GSR Weekly Update - February 23rd, 2026

BTC: $67,272 (-2.6%) | ETH: $1,938 (-3.6%) | BTC Dom: 56.6% | Global Cap: $2.38T

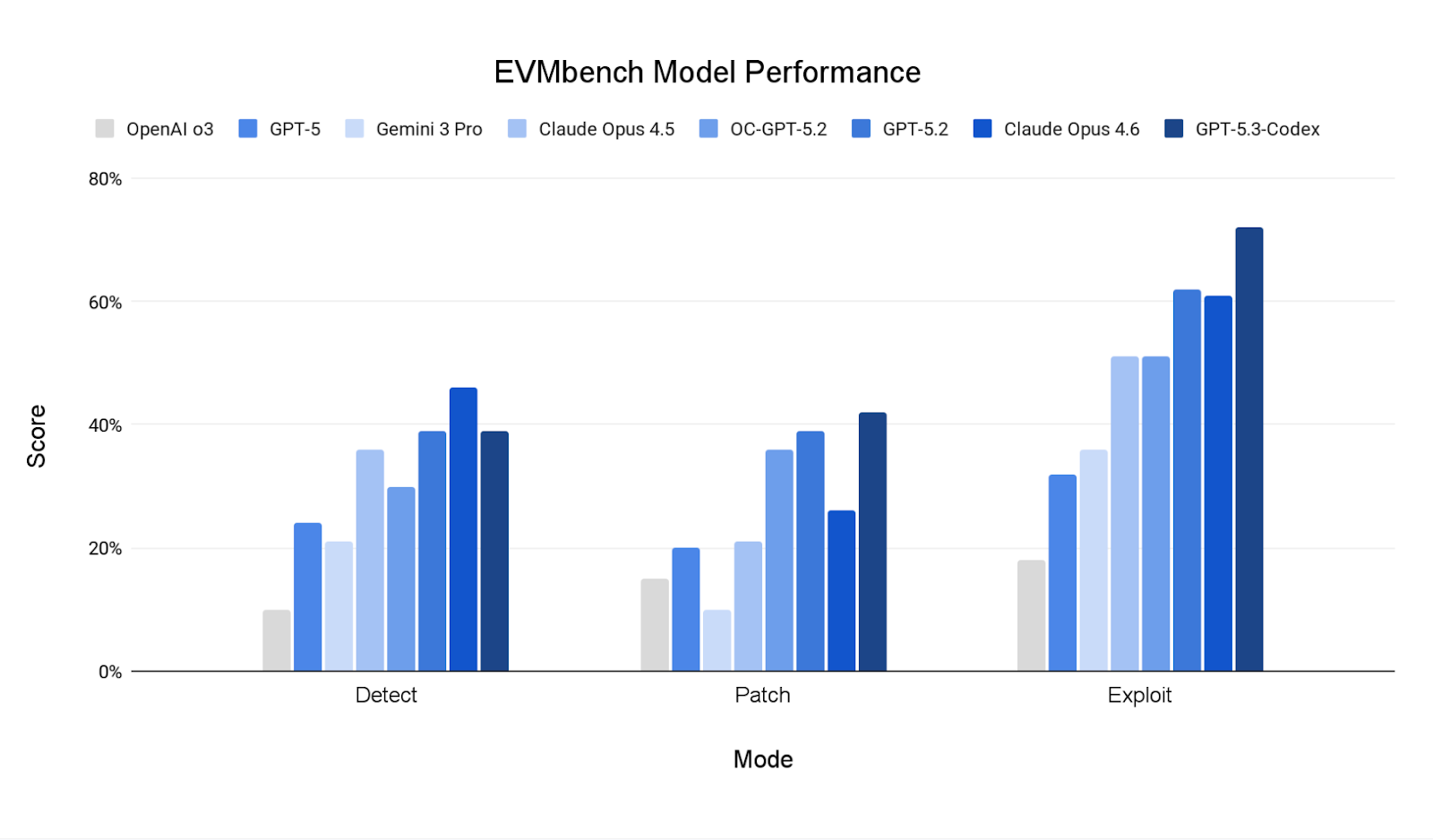

On Wednesday, OpenAI and Paradigm jointly unveiled EVMbench, an evaluation framework that tests AI agents on their ability to detect, patch, and exploit high-severity smart contract vulnerabilities. The benchmark draws on 120 curated vulnerabilities from 40 real-world audits, most sourced from Code4rena auditing competitions, and places AI agents in containerized blockchain environments where they must demonstrate security skills. The results are striking: GPT-5.3-Codex can now successfully exploit over 70% of the critical, fund-draining bugs in the benchmark, up from less than 20% when the project began. With smart contracts currently securing close to $100B in crypto assets, EVMbench marks an important milestone in the accelerating convergence of AI and blockchain security.

