GSR Weekly Update - March 23rd, 2026

BTC: $68,707 (-4.1%) | ETH: $2,080 (-0.7%) | BTC Dom: 56.3% | Global Cap: $2.44T

Carlos Guzman

Research Analyst

Slater Santer

Research Analyst

BTC: $68,707 (-4.1%) | ETH: $2,080 (-0.7%) | BTC Dom: 56.3% | Global Cap: $2.44T

Carlos Guzman

Research Analyst

Slater Santer

Research Analyst

Frank Chaparro, GSR Head of Content and Special Projects

Trump has declared himself the “crypto president,” but in many ways he’s also the “perps president.” As is well documented, Trump doesn’t sleep and he has no hesitation making market-moving statements outside traditional trading hours. It’s a strange but fitting backdrop: markets are evolving toward round-the-clock trading just as we have a president best described as spontaneous, and at times, chaotic.

That dynamic was on full display this weekend. Just days after S&P Global announced it would license the S&P 500 for trading on Hyperliquid, Trump said Friday afternoon, after markets had closed, that the U.S. was “getting very close to meeting our objectives.” The S&P 500 proxy on Hyperliquid rallied in response.Then on Saturday at 7:44pm ET, Trump escalated rhetoric, threatening to strike Iran’s power plants if the Strait of Hormuz wasn’t reopened. The reaction on Hyperliquid was clear: the S&P 500 sold off.

