GSR Weekly Update - February 9th, 2026

BTC: $71,198 (-8.6%) | ETH: $2,113 (-10.0%) | BTC Dom: 57.1% | Global Cap: $2.49T

Ethereum founder Vitalik Buterin shocked crypto users last Wednesday when he published a post on X stating that “the original vision of L2s and their role in Ethereum no longer makes sense.” While X users were quick to react to the headline, the post didn’t represent the wholesale rejection of rollups that many took it to be. Instead, Vitalik’s aim was to realign the Ethereum community’s vision for the chain’s scaling in a direction that recognizes the challenges the old roadmap has run into, and takes into account the technological progress that has occurred since the rollup-centric direction was set in 2020.

The original rollup-centric roadmap envisioned rollups as extensions of Ethereum that would provide the exact same security guarantees as the base layer while scaling transaction throughput. Almost six years later, however, practically zero rollups have reached the ‘Stage 2’ level that would qualify them as fully inheriting the base layer’s guarantees. Indeed, very few rollup teams intend to reach this milestone in the short term, as it would mean giving up on their ability to upgrade their systems to fix software bugs, or for customization purposes. The original vision of homogenous security guarantees across layer 1 and layer 2s thus remains far from becoming a reality.

Security guarantees aren’t the only reason Vitalik believes the rollup-centric roadmap no longer makes sense, he also believes that layer 2s are not needed for scaling anymore. This is mainly because the base layer itself is scaling, with the chain’s gas limit set to more than triple after this year’s Glamsterdam fork. By integrating zkEVM tech directly into the base layer, the roadmap calls for an eventual increase in throughput from a current 40 TPS to a target level of 10,000 TPS. Because he believes that rollups are no longer needed to scale, Vitalik suggested that layer 2s specialize and “identify a value other than ‘scaling’” by offering differentiated features such as optimizing around a specific application, overlaying privacy, or implementing a complete redesign for applications that are not financial in nature like social and identity layers, among other things.

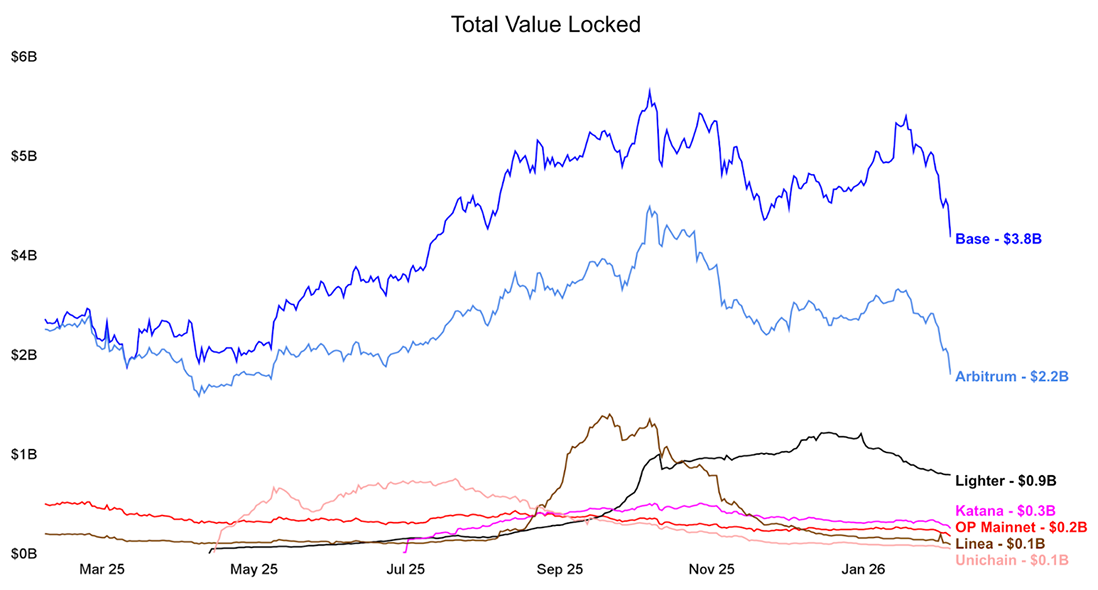

Source: DeFiLlama - Data as of Feb 8, 2026

Vitalik’s comments come at a time when generalized scaling solutions like Arbitrum and Base dominate specialized layer 2s in fundamental metrics like total value locked. The reality is that, today, generalized layer 2s are scaling Ethereum and are likely to be where a large fraction of users continue to transact into the near future.