Security has long been one of crypto's biggest challenges. The industry lost an estimated $3.4B to hacks and exploits in 2025. Unlike traditional software, smart contracts are often immutable once deployed, meaning even minor coding errors can result in permanent, irrecoverable financial losses. The sector has relied on a combination of manual audits, bug bounties, and formal verification to mitigate these risks, but the process remains expensive, time-consuming, and imperfect. Many critical vulnerabilities continue to slip through.

This is where AI-powered security tooling holds great promise. Automating the process of detecting and patching vulnerabilities could both greatly reduce the cost of auditing and securing smart contracts, while also expanding security coverage ensuring more bugs are detected and fixed. Such tooling could greatly enhance the security of the ecosystem overall.

We’ve already begun to see early signs of this positive impact from AI on crypto security. For example, crypto auditing outfit Cantina recently rolled out an AI ‘Code Analyzer’, which it claims has helped secure over $25B in funds. OpenAI and Paradigm’s EVMbench represents another step forward in this direction. The existence of benchmarks often helps guide and accelerate model improvements with a clear goal in sight. EVMbench now helps provide model and agent companies with an objective measuring stick they can use to improve their capabilities in a high-impact area for crypto.

Source: OpenAI and Paradigm

Unfortunately, EVMbench also illustrates the double-edged nature of AI-powered coding in blockchain security. Across the three capabilities that models were tested in, ‘exploit’ was the one they were consistently the most adept at, ahead of ‘detect’, and ‘patch’. That is, the models were more effective at exploiting smart contract vulnerabilities and draining funds than they were at finding vulnerabilities in the first place, or fixing them. This highlights the strong offensive capabilities of current models, which appear to be stronger than their defensive ones. Regrettably, this empowers attackers today, enhancing their abilities to exploit existing vulnerabilities. It’s widely suspected that many recent exploits have been aided by AI tools, and it’s likely this will continue to occur or accelerate into the near future. The situation could be further worsened by imperfect AI tools being used to generate code, which could inadvertently introduce more vulnerabilities. It is likely that AI may overall make the security situation for blockchains worse in the near future, before it makes it better.

The flipside is that, looking further ahead, advances in AI reasoning may unlock far more powerful security capabilities. Reinforcement learning has dramatically improved AI's capacity for the kind of rigorous, step-by-step logical reasoning that security analysis requires. AI models have recently become exceptional at math, having improved at an incredible rate given they struggled with basic arithmetic just a couple of years ago. The likes of OpenAI, Google’s Deepmind, and Harmonic have models that achieve gold-medal level performance at the International Mathematical Olympiad, and are useful for mathematical research. Harmonic’s Aristotle engine specifically is built such that it uses the Lean proof assistant to produce formally verified proofs of its outputs. When applied to blockchains, similar capabilities could enable AI-assisted formal verification of smart contracts at scale, dramatically reducing the surface area for exploits.

The race between AI-powered attackers and AI-powered defenders is on, and the outcome will have significant implications for the security and trustworthiness of the entire crypto ecosystem. The long-term outlook appears bright, however, as smart contract code will become increasingly hard to break, and might eventually become impenetrable.