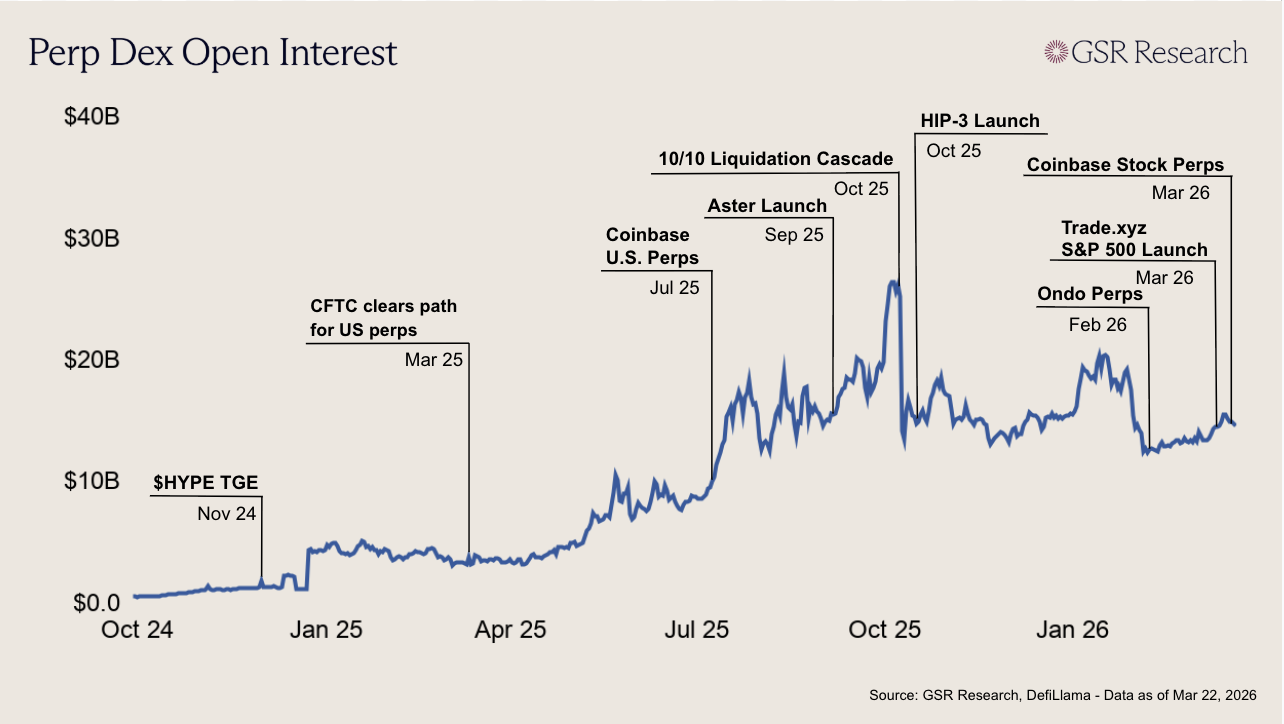

The nature of the Trump presidency may not be ushering in 24/7 markets, but it certainly makes them more interesting. To be clear, it’s not yet apparent which specific perpetual product will emerge as dominant, or whether this will ultimately become the preferred 24/7 market structure. That remains to be seen. Futures have historically been a less familiar product for U.S. retail investors compared to options. And I have my reservations about the extent to which traditional brokers will gatecrash perpetuals with their own offerings. For one because I don’t know if their existing client base will love the product as much as the crypto world has embraced them. Still, open interest across perp DEX platforms has surged. In January 2026, perp DEX volume reached $739.48 billion, while decentralized venues captured 10.2% of total crypto perpetuals trading, up sharply from 2.0% two years earlier.

This morning, Katana announced the acquisition of IDEX alongside the launch of Katana Perps, a new perpetual futures platform designed to integrate spot and derivatives trading within a single onchain environment. The move marks the first major initiative under new CEO Matthew Fisher and signals a clear strategic shift: owning more of the trading infrastructure and capturing a greater share of associated revenues.

IDEX brings nearly a decade of live exchange infrastructure, including a high-performance matching engine paired with onchain settlement. That foundation is expected to support higher throughput execution and deeper liquidity as Katana scales its perpetuals offering.

The timing is notable. Regulatory signals in the U.S. are beginning to point toward a potential path for crypto perpetual futures, while trading activity continues to migrate toward always-on venues. In parallel, decentralized perpetuals have seen rapid growth. In January 2026, perp DEX volume reached $739 billion, with decentralized venues accounting for 10.2% of total crypto perpetuals trading, up from just 2.0% two years earlier.

