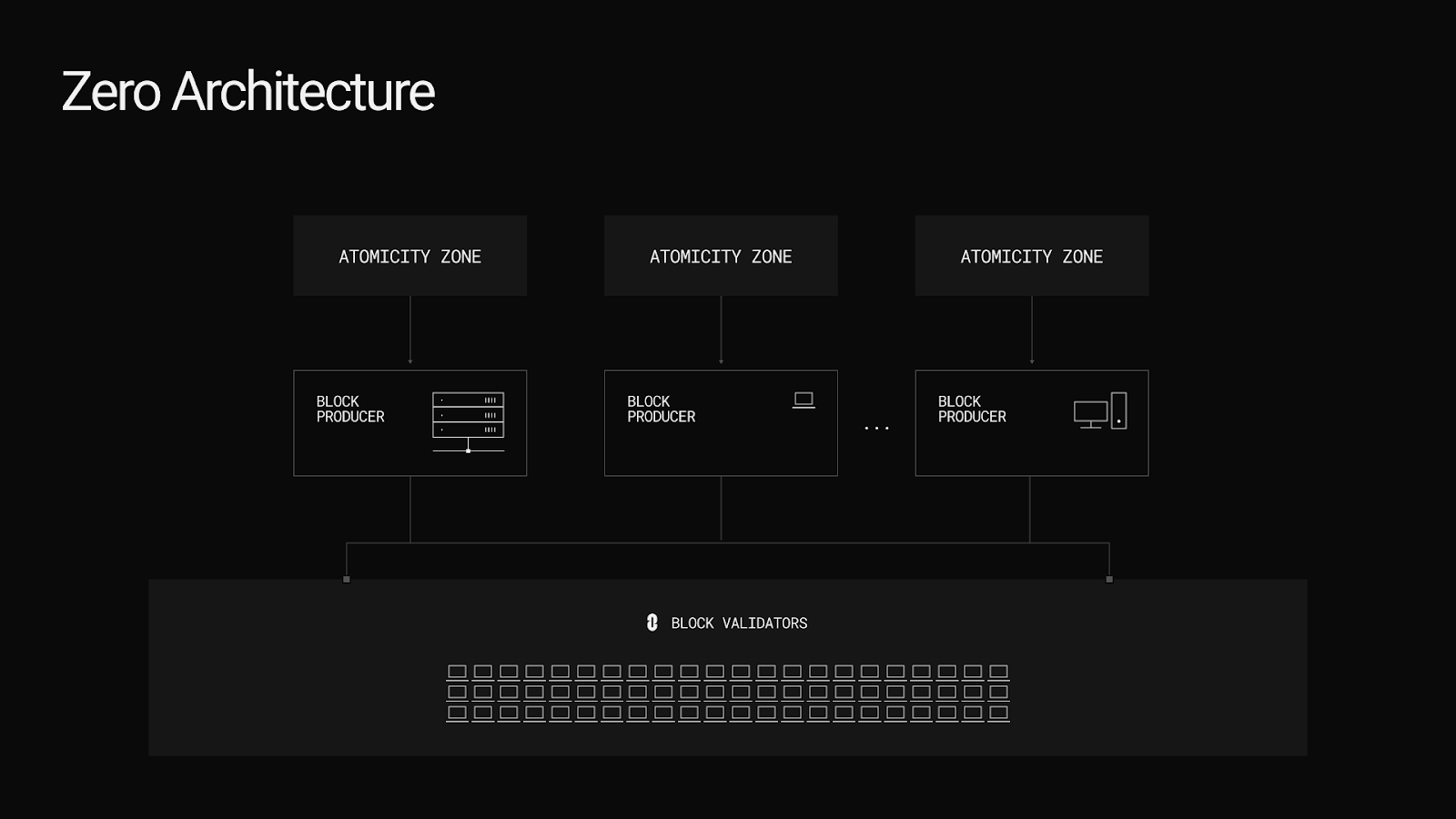

In a surprising move for a chain-agnostic interoperability protocol, Layer Zero announced its plans to launch a new layer 1 blockchain called Zero. The team said it’s been working on the project in stealth over the past two and a half years, and they expect to launch the chain in fall 2026. Layer Zero also announced an impressive list of partners and investors that have signed up to collaborate with and support the project. Ark Invest and Citadel Securities made strategic investments, notably acquiring the protocol’s ZRO token, and the likes of Google Cloud, DTCC, and Intercontinental Exchange are partnering with the team as they expand their efforts in blockchain technology and asset tokenization.