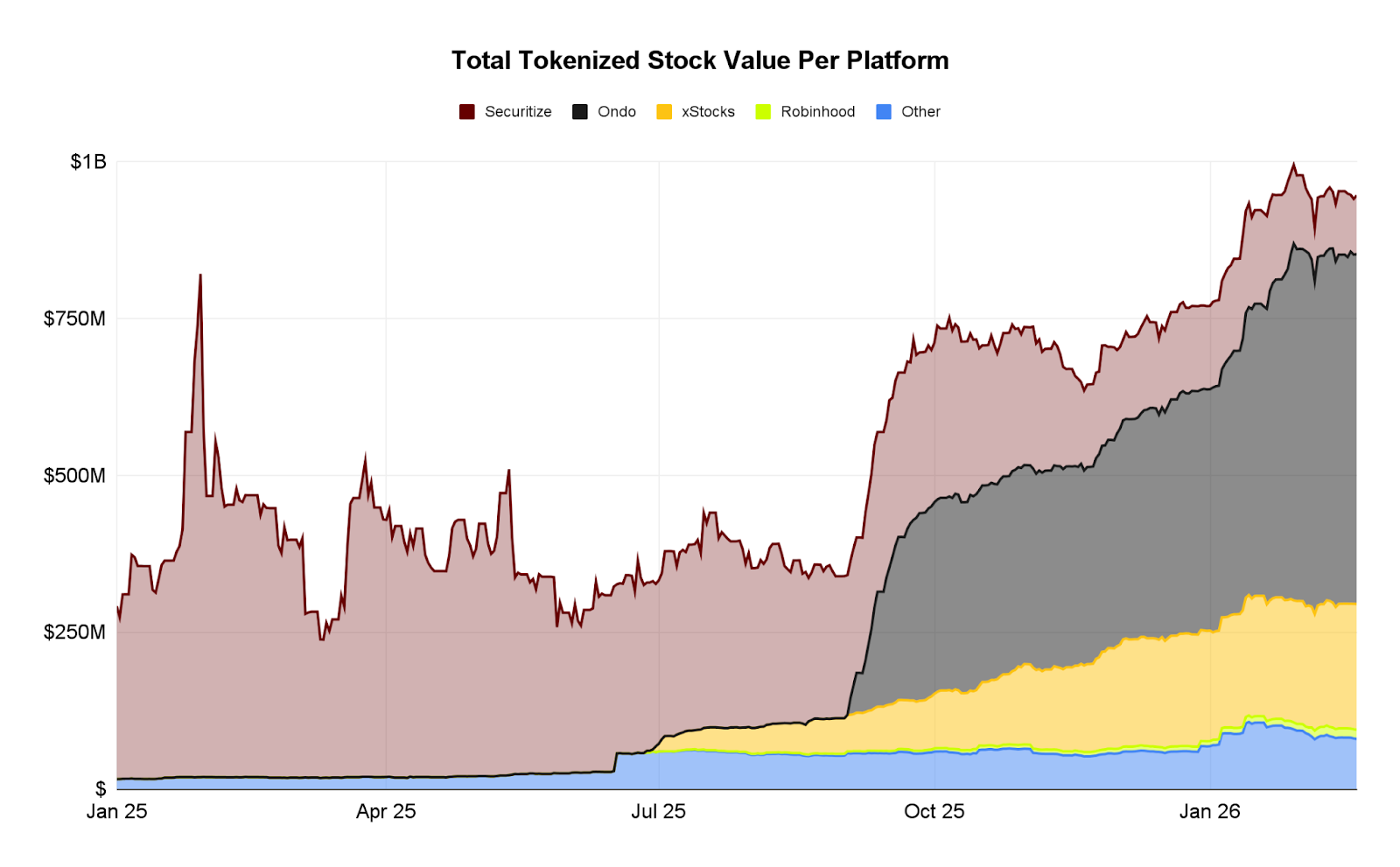

Figure, an onchain capital marketplace for loan origination, funding, and secondary trading, debuted a tokenized offering of its public stock that trades and settles natively onchain. As part of their $150M public secondary offering, Figure issued stock directly on its Onchain Public Equity Network (OPEN), bypassing traditional intermediaries entirely. This puts Figure among the first efforts to offer SEC-registered public equity that is issued and settles natively onchain, rather than synthetic price-tracking tokens or transfer-agent bridges of existing DTCC-format shares.

To date, tokenized stocks have largely existed as synthetic wrappers where a platform holds actual shares in a vault and issues tokens backed 1:1 to track their value. Because these tokens represent an indirect interest through a third party rather than the share itself, holders typically lack direct voting rights and must still rely on an array of traditional intermediaries, such as custodians and transfer agents, to bridge the gap between the blockchain and the legacy stock market. In contrast, Figure’s onchain FGRD shares are natively issued equity where the blockchain serves as the official SEC-registered master ledger of record, providing holders with direct ownership and full voting rights without the need for legacy intermediaries like the DTCC.

Figure is the first company to thoroughly eschew traditional intermediaries and offer stock natively onchain. Unlike third-party wrapped stocks, FGRD functions without legacy exchange rails or settlement cycles, and is the first to offer full equity and voting rights onchain. This means that FGRD is the first ever SEC-registered public stock to feature near-instant settlement, rather than the typical T+1 cycle of traditional finance. Additionally, because the OPEN network acts as the master record for FGRD shares, holders are now direct owners and won’t need to rely on the DTCC, a clearinghouse, or beneficial ownership through a broker. This allows FGRD to bypass several layers of cost, delay, and risk.