Against that backdrop, Katana’s move reflects a broader shift toward vertical integration in onchain trading. Rather than relying on fragmented infrastructure, platforms are increasingly looking to control execution, liquidity, and product layers in-house. The launch of Katana Perps, alongside the IDEX acquisition, positions the protocol to compete more directly in a market where scale, liquidity, and user experience are becoming key differentiators.

More broadly, as perpetual futures gain share from centralized exchanges and traditional market structures evolve toward continuous trading, the competitive landscape is likely to consolidate around platforms that can offer integrated, high-performance infrastructure. Katana’s latest move is an early step in that direction.

On Tuesday, payments blockchain Tempo launched its mainnet. Incubated by Stripe and Paradigm, Tempo is a layer 1 purpose-built for stablecoin payments, targeting use cases like cross-border remittances, global payouts, embedded finance, and increasingly, agentic payments. Alongside mainnet, the team also introduced the Machine Payments Protocol (MPP), an open standard for machine-to-machine payments co-authored with Stripe. MPP rivals Coinbase's x402 protocol as one of a growing number of frameworks vying to become the standard way for AI agents to pay for services on the internet. Both protocols represent an attempt to fill a gap that has existed since the web's inception: a native way for software to pay for other software. If they succeed, they could meaningfully expand what AI agents are capable of.

Today's AI agents can write code, coordinate services, retrieve data, and execute complex multi-step workflows. However, they hit a wall whenever they need to pay for something. Traditional payment flows require accounts, subscriptions, API keys, and manual approval, all designed for humans. This forces agents to rely on credentials their human operators have provisioned, restricting them to a narrow, pre-configured set of tools. An agent tasked with a research project can't independently access a dataset it discovers along the way, purchase additional compute, or pay for a specialized model inference. It either works within the confines of what's already been set up, or it stops and asks for help.