Despite the impressive list of partners and the remarkable performance figures touted for the new chain, the industry’s response was mixed amidst generalized infrastructure fatigue. As the industry clamors for more useful apps and less undifferentiated blockspace, many wonder whether another layer 1 blockchain is truly what the industry needs. While understandable, this attitude risks ignoring what could turn out to be genuinely important technical progress by Layer Zero, which could help move the entire industry forward.

Zero’s architecture is highly reminiscent of the high-level architecture that Vitalik Buterin and others at the Ethereum Foundation have described for the end state of Ethereum. This is notable because many in the Ethereum ecosystem view this design as the ideal end state architecture for public blockchains, one that can overcome the tradeoff between scalability and decentralization. Importantly, while Ethereum expects to transition to this architecture over the next 4 years or so, Zero is set to deploy a production-grade implementation as soon as this fall.

The key element that enables this new blockchain architecture is zero-knowledge (ZK) proof technology. ZK proofs can help reduce the amount of work that nodes in a blockchain network have to do to validate blocks of transactions. Instead of having all nodes re-execute all transactions to verify their correctness, ZK proofs allow one node to do the execution and create a succinct cryptographic proof of its correctness that other nodes can easily verify.

Blockchains have long faced a tradeoff between scalability and decentralization since they can roughly only be as fast as their slowest validating node. Because of this, high-performance chains tend to impose high hardware requirements on nodes. However, this restricts the scope of who can participate. On the other hand, chains that prioritize decentralization keep node requirements low, but this limits what they can achieve in terms of transaction throughput.

ZK allows chains to have their cake and eat it too, as it were, by letting them have powerful block-producing nodes processing large volumes of transactions and generating proofs for them, while much weaker nodes can still verify those proofs and keep the block-producing nodes in check. This enables ZK blockchains to achieve both scalability and decentralization.

Source: Layer Zero

A blockchain architecture baking ZK into its base layer only started becoming practical in the last year or so, when zkVMs began breaking the ‘real-time’ proving barrier: generating proofs for Ethereum blocks within the blockchain’s 12 second block time. Today, multiple teams including Axiom, Brevis, Matter Labs, Succinct, and Zisk achieve average block proving times of 7-9 seconds in multi-GPU clusters, and are working on further reducing proving times, especially for worst case blocks. While results haven’t yet been publicly benchmarked, Layer Zero claims to have significantly improved the state of the art here with their in-house Jolt Pro zkVM, which they claim is orders of magnitude more performant than existing competitors. This leap, combined with innovations across data availability, state storage, and parallel execution allow Zero to target low single-digit millions of transactions per second in throughput. Absent real-world performance benchmarks, such claims should be taken with a degree of caution. If they hold up, however, even at a fraction of the performance claimed, it would represent a remarkable achievement.

If the innovations embedded in Zero deliver at the level Layer Zero claims, they could genuinely represent a leap forward for the industry. Furthermore, the great benefit of open source software is that these innovations can help the industry as a whole level up by learning from Layer Zero’s efforts and adopting the technology. If Zero can deliver on the vision of the Ethereum roadmap four years ahead of schedule, the industry might finally be able to look past scalability as a significant challenge for adoption.