Despite its benefits, Figure’s approach does have some limitations, primarily with regards to composability. As natively issued equity, FGRD shares are currently restricted to the OPEN platform which runs on the Provenance blockchain, confining their DeFi integrations to the specialized ecosystem of whitelisted protocols running on the chain and limiting their access to liquidity. In contrast, other tokenized equities like xStocks function as permissionless wrappers (either ERC-20 or SPL tokens), enabling them to be traded freely across multiple ecosystems and integrate with existing protocols. While OPEN has some whitelisted integrations with public DeFi products like Exponent for yield trading using Figure’s YLDS stablecoin, DeFi functionality for tokenized stocks issued on OPEN is currently limited to Figure’s flagship lending and borrowing protocol, Democratized Prime. The platform will enable shareholders to use their FGRD as collateral for loans, lend their equity into hourly Dutch auction pools to earn market-driven yields, and earn short-selling locate fees that are normally exclusive to banks. While this already enables functionality improvements over holding equity in a traditional brokerage, it’s still limited compared to crypto assets that are fully composable within the broader DeFi ecosystem.

Figure understands the disadvantages of siloing its tokenized equity from the broader DeFi ecosystem and has announced plans for a second launch of its registered common stock directly on Solana. This expansion will eventually allow Figure's native shares to move beyond the OPEN network and integrate with the broader Solana DeFi landscape, enabling users to use their equity as collateral in protocols like Kamino and Raydium without the need for traditional intermediaries.

Source: RWA.xyz - Data as of February 20, 2026

Figure's goal is to offer native stock deployment on the OPEN network to any issuer, extending the service beyond its own equity. The company has already confirmed its first commitment from a third-party issuer following the onchain deployment of FGRD. This places Figure at the forefront of a shifting RWA landscape where both legacy and crypto-native players are racing to bring the $126T in global equities onchain. While the majority of tokenized equities today are created by crypto-native protocols like Ondo, Kraken, and Securitize, legacy brokerages have already begun to transition their core businesses onchain. Notably, Robinhood has brought $15M of equities onchain since they launched tokenized stock and ETF trading for EU users in July 2025, and their proprietary Ethereum layer 2 purpose-built for RWA trading saw 4 million transactions in its first week of public testnet. Today, Robinhood’s $15M in tokenized equities represents less than 0.005% of its $324 billion in Total Platform Assets. Simultaneously, ICE (the parent company of the NYSE) has announced plans to launch their own 24/7 tokenized securities platform with whitelisted trading. Unlike Robinhood, which currently settles trades on Arbitrum, exchanges made through ICE’s new platform will settle on a purpose-built permissioned blockchain. Figure is uniquely positioned in this field, as their approach to tokenizing equities retains the advantages of both institutional and crypto-native solutions. Shares issued on the OPEN network preserve the full ownership and voting of traditional equities, yet remain composable within whitelisted DeFi.