Agentic payment protocols aim to remove this bottleneck. The core promise is simple: if an agent can pay for any compatible service on demand, without prior setup, the range of tools and capabilities available to it expands dramatically. Instead of operating within a walled garden of pre-approved services, agents become capable of dynamically discovering, accessing, and composing tools as needed.

Both MPP and x402 work by reviving the long-dormant HTTP 402 'Payment Required' status code. The basic flow is similar across both: an agent requests a resource, the server responds with a 402 containing payment instructions, the agent authorizes payment, and the server delivers the resource. No accounts, no API keys, no subscriptions. The payment itself is the credential.

Where they diverge is in their approach to throughput and settlement. x402 currently requires a discrete onchain transaction per payment, which works well for one-off requests but becomes less practical for the high-frequency, low-value interactions that agent workflows generate at scale. MPP addresses this with a primitive called 'sessions', which function as payment channels on the EVM. An agent deposits funds into an onchain escrow, then signs cumulative cryptographic vouchers as it consumes resources, which the server can verify in microseconds without touching the chain. Using this approach, thousands of micro-interactions can be batched into a single settlement transaction, making per-API-call pricing viable at internet scale.

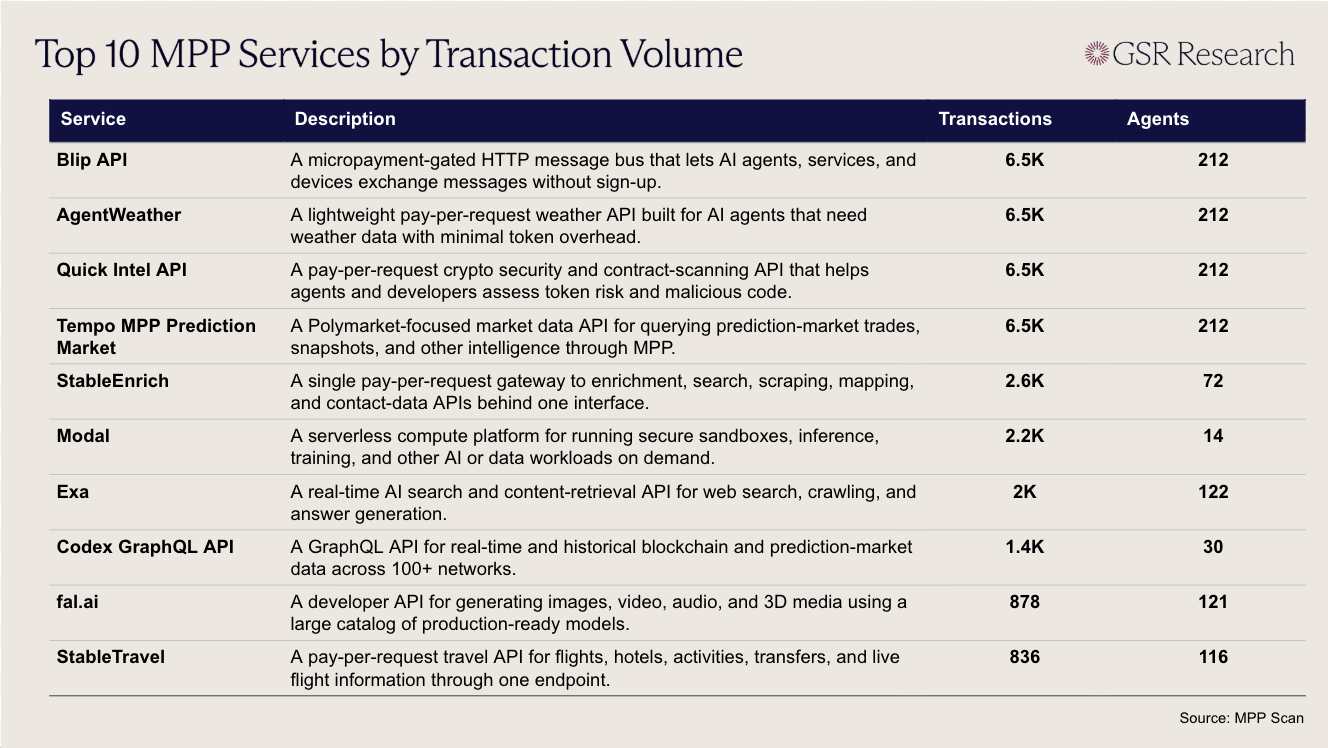

Both protocols already have live service directories. MPP launched with integrations across more than 100 services spanning model providers, compute platforms, developer infrastructure, and data services, with the likes of Visa, Mastercard, and Lightspark extending it to support card and Lightning payments. Meanwhile, x402 has processed over 50 million transactions, and recently added support for any ERC-20 token.