Source: CoinGecko, GSR - Data as of Feb 16, 2026

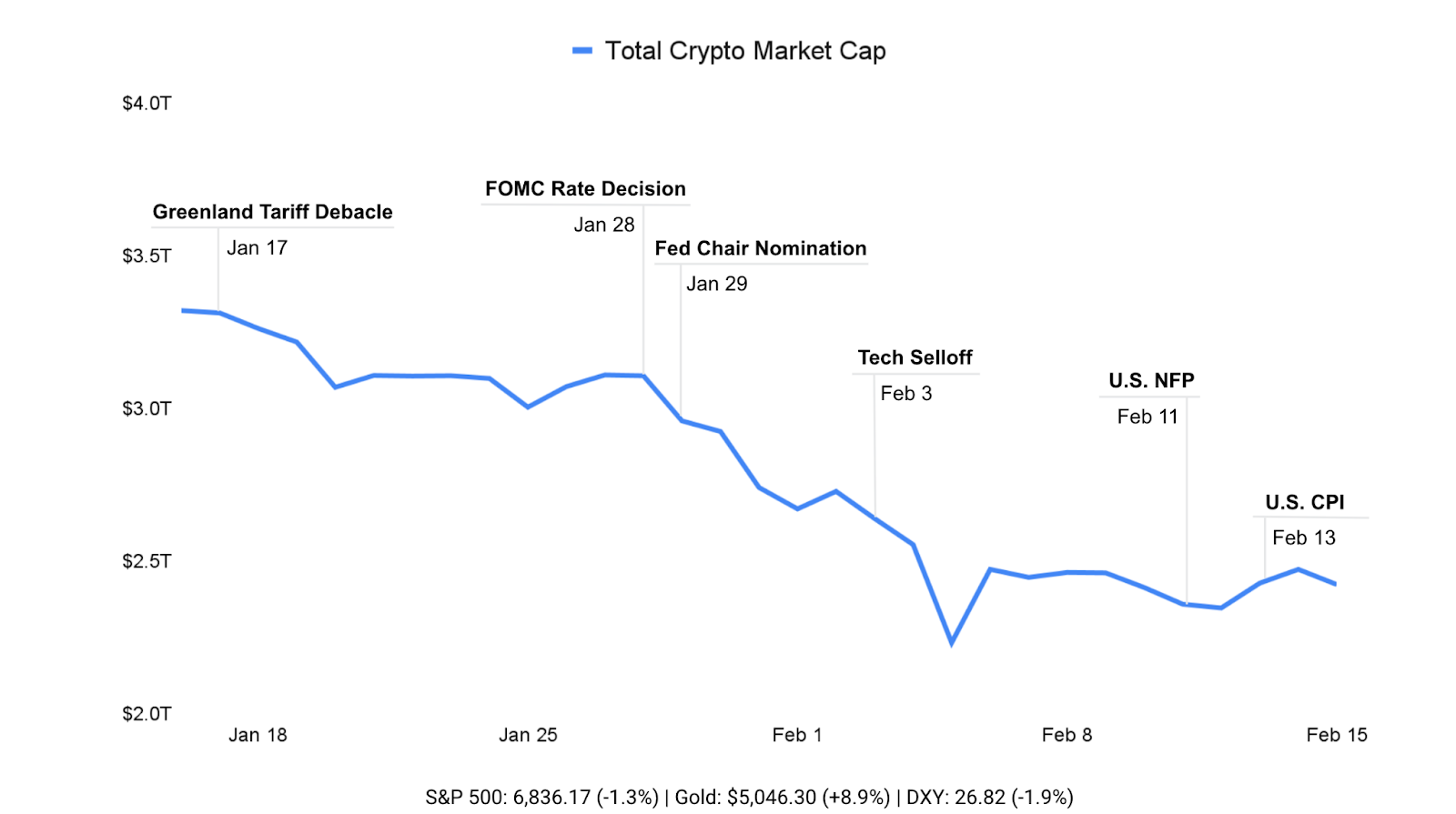

After the previous week’s violent liquidation cascade and snapback, crypto markets spent the past week in a consolidation phase. The total crypto market cap held near the $2.4T level, with drawdowns proving shallower than the early-February washout, but with rallies still struggling to reclaim the $2.5T level. Traditional markets told a similar story: equities closed the week lower amid renewed tech volatility, while defensive positioning stayed firm with gold hovering near recent highs and the dollar modestly weaker.