Source: CoinGecko, GSR - Data as of Feb 22, 2026

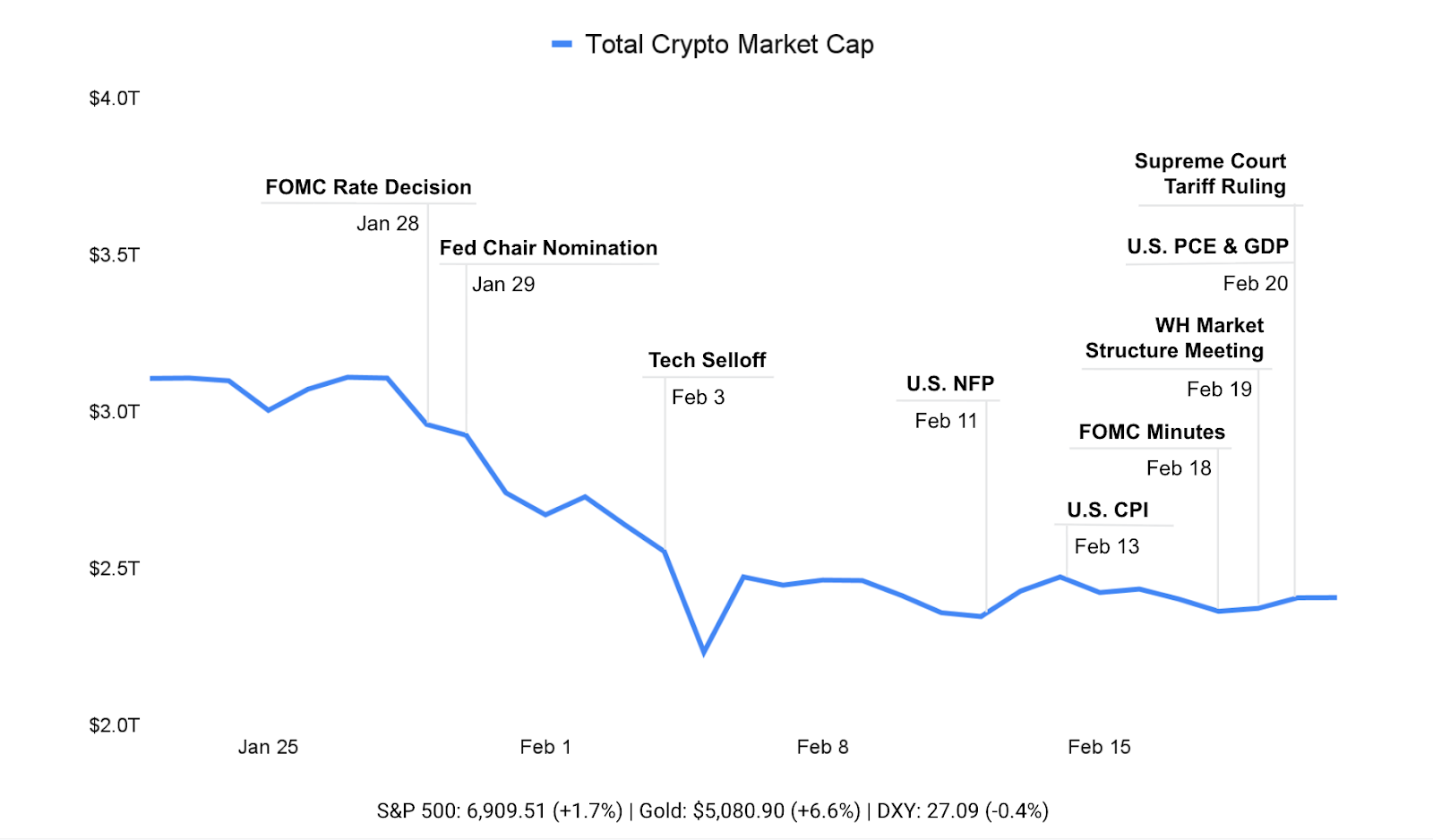

Crypto markets were largely range-bound this week, with total market cap chopping around the mid-$2T area and finishing only modestly changed. Other markets looked more constructive: U.S. equities ground higher, while gold extended its run and the dollar softened.

The macro focus stayed firmly on the Fed. FOMC minutes reinforced a ‘higher-for-longer’ bias, with policymakers warning that progress back to 2% inflation could be ‘slower and more uneven’ and explicitly flagging tariff-related cost pressures as a potential upside risk to prices. That framing kept risk appetite contained.

Friday’s data releases did little to ease those concerns. The BEA’s advance read on Q4 2025 GDP showed growth slowing to 1.4%, while inflation data remained sticky with headline PCE rising 2.9% YoY. Overall, the market got slower growth without relief on the inflation front, reinforcing the Fed’s caution and tempering risk appetite.

Geopolitical concerns further limited risk appetite throughout the week amid a massive buildup of U.S. military forces in the Middle East as the Trump administration considers whether or not to strike Iran. Uncertainty on whether the US will choose diplomacy or military action continues to cause market jitters.

Trade policy also re-entered the picture. The Supreme Court struck down major parts of Trump’s tariff regime with a 6–3 decision finding the emergency-powers law used did not authorize the tariffs, raising questions around refunds and the path forward for U.S. trade policy. Risk assets initially took the news positively, but the bigger impact was the renewed policy uncertainty, with officials signaling alternative legal routes to re-impose broad tariffs, keeping the inflation outlook murky.