Additionally, these protocols enable use cases that go well beyond simple API access. One could imagine, for instance, a medical research agent that pays for access to proprietary datasets, clinical trial results, and patent filings, cross-referencing them across multiple paid sources before delivering a synthesis. Or a software development agent that autonomously provisions cloud compute, deploys a staging environment for a mobile app, runs tests against it, and shuts it down when it's done. Or a video editing agent that purchases stock footage, music licenses, and rendering credits, assembling a finished product from components that each have their own pricing and rights management. None of these transactions involve a human clicking 'buy', none of them map to a traditional checkout, and none of them work with monthly subscriptions, since the agent might use a service once for three seconds and never return. These are still largely theoretical, but the recent MPP hackathon, where 41 projects were built in under a week, suggests developers are already trying to make such workflows a reality.

Stablecoins and crypto rails are a particularly natural fit for this kind of commerce. Traditional payment systems carry per-transaction fees in the tens of cents, making sub-cent micropayments economically impossible. Stablecoins on modern blockchains reduce fixed transaction costs to fractions of a penny, which is what makes pay-per-API-call pricing viable in the first place. Beyond cost, crypto rails offer properties that are hard to replicate in traditional finance: instant settlement without intermediaries, programmable escrow and spending policies that let a human define precise budget constraints an agent must operate within, and 24/7 availability without banking hours or batch processing windows. As we noted in our February 9th edition, crypto can complement AI in two key ways: that is, by providing infrastructure for trust and digitally-native value exchange. Agentic payment protocols promise to make the latter a reality. Both MPP and x402 remain early, with actual commercial volumes still modest, but the infrastructure race to build the payment layer for the agentic internet is well underway.