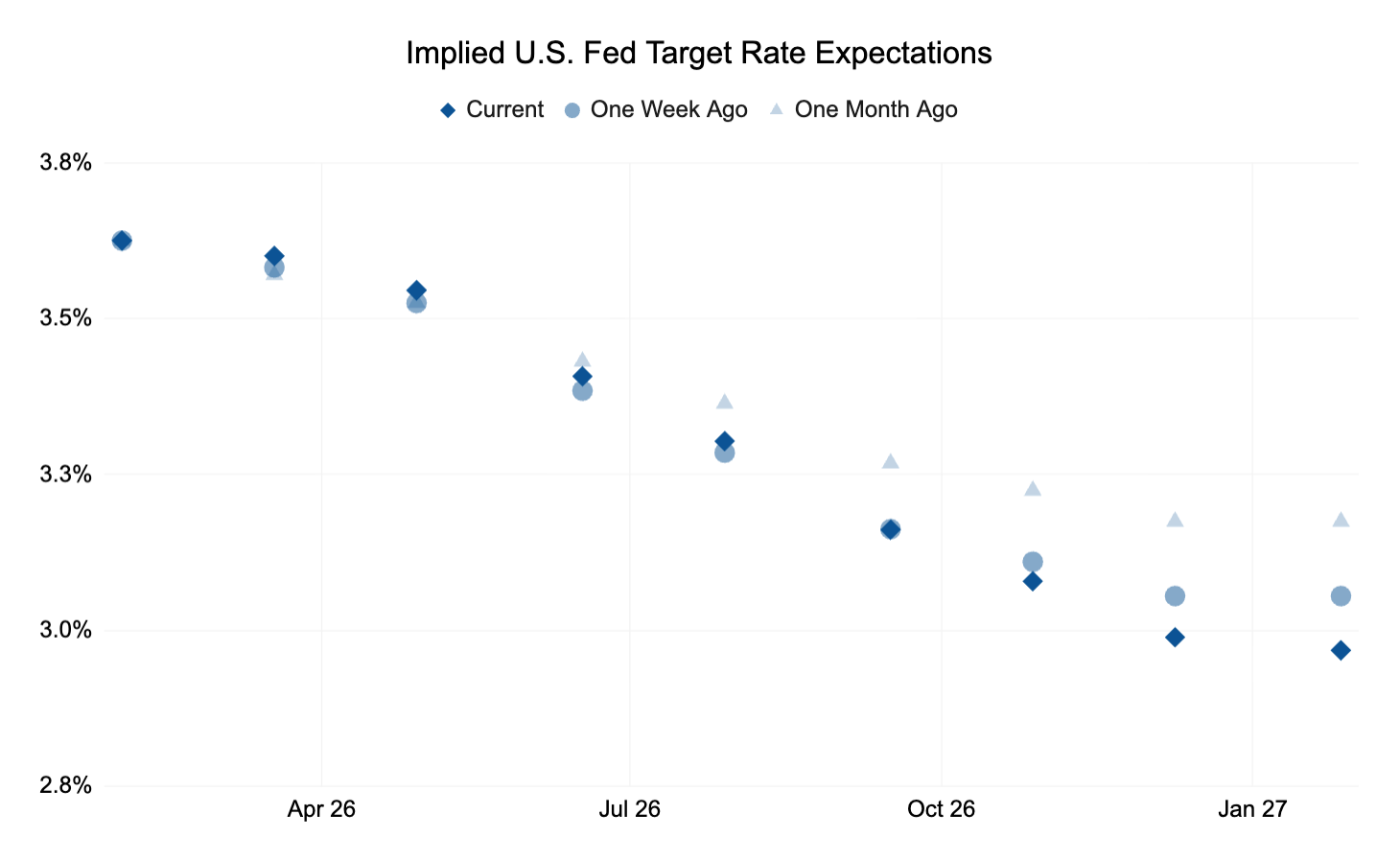

The macro spotlight shifted to data releases, with markets recalibrating rate expectations on each print. The delayed January employment report surprised to the upside, with nonfarm payrolls rising 130,000 versus expectations around 70,000 and the unemployment rate printing 4.3%. Wage growth also remained firm, with average hourly earnings up 0.4% MoM. The combination was enough to push yields higher and reduce the market’s near-term conviction around Fed easing, prompting another round of cautious de-risking across high beta exposures.