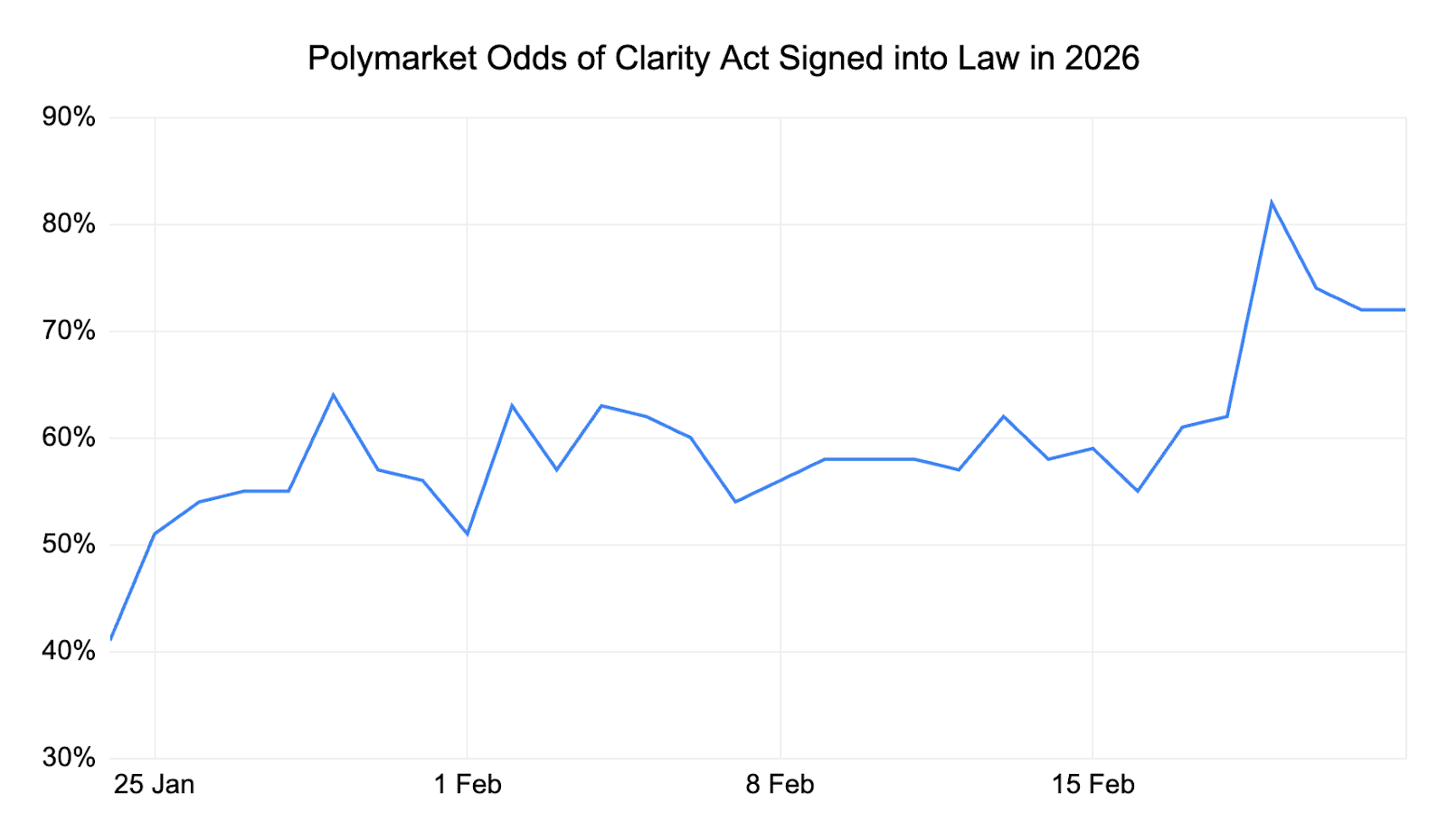

Source: Polymarket

Finally, U.S. regulatory headlines provided some optimism. White House market structure talks on Thursday between major banks and crypto industry participants were characterized as constructive, even if no deal was finalized. The improvement in tone was reflected in prediction markets, with Polymarket’s odds for the Clarity Act being signed this year jumping from around 60% earlier in the week to over 80% on Thursday, before settling around 70%.