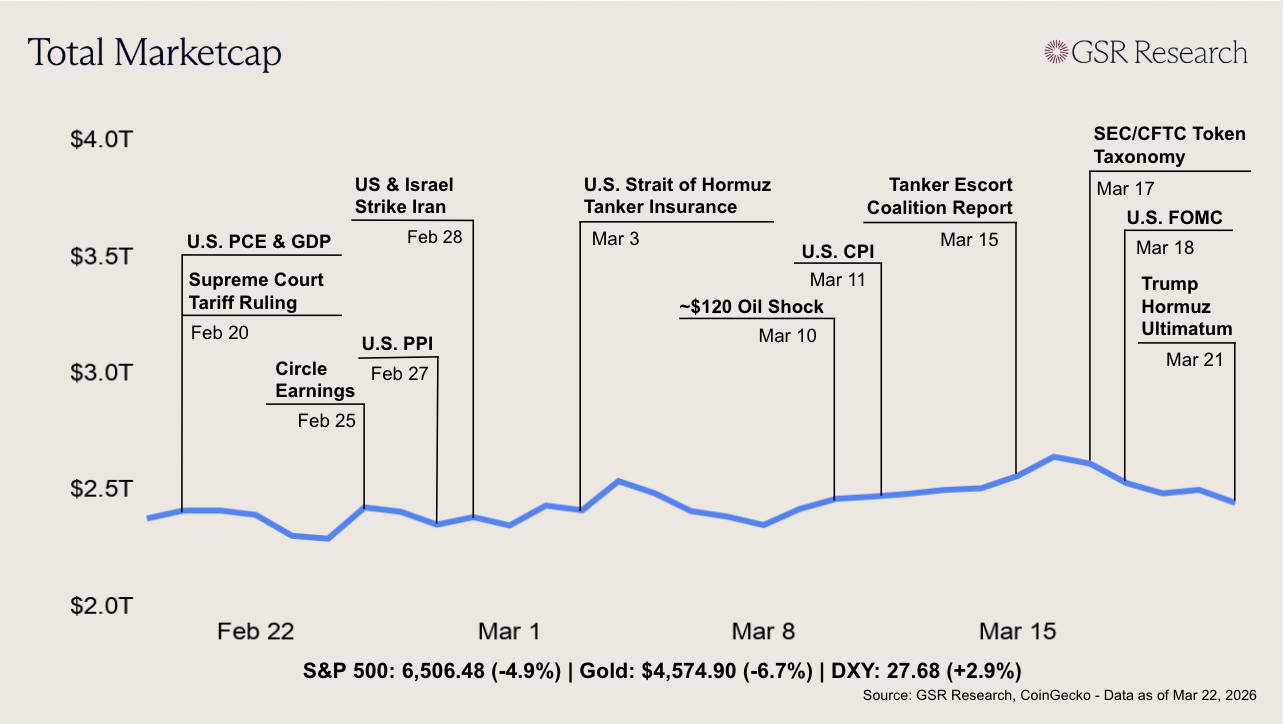

Crypto markets gave back the prior week's gains as a hawkish FOMC decision and escalating geopolitical tensions overwhelmed substantial U.S. regulatory progress. The total crypto market cap opened near $2.51T and peaked on Tuesday as BTC briefly touched $75,800, driven by a wave of derivatives-led short covering. On the same day, the SEC and CFTC published their landmark joint interpretation classifying 16 major crypto assets (including BTC, ETH, SOL, and XRP) as digital commodities rather than securities. However, the rally faded ahead of Wednesday's Fed decision, which proved to be the week's dominant price catalyst. The FOMC held rates at 3.50-3.75% as expected, but the dot plot and press conference struck a decidedly hawkish tone. While the median projection still calls for one 25bp cut this year, 14 of 19 members now see one cut or fewer, a meaningful shift from December's wider distribution. The Fed raised its 2026 PCE inflation forecast to 2.7% from 2.4%, with Powell warning that the central bank was not making as much progress on inflation as it had hoped and acknowledging that surging oil prices had already filtered into projections. BTC fell roughly 5% within hours, sliding from above $74,000 to around $70,500.

The FOMC's hawkish stance set the tone for a coordinated global tightening of financial conditions on Thursday, as the Bank of England, ECB, and Bank of Japan all held rates steady, each citing the Iran war and rising energy costs as key sources of uncertainty. The synchronized holds effectively killed remaining hopes for near-term easing across developed economies. Notably, gold suffered a sharp 6% two-day decline post-FOMC, crashing below $5,000 and sliding to $4,700 by Thursday as rising real yields and a stronger dollar punished the traditional safe haven. Bitcoin's relative resilience through this period, holding above $70,000 while gold sold off aggressively, lent further support to the digital safe-haven narrative that has been building in recent weeks.

The Strait of Hormuz crisis continued to dominate the macro backdrop and whipsaw risk sentiment. A brief reprieve came Friday when Trump indicated he was considering winding down military efforts, but he reversed course over the weekend, issuing an ultimatum threatening to destroy Iran's power plants if the strait was not reopened within 48 hours. Iran responded by threatening indefinite closure, sending Brent crude to $114 at Sunday's open. The S&P 500 closed at 6,506 on Friday, extending its losing streak and sitting at its lowest level of 2026.