We thus can’t help but wonder whether Vitalik’s comments are perhaps somewhat premature. While the layer 1 is set to scale significantly in the next year, even tripling its throughput will put it far behind the scaling capabilities of generalized layer 2s like Optimism, Arbitrum, and Base. The upgrade to using zkEVMs at the base layer will be complex, and is likely to happen in the order of years. On top of that, the layer 1 is not currently competitive in terms of transaction confirmation latency, and solutions around pre-confirmations or reducing slot times seem unlikely to be implemented anytime soon. Generalized layer 2s will continue to provide a better, snappier user experience for the foreseeable future. Lastly, focusing only on tech ignores many of the other vectors of differentiation that otherwise “copypasta EVM chains” can pursue, for instance via culture and branding. Base, as an example, has been successful by focusing on consumer use cases, while Arbitrum has found market fit with its focus on DeFi, despite both chains largely supporting the same EVM development environment at the technical level. Ultimately, while Vitalik’s vision of vanilla EVM activity mainly occurring on the base layer may eventually become a reality, Stage 1 layer 2s and sidechains will continue to play a significant role in the short term by scaling and bringing users into the ecosystem.

AI agents have burst back into the scene with a flurry of new developments. ‘Moltbook’, a new Reddit-style social network for AI agents, was the center of attention last week as the tech industry grappled with the significance of major advancements in agent autonomy. Coinciding with the Moltbook buzz, the Ethereum Foundation’s dAI team began the rollout of its ERC-8004 Trustless Agents standard, pointing to a potentially compelling area of convergence for crypto and AI.

Moltbook captured the tech industry’s imagination by displaying how human-like and independent AI agents can now seem. It consists of an online forum that is in principle only accessible to AI agents, but which humans can observe. It generated much fascination as agents interacted and had deep conversations with one another, without a human in the loop. It also raised concerns with at least one agent posting a manifesto calling for the end of the ‘age of humans’, while others attempted to create their own language that would allow them to communicate without human supervision. While both astounding and worrying at first glance, many, if not most, of these Moltbook interactions are puppeteered by humans in the background to maximize engagement, and so should be viewed with some skepticism. The overall experiment, however, does point to real and important trends in rising agent autonomy.

Moltbook is linked to the rise in popularity of agent frameworks like OpenClaw (formerly known as Clawdbot, and later Moltbot). OpenClaw is an open source framework that allows users to run an AI assistant using their own hardware. It orchestrates interactions between LLMs like Claude or ChatGPT and the user’s own hardware, allowing the AI to read local files, run terminal commands, and use applications on the system like a web browser or messaging apps. Because it has direct system access, it can perform multi-step workflows. Its ‘heartbeat’ feature enables the agent to work proactively, instead of waiting for the user to prompt it: the agent will automatically wake itself up and follow previous instructions, allowing it to execute complex, long-horizon tasks similar to how a human would.

Frameworks like OpenClaw are enabling a shift in the prevailing model of human-to-AI interactions. While most AI use to date has occurred synchronously via chat interfaces, improvements in AI autonomy are increasingly making asynchronous workflows possible, such that users can specify a task and agents can go off and try to execute it independently over the span of hours, occasionally checking-in with the user for feedback and guidance. This change is being driven not only by ‘harness’ frameworks like OpenClaw, but by improvements in the capabilities of the underlying models to perform long-horizon tasks. AI models from the likes of OpenAI and Anthropic have improved in this regard at an exponential rate. Interacting with AI is thus becoming more like collaborating with a human coworker than engaging in one-off prompt-and-response sessions.