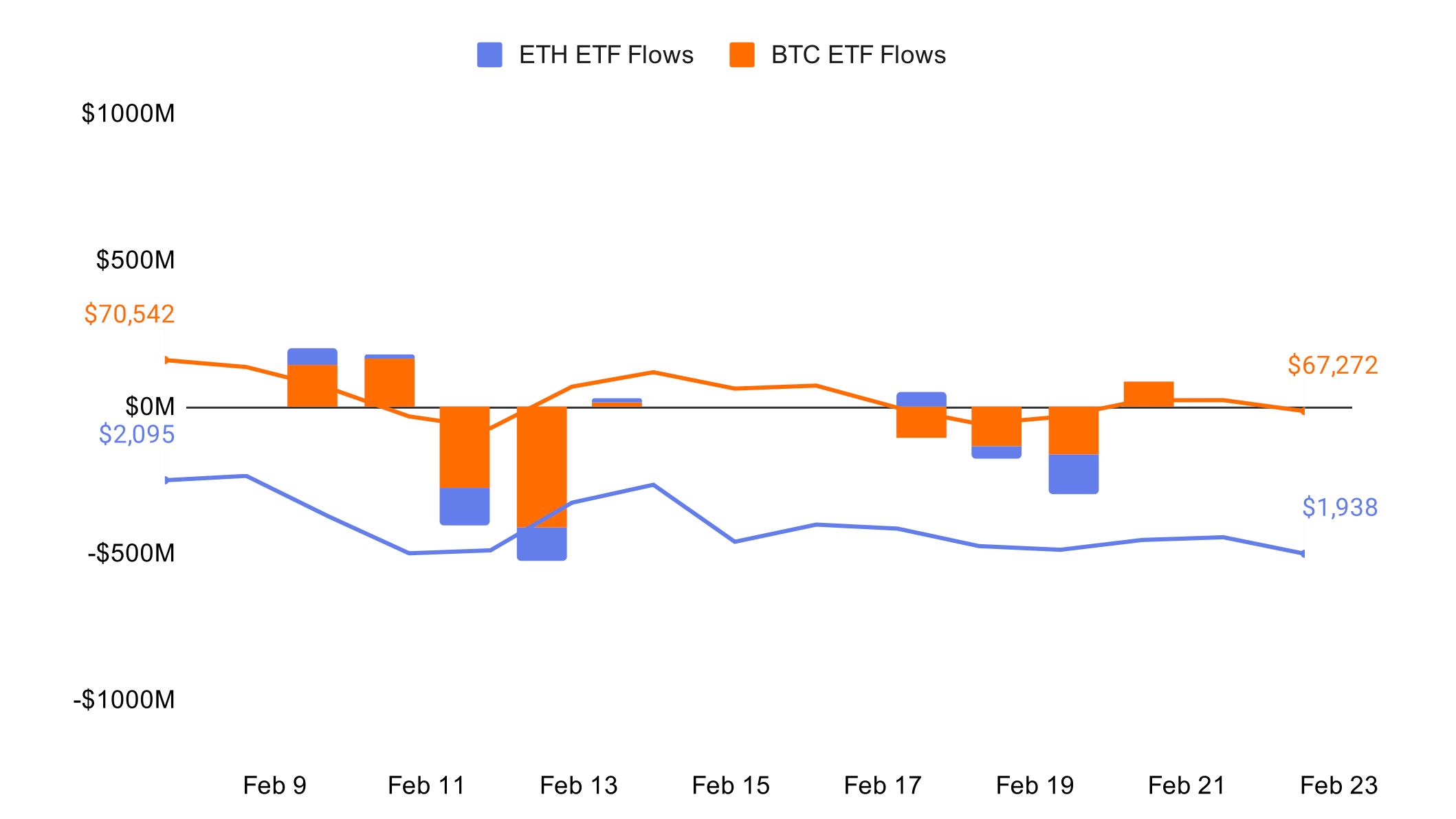

Source: Farside Investors, CoinGecko - Data as of Feb 22, 2026

Net ETF flows, while still mostly negative, have stabilized in comparison to the wild swings of the prior month. U.S. spot Bitcoin ETFs posted three sessions of net outflows (-$105M on Feb 17, -$133M on Feb 18, and -$166M on Feb 19), but saw a modest reversal on Friday (+$88M on Feb 20), closing the week down roughly $316M. Ether ETF flows swung from an early-week inflow (+$49M on Feb 17) to heavy mid-week redemptions (-$42M and -$130M), for a net -$123M. The major pairs have traded relatively flat over the past 2 weeks. BTC drifted from $69.3k to $67.2k (-3%), failing to hold a brief push back toward $69k. ETH lagged behind, sliding from $2,091 to $1,938 (-7%) and continues to fail in sustainably reclaiming the $2,000 level.