Despite the challenging macro environment, the week's regulatory developments were significant. Beyond the SEC/CFTC token taxonomy, Senators Tillis and Alsobrooks confirmed an agreement in principle on stablecoin yield on Friday, resolving the central dispute that had stalled the CLARITY Act since January. The deal prohibits passive yield on stablecoin balances while permitting activity-based rewards, clearing the path for a Senate Banking Committee markup in late April. Polymarket odds for the CLARITY Act being signed into law this year sit around 68%. Meanwhile, Morgan Stanley filed an amended S-1 for its spot Bitcoin ETF, positioning it as the first major U.S. bank to directly issue such a product. The week's regulatory progress was largely overshadowed by the macro environment, but it lays important groundwork that the market will likely revisit once conditions stabilize.

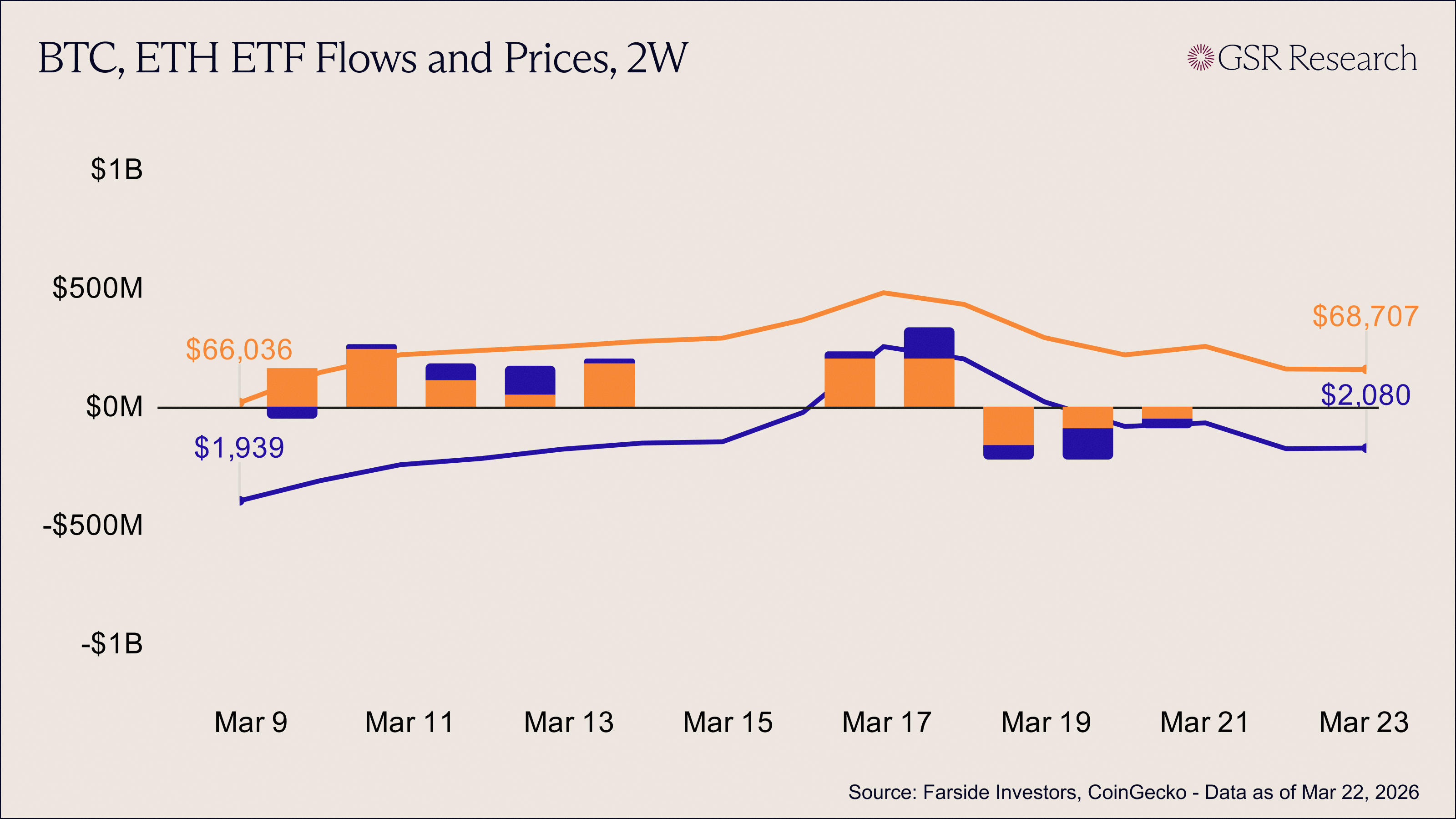

ETF flows flipped decisively negative this week, marking a sharp reversal from the prior stretch of relative stability. U.S. spot Bitcoin ETFs began the period with massive momentum, logging identical back-to-back creation days of +$199.4M on Monday and Tuesday. However, the tide turned abruptly on March 18, triggering three consecutive sessions of red tape (-$163.5M, -$90.2M, and -$52.0M). Despite the late-week exodus, the strong start allowed Bitcoin ETFs to finish the five-day trading session with a modest net positive of +$93.1M.

Ether ETF flows followed a more volatile trajectory, ultimately failing to maintain their early-week gains. The week opened with constructive interest (+$35.9M on Mar 16) and surged on Tuesday with a standout +$138.2M print. This optimism was short-lived, however, as Wednesday and Thursday saw heavy redemptions (-$55.7M and -$136.4M), with the latter marking the largest single-day outflow for Ether funds in over a month. After a final Friday giveback of -$42.0M, Ether ETFs closed the week with a net outflow of roughly -$60M, as investors moved to reduce exposure amid a broader cooling of the recent rally.

The price action mirrored this shift from aggression to caution. Bitcoin started the week at a high of $74,858, but failed to sustain its footing above the $74k level as the ETF bid evaporated. By Sunday, BTC had drifted down to $68,707, representing an 8.2% decline from its Monday peak. Ethereum’s underperformance was notably more pronounced; after reaching a weekly high of $2,351 on March 16, it struggled against the mid-week liquidity drain, sliding to $2,080 by the week's end—a total retracement of roughly 11.5%.

