GSR Weekly Update - March 2nd, 2026

BTC: $66,125 (-0.1%) | ETH: $1,938 (+1.2%) | BTC Dom: 56.2% | Global Cap: $2.35T

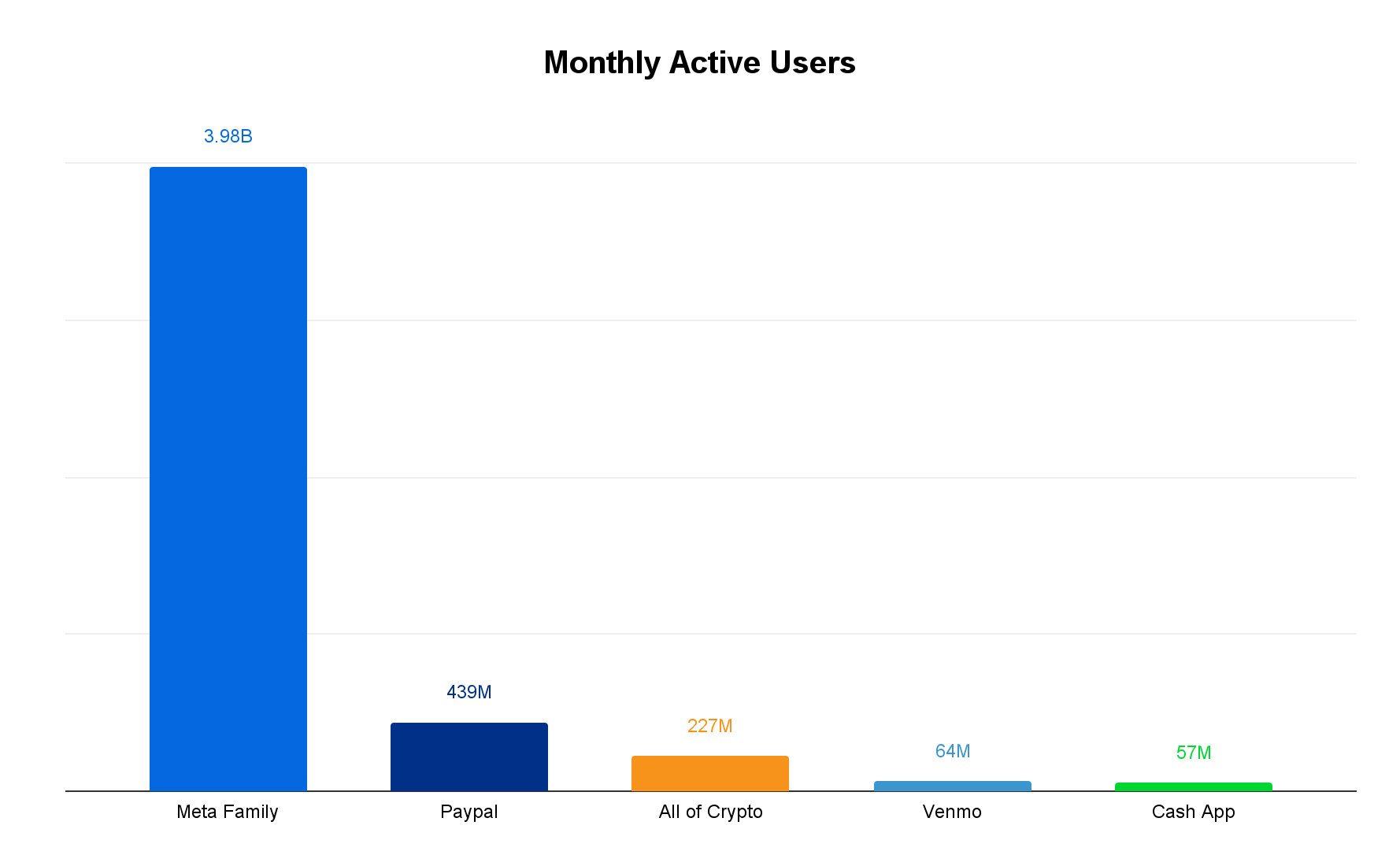

According to three sources who spoke with reporters at CoinDesk, Meta has sent out a request for proposal (RFP) to third-party providers to build a stablecoin-backed payments platform and in-house digital wallet, with plans to begin integration in the second half of this year. Stripe, which acquired stablecoin infrastructure firm Bridge for $1.1B in 2024, is reportedly the leading candidate, a natural fit given its existing payments partnership with Meta and CEO Patrick Collison's seat on Meta's board since April 2025. If it comes to fruition, the initiative would embed stablecoin payments into WhatsApp, Instagram, and Facebook, bringing crypto-native financial rails to a platform with nearly four billion monthly active users and potentially representing the single largest onboarding event for stablecoins in the technology's history.