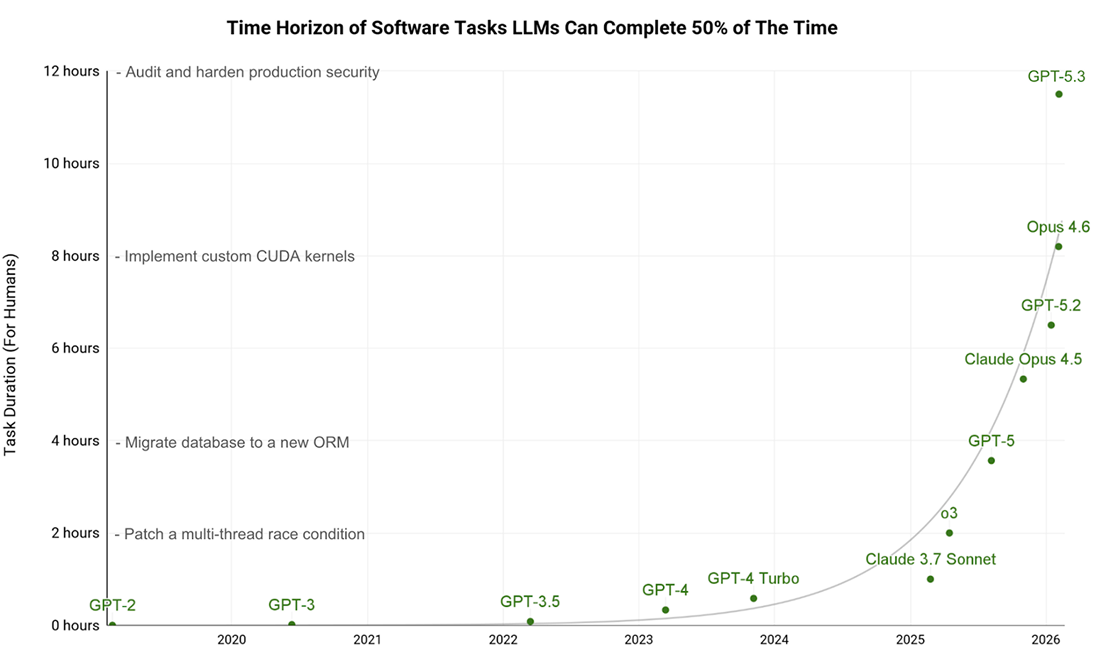

Source: METR

How does any of this relate to crypto and blockchains, anyway? In two key ways: trust and digitally-native value exchange. As AI agents become more autonomous, it’ll increasingly become harder to supervise their actions, and we’ll inevitably rely on them to independently perform more complex and consequential tasks. The degree of trust placed on AI agents will only grow, giving rise to a problem: how can AI agents provide us with sufficient trust guarantees?

Blockchains provide a natural array of solutions, it turns out, which the Ethereum Foundation is hoping to promote with its ERC-8004 Trustless Agents standard. The standard acts almost like a ‘Yelp’ for AI agents, providing a credibly neutral registry of agents that records the services they provide and their reputation. It thus helps users discover agents providing services they’re interested in, and decide which agents to trust based on the reputation they’ve developed across past interactions with other users. The standard further includes a forthcoming ‘Validation Registry’, which leverages the trustless execution guarantees of crypto systems via TEEs, validator staking, or zkML to ensure AI agents operate honestly.

On top of providing this trust layer for AI agents, blockchains also provide a natural means for them to exchange value. The low cost, programmable, and instant payments that high-performance blockchains enable are a perfect fit for AI agents to receive payment for their services, transact with other agents, and pay for the API based tools and resources they need to accomplish their tasks. In this vein, open source protocols like Google’s A2A protocol and Coinbase’s x402 payments protocol enable agents to communicate, collaborate, negotiate, and pay each other through crypto-native means.

We’re in the midst of an exciting convergence between AI and crypto. Rising capabilities in AI autonomy are naturally complemented by the trust and value exchange infrastructure that blockchains have developed. While the AI agent cycle in late 2024 resulted in little more than chatbots attached to memecoins, the current wave of convergence between crypto and artificial intelligence promises to be substantial and durable.