Source: CME Fedwatch, GSR

Two days later, however, the January CPI report offered some relief. Headline CPI slowed to 2.4% YoY from the previous month’s 2.7%, and below the expected 2.5%. The cooler print briefly revived risk appetite and helped stabilize broader markets, but follow-through remained limited as “SaaSpocalypse” concerns and earnings-driven tech volatility resurfaced.

Based on the balance of the two macro prints, Fed target rate expectations based on Fed Funds futures now show a slightly increased likelihood of higher rates in the near term compared to expectations last week and a month prior, but an expectation of lower rates toward the end of 2026 and beginning of 2027.

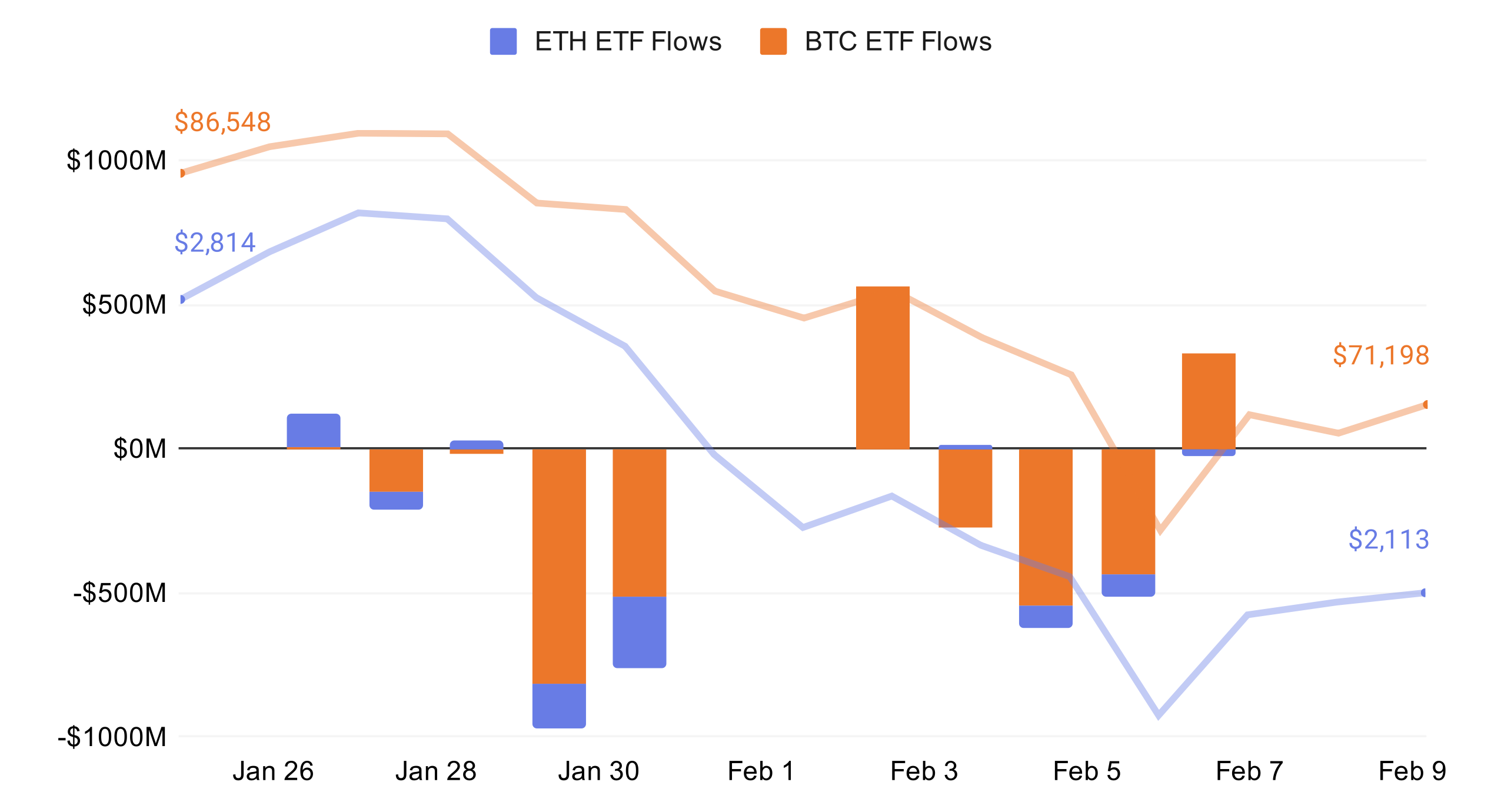

Source: Farside Investors, CoinGecko - Data as of Feb 16, 2026

ETF flows echoed an overall cautious posture. U.S. spot Bitcoin ETFs started the week with two sessions of net inflows (+$145m on Feb 9 and +$167m on Feb 10), but saw heavy redemptions around the macro prints (-$276m on Feb 11 and -$410m on Feb 12), leaving the week modestly negative at roughly -$360m. Ether ETF flows followed a similar arc, swinging from early-week inflows (+$57m and +$14m) to mid-week outflows (-$129m and -$113m), for a net -$161m across the five trading sessions. Against that backdrop, BTC drifted from ~$71.2k to ~$67.5k (-5.2% WoW), failing to hold a brief push back toward $70k, while ETH continued to lag, sliding from ~$2,113 to ~$1,955 (-7.5% WoW) and struggling to sustainably reclaim the $2,000 level.