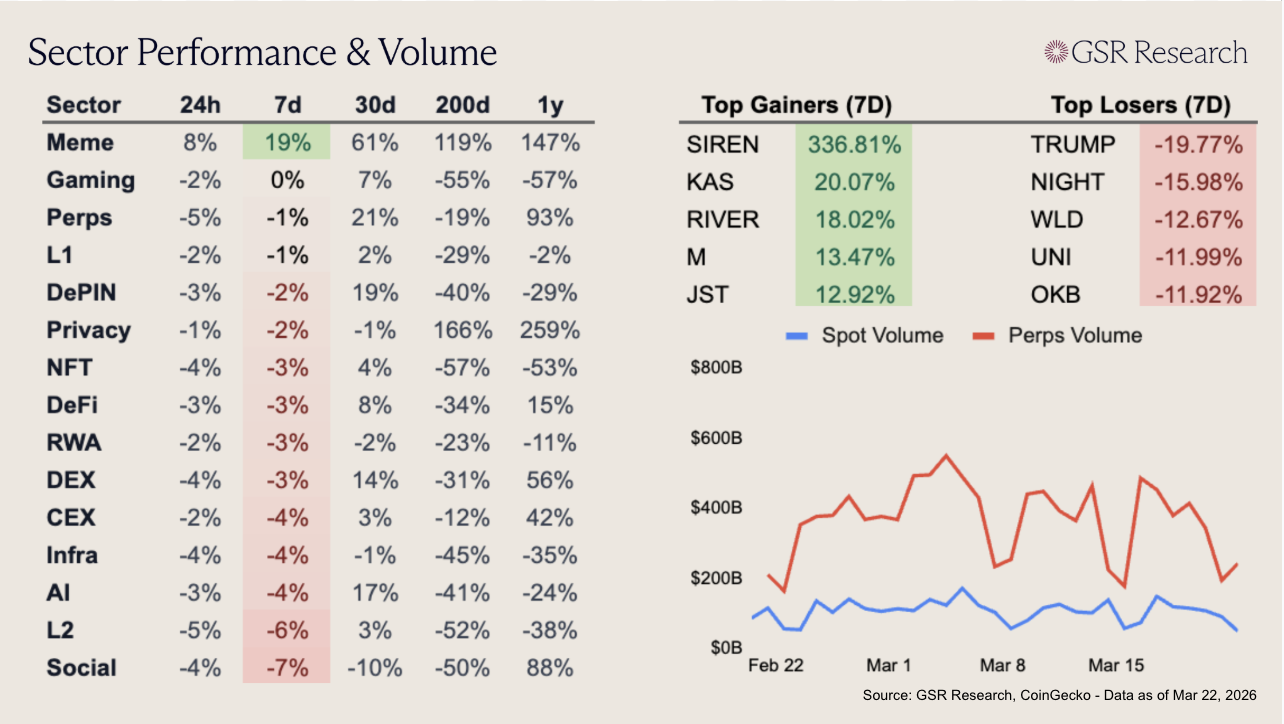

With the majors trading down on the week, altcoin performance remained subdued. The memecoin sector was the only category to post positive returns following a 337% increase in SIREN. Outside of memes, performance was muted to weak, with Gaming flat on the week and most other sectors slipping between 1% and 7%. Social (-7%) and L2 (-6%) were the worst performers, continuing their longer-term downtrends, now down 50% and 52% over 200 days respectively.

OKB (-11.92%) was among the top losers this week, with the token cooling off following the rally that occurred after OKX announced their partnership and investment from NYSE parent company Intercontinental Exchange half a month ago. KAS (+20.07%) is up on the week, as there has been renewed interest for high-throughput payment-focused networks with the agentic AI narrative re-ermerging.

Download the PDF of the full report here.

This material is provided by GSR (the “Firm”) solely for informational purposes. It is not intended to be advice or a recommendation to buy, sell or hold any investment mentioned. Investors should form their own views in relation to any proposed investment.

It is intended only for sophisticated, institutional investors and does not constitute an offer or commitment, a solicitation of an offer or commitment, or any advice or recommendation, to enter into or conclude any transaction (whether on the terms shown or otherwise), or to provide investment services in any state or country where such an offer or solicitation or provision would be illegal. The Firm is not and does not act as an advisor or fiduciary in providing this material.

This material is not an independent research report, and has not been prepared in accordance with any legal requirements by any regulator (including the FCA, FINRA or CFTC) designed to promote the independence of investment research.

This material is not independent of the Firm’s proprietary interests, which may conflict with the interests of any counterparty of the Firm. The Firm may trade investments discussed in this material for its own account, may trade contrary to the views expressed in this material, and may have positions in other related instruments. The Firm is not subject to any prohibition on dealing ahead of the dissemination of this material.

Information contained herein is based on sources considered to be reliable, but is not guaranteed to be accurate or complete. Any opinions or estimates expressed herein reflect a judgment made by the author(s) as of the date of publication, and are subject to change without notice. The Firm does not plan to update this information.

Trading and investing in digital assets involves significant risks including price volatility and illiquidity and may not be suitable for all investors. The Firm is not liable whatsoever for any direct or consequential loss arising from the use of this material. Copyright of this material belongs to GSR. Neither this material nor any copy thereof may be taken, reproduced or redistributed, directly or indirectly, without prior written permission of GSR.

Please see here for additional Regulatory Legal Notices relevant to US, UK and Singapore.