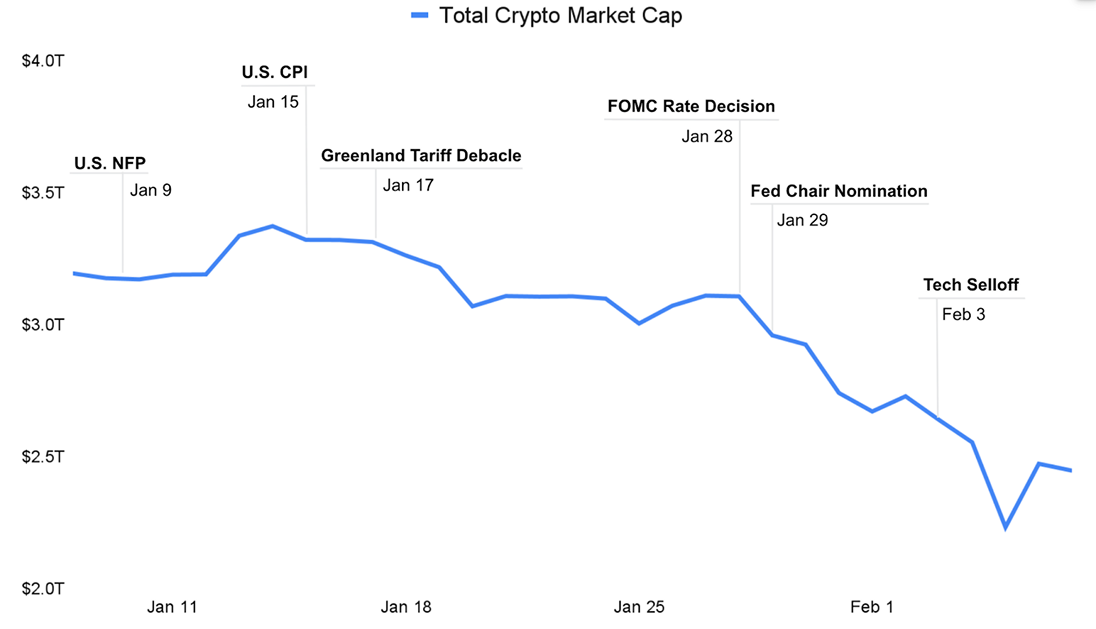

Source: CoinGecko - Data as of Feb 8, 2026

It’s been a turbulent month for crypto as early-year optimism quickly transitioned into an aggressive deleveraging phase that saw the total crypto market cap plunge to $2.2T, the lowest level since September 2024. While the year began with some upward momentum amid new year optimism and a reprieve from tax-related selling, a series of compounding macro and geopolitical shocks have led to overwhelming risk-off sentiment.

The recent nomination of Kevin Warsh as Federal Reserve Chair introduced a new layer of uncertainty that significantly dampened the market’s appetite for risk assets. Known for his historically hawkish stance on inflation and criticisms of the Fed’s balance sheet expansion, Warsh’s selection led to a reassessment of the market’s expectations around monetary policy. Market participants had previously expected Trump to go with a more dovish pick that would hew closely to his preferences. Picking Warsh was a surprise that was taken as a positive for Fed independence and the dollar, but led to a preemptive derisking phase that contributed to the breach of key support levels across crypto, precious metal, and equity markets.

Already fragile market conditions were further tested by a sudden spike in geopolitical tensions last week after U.S. forces intercepted and destroyed an Iranian Shahed-139 drone in the Arabian Sea. President Trump had previously commented on the high stakes of upcoming nuclear negotiations with Iran, warning that “bad things” would happen if a deal could not be reached. The event thus triggered a flight to safety out of risk assets like crypto and equities towards commodities like gold and silver. While the market has since staged a tentative recovery, investors remain cautious amid ongoing global friction.