Source: CoinGecko, GSR - Data as of Feb 16, 2026

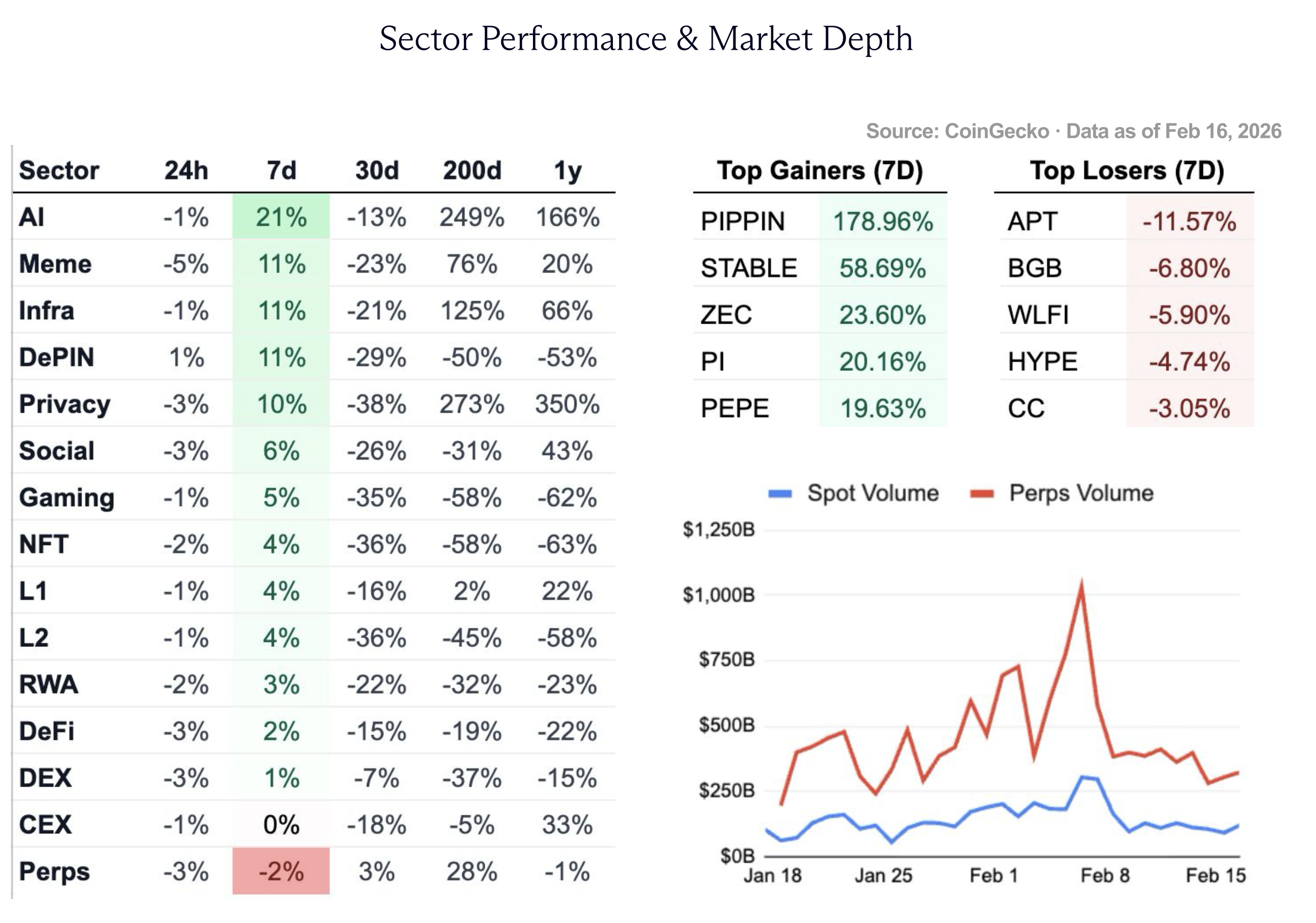

Despite the choppy week for crypto markets, several sectors had a positive performance overall. AI was the top performing sector, with notable rallies for Bittensor (+14.4%) and Render (+6.5%). On the privacy side, Zcash rebounded 24% after its sharp drawdown last week.

Despite Aster being up 16% on the week, the perps sector performed the worst over the last 7 days, driven almost entirely by a 5% decline in the price of HYPE. Hyperliquid’s token performance has cooled somewhat after the 10% increase the previous week that was driven by the announcement of HIP-4 markets.

On the subject of perps, volumes have stabilized after the frenzy of liquidations in early February. Both perps and spot volumes were relatively subdued and stable for the week, with no notable spikes in activity.

This material is provided by GSR (the “Firm”) solely for informational purposes. It is not intended to be advice or a recommendation to buy, sell or hold any investment mentioned. Investors should form their own views in relation to any proposed investment.

It is intended only for sophisticated, institutional investors and does not constitute an offer or commitment, a solicitation of an offer or commitment, or any advice or recommendation, to enter into or conclude any transaction (whether on the terms shown or otherwise), or to provide investment services in any state or country where such an offer or solicitation or provision would be illegal. The Firm is not and does not act as an advisor or fiduciary in providing this material.

This material is not an independent research report, and has not been prepared in accordance with any legal requirements by any regulator (including the FCA, FINRA or CFTC) designed to promote the independence of investment research.

This material is not independent of the Firm’s proprietary interests, which may conflict with the interests of any counterparty of the Firm. The Firm may trade investments discussed in this material for its own account, may trade contrary to the views expressed in this material, and may have positions in other related instruments. The Firm is not subject to any prohibition on dealing ahead of the dissemination of this material.

Information contained herein is based on sources considered to be reliable, but is not guaranteed to be accurate or complete. Any opinions or estimates expressed herein reflect a judgment made by the author(s) as of the date of publication, and are subject to change without notice. The Firm does not plan to update this information.

Trading and investing in digital assets involves significant risks including price volatility and illiquidity and may not be suitable for all investors. The Firm is not liable whatsoever for any direct or consequential loss arising from the use of this material. Copyright of this material belongs to GSR. Neither this material nor any copy thereof may be taken, reproduced or redistributed, directly or indirectly, without prior written permission of GSR.

Please see here for additional Regulatory Legal Notices relevant to US, UK and Singapore.