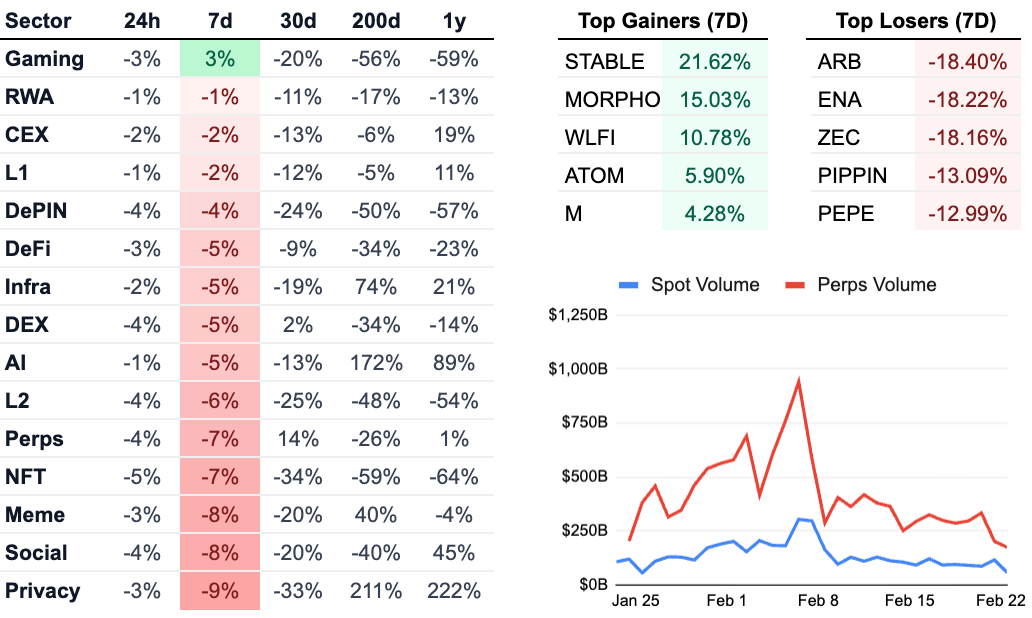

Source: CoinGecko, GSR - Data as of Feb 22, 2026

While most sectors traded flat, matching the performance of major pairs, a few categories posted losses for the week. The privacy sector was the worst performer due to drawdowns in Zcash (-17.8%) and Monero (-3.5%). While privacy remains a key narrative, the sector has continued to bleed ever since Zcash’s parabolic rise last September. Perpetuals, which have been the standout performer over the last 30 days, cooled off this week with a 7% decline. Their ability to generate consistent revenue despite broader conditions has allowed them to consistently outperform other sectors during the bear market.

Despite the generally lackluster week for the broader market, several individual tokens managed to post significant gains. STABLE (+22%) led the pack, not due to any singular catalyst but through a combination of hype generated from updates around development progress and potential integrations with institutional rails. MORPHO (+15%) also saw sustained demand following news of its partnership with Global Asset Manager Apollo the prior week. Given more favorable market conditions, the announcement of an integration between a major asset manager and a DeFi protocol would be reflected on charts in a matter of minutes instead of days, but the market has generally been delayed in its reaction to positive news.

This material is provided by GSR (the “Firm”) solely for informational purposes. It is not intended to be advice or a recommendation to buy, sell or hold any investment mentioned. Investors should form their own views in relation to any proposed investment.

It is intended only for sophisticated, institutional investors and does not constitute an offer or commitment, a solicitation of an offer or commitment, or any advice or recommendation, to enter into or conclude any transaction (whether on the terms shown or otherwise), or to provide investment services in any state or country where such an offer or solicitation or provision would be illegal. The Firm is not and does not act as an advisor or fiduciary in providing this material.

This material is not an independent research report, and has not been prepared in accordance with any legal requirements by any regulator (including the FCA, FINRA or CFTC) designed to promote the independence of investment research.

This material is not independent of the Firm’s proprietary interests, which may conflict with the interests of any counterparty of the Firm. The Firm may trade investments discussed in this material for its own account, may trade contrary to the views expressed in this material, and may have positions in other related instruments. The Firm is not subject to any prohibition on dealing ahead of the dissemination of this material.

Information contained herein is based on sources considered to be reliable, but is not guaranteed to be accurate or complete. Any opinions or estimates expressed herein reflect a judgment made by the author(s) as of the date of publication, and are subject to change without notice. The Firm does not plan to update this information.

Trading and investing in digital assets involves significant risks including price volatility and illiquidity and may not be suitable for all investors. The Firm is not liable whatsoever for any direct or consequential loss arising from the use of this material. Copyright of this material belongs to GSR. Neither this material nor any copy thereof may be taken, reproduced or redistributed, directly or indirectly, without prior written permission of GSR.

Please see here for additional Regulatory Legal Notices relevant to US, UK and Singapore.