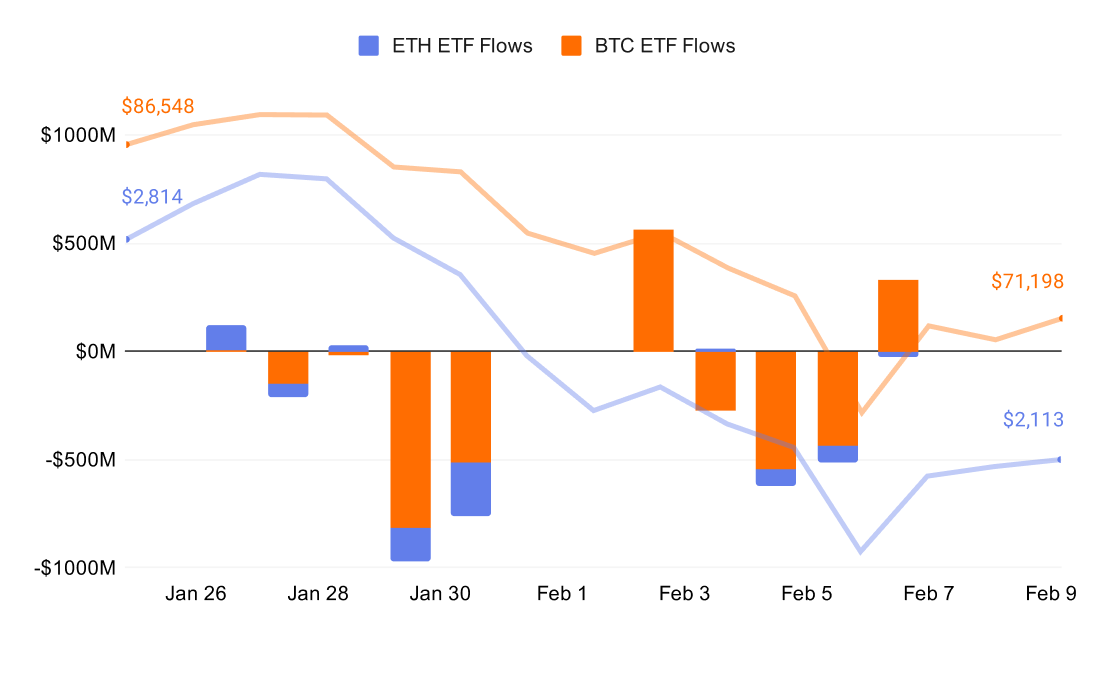

Source: CoinGecko, Farside Investors - Data as of Feb 8, 2026

Looking at ETF flows, the massive capitulation event on the 29th led to combined net outflows of nearly $1B, with BTC experiencing its worst single-day net outflow since November 2025. This liquidity vacuum forced an immediate repricing, driving Bitcoin from the $89,000 range down toward $75,000 in a near-vertical descent. While Bitcoin saw significant outflows, the selling pressure on Ethereum relative to its market cap was even more severe, resulting in continued underperformance relative to Bitcoin throughout the drop.

There was a singular day of respite on February 2nd, with over $500 million in positive inflows as Bitcoin buyers attempted to front-run a potential bottom. However, the recovery proved short-lived. Prices failed to reclaim key structural levels, and the immediate return to net outflows on February 4 and 5 precluded a reversal.

Toward the end of the week, crypto markets were dragged down by a selloff in tech equities. A key driver of the selloff was a repricing in software and SaaS equities driven by fear that generative AI will make traditional subscription models obsolete. The S&P 500 Software & Services Index plummeted 7% over the week, extending its year-to-date losses to over 15%. Worries about AI-related equity valuations also played a role, driven by concerns that valuations are outpacing near-term returns amid massive capital expenditures. Alphabet, for example, revealed it’s projecting up to $185 billion of AI spending in 2026. Weighed by these concerns, hyperscalers like Microsoft, Alphabet, and Amazon shed 5%, 6%, and 13% throughout the week, respectively. Because of the high correlation between speculative tech and digital assets, Bitcoin plunged to roughly $62,000, its lowest level since 2024.