Meta's interest in stablecoins is not new. In 2019, the company launched the Libra project, an ambitious effort to create a global digital currency backed by a basket of international currencies. The Libra Association, a consortium of 28 founding members including Visa, Mastercard, and PayPal, was designed to distribute governance across multiple entities, but the project drew immediate and fierce backlash from regulators worldwide who saw it as an attempt by a private company to usurp sovereign monetary authority. Under relentless political pressure, key partners dropped out, the project was scaled back and rebranded to Diem, and ultimately wound down in early 2022 after the Federal Reserve refused to greenlight its banking partner Silvergate to issue the token. The engineering team dispersed to found Aptos and Sui.

The regulatory landscape today bears little resemblance to 2019. The GENIUS Act has established a legal framework for stablecoin issuance in the U.S. for the first time, and Bridge received conditional OCC approval for a national trust bank charter in February 2026. Meta's approach has also changed fundamentally. Rather than trying to create its own currency and monetary infrastructure, Meta is positioning itself purely as a distribution layer for existing third-party stablecoins. This allows the company to offload the heavy burdens of KYC/AML compliance, reserve management, and regulatory oversight to specialized vendors while maintaining control over the user experience. In essence, Meta has traded the controversial ambition of creating a global reserve currency for the more defensible, but still highly ambitious, goal of becoming the world's dominant payments platform.

This shift in strategy may be more significant than it appears. In stablecoin payments, distribution is the moat. The rails and the assets are rapidly commoditizing, there will be many stablecoin issuers, and orchestration infrastructure is becoming standardized. The scarce resource is the direct relationship with billions of end users, and no company on earth has more of that than Meta. To put the potential impact in perspective: PayPal, one of the current leaders in digital payments in the West, has 439 million active users. Total crypto active addresses reached 227 million in December 2025, according to Token Terminal (though these include bots and secondary wallets, real active users are estimated to be a fraction of this). Even converting a small portion of Meta's user base would dwarf both figures. Meta has demonstrated this kind of transformative distribution power before, it turned WhatsApp into the global default for instant messaging and Instagram into the backbone of creator commerce. If it can do the same for stablecoin payments, making them seamless, global, and invisible to the end user, the impact on adoption would be massive.

Source: Statista, Token Terminal - Data as of Feb 27, 2026

There's also a longer-term dimension worth watching. During Meta's February 2026 earnings call, Zuckerberg described 2026 as the year of ‘Personal Superintelligence’, envisioning AI agents that know each user's history, preferences, and habits. A stablecoin-backed payments layer integrated with increasingly capable AI agents could eventually enable entirely new forms of autonomous financial interaction, agents that don't just recommend products but execute transactions, manage budgets, and negotiate on behalf of users. While still speculative, the convergence of Meta's AI ambitions with its payments infrastructure points toward a future where the boundaries between social, commercial, and financial experiences blur together.