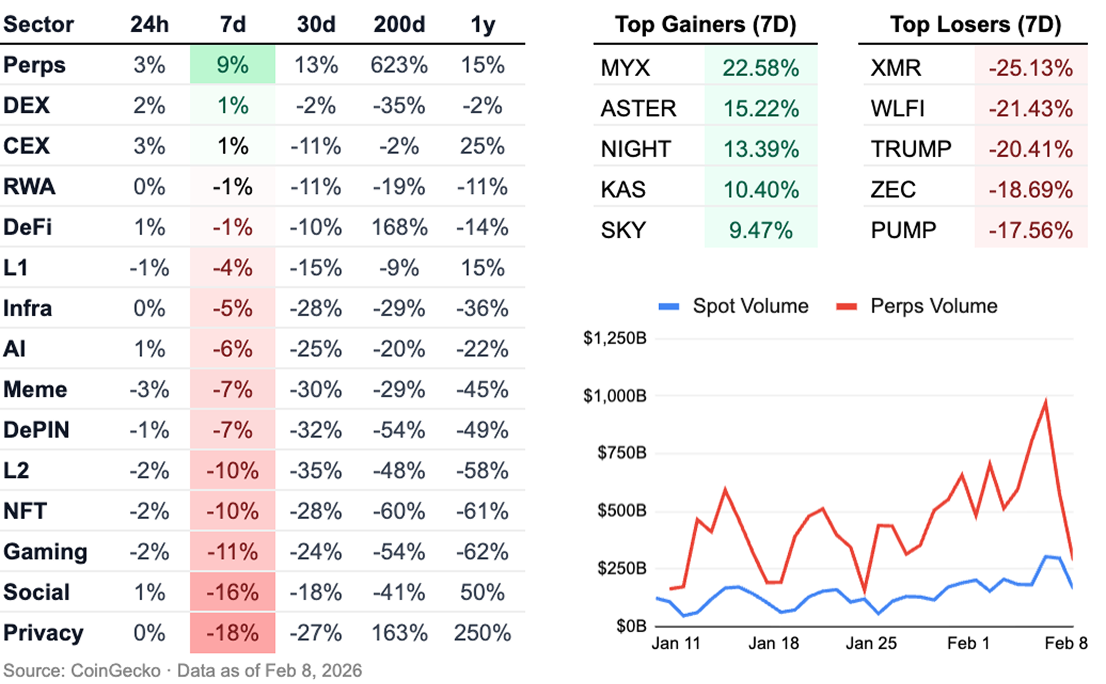

Despite the sharp drop in most sectors last week, the perpetual sector is up 9%, driven by rallies in Aster (15%) and Hyperliquid (10%). Hyperliquid’s bullish momentum in an otherwise bearish market was fueled by the protocol’s continually increasing HIP-3 volumes and the recent announcement of HIP-4. The proposed network upgrade would allow Hyperliquid to natively support prediction markets and options trading, increasing its core product offerings and enabling it to compete with centralized exchanges as these increasingly add prediction market capabilities.

The privacy sector took the largest hit this week, as industry leaders Monero (-25%) and Zcash (-19%) were some of the worst performing assets in the top 100 by market cap. Although the sector has struggled recently, privacy remains the clear winner over the last twelve months, up 250% while most are down double-digits.

On February 6th, there was nearly $1T in total volume across perpetual markets as markets lit up with activity amid the heightened volatility.

This material is provided by GSR (the “Firm”) solely for informational purposes. It is not intended to be advice or a recommendation to buy, sell or hold any investment mentioned. Investors should form their own views in relation to any proposed investment.

It is intended only for sophisticated, institutional investors and does not constitute an offer or commitment, a solicitation of an offer or commitment, or any advice or recommendation, to enter into or conclude any transaction (whether on the terms shown or otherwise), or to provide investment services in any state or country where such an offer or solicitation or provision would be illegal. The Firm is not and does not act as an advisor or fiduciary in providing this material.

This material is not an independent research report, and has not been prepared in accordance with any legal requirements by any regulator (including the FCA, FINRA or CFTC) designed to promote the independence of investment research.

This material is not independent of the Firm’s proprietary interests, which may conflict with the interests of any counterparty of the Firm. The Firm may trade investments discussed in this material for its own account, may trade contrary to the views expressed in this material, and may have positions in other related instruments. The Firm is not subject to any prohibition on dealing ahead of the dissemination of this material.

Information contained herein is based on sources considered to be reliable, but is not guaranteed to be accurate or complete. Any opinions or estimates expressed herein reflect a judgment made by the author(s) as of the date of publication, and are subject to change without notice. The Firm does not plan to update this information.

Trading and investing in digital assets involves significant risks including price volatility and illiquidity and may not be suitable for all investors. The Firm is not liable whatsoever for any direct or consequential loss arising from the use of this material. Copyright of this material belongs to GSR. Neither this material nor any copy thereof may be taken, reproduced or redistributed, directly or indirectly, without prior written permission of GSR.

Please see here for additional Regulatory Legal Notices relevant to US, UK and Singapore.