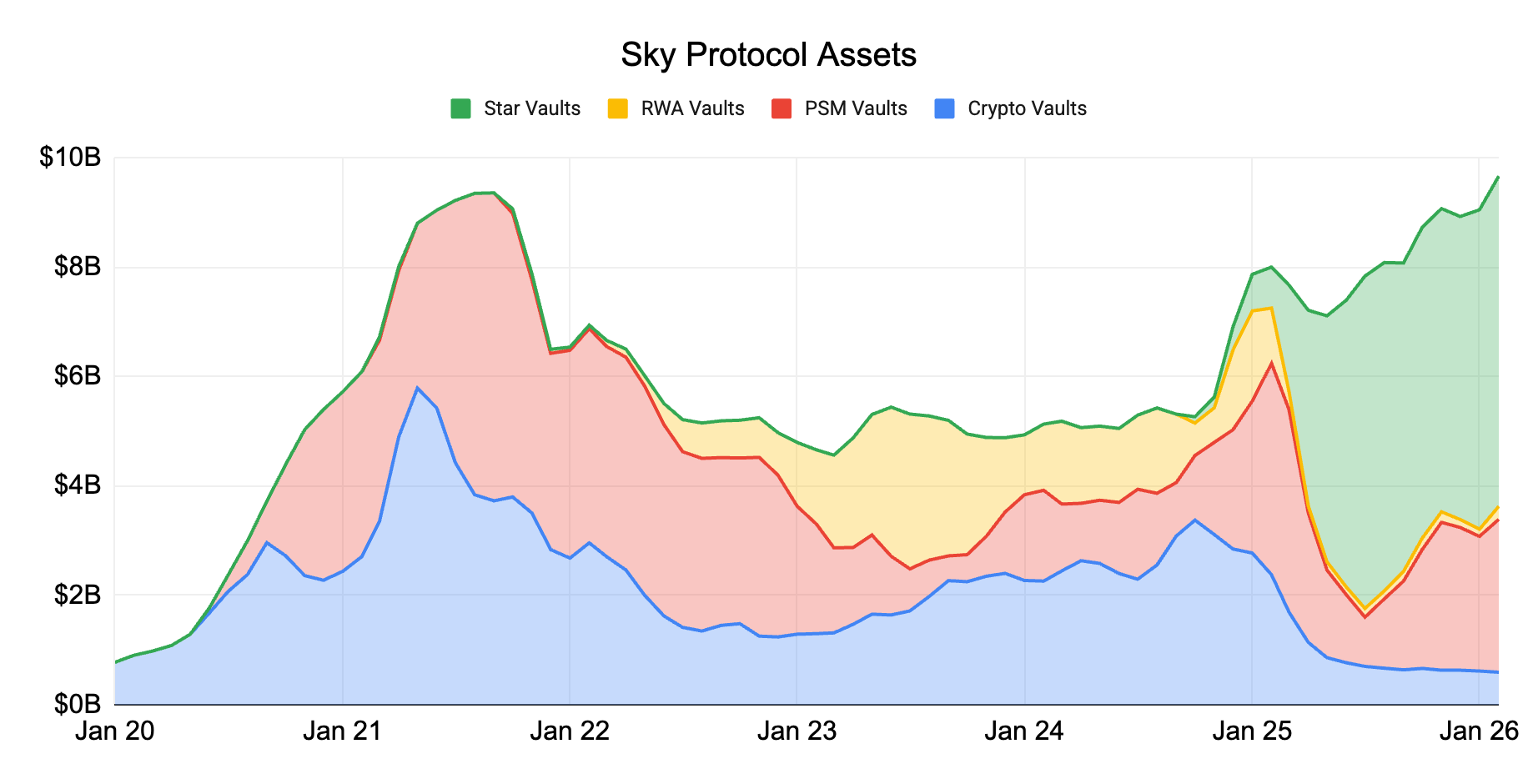

On Monday, AI-native mortgage lender Better and crypto venture firm Framework Ventures announced a strategic partnership that will see Better join Sky (formerly MakerDAO) as the ecosystem's home finance 'Star', gaining access to up to $500M in credit to fund mortgage originations. As part of the deal, Framework is acquiring a roughly 10% equity stake in Better for approximately $45M, and Better plans to issue yield-bearing tokens backed by its mortgage assets. Better intends to integrate into Sky's ecosystem through Obex, Framework's Sky-focused incubator backed by a $2.5B commitment from Sky. The partnership marks one of the most significant integrations of traditional consumer lending into DeFi to date, and offers a window into how crypto and real-world economic activity are increasingly converging.

At its core, the deal restructures how mortgage funding works. Traditionally, mortgage originators like Better rely on bank warehouse lines of credit and securitization markets to fund their lending. These channels work, but involve multiple layers of intermediation, warehouse lenders, investment banks, rating agencies, trustees, and servicers, each extracting fees and adding delays. Better claims that by drawing funding directly from Sky's stablecoin ecosystem, it can remove several of these intermediary layers and reduce its funding costs by more than 100 basis points annually. If realized, this could translate into mortgage rates below 5% for its borrowers at a time when the industry is generally charging over 6%. Better will retain full responsibility for underwriting and origination, with the Sky Star providing an alternative source of warehouse funding secured by originated assets.

The partnership is also noteworthy for the particular form of crypto-TradFi integration it represents. Much has been made of the 'DeFi mullet' model, where a fintech frontend provides a familiar user experience while accessing onchain rates and liquidity on the backend. The Better–Sky integration is fundamentally different. Here, the blockchain infrastructure operates at the wholesale level as a global capital aggregation and funding mechanism, entirely invisible to the borrower. A homebuyer taking out a mortgage through Better would have no idea crypto is involved. Meanwhile, asset origination occurs entirely in traditional finance through Better's AI-powered Tinman underwriting platform. In a sense, this model represents an unbundling, modularization, and rebundling of the traditional banking function: Better specializes in underwriting and origination, while Sky handles funding on the backend through its onchain capital formation infrastructure. Each component does what it does best, and the result is a more efficient, modular system that reduces costs for all participants.

Sky's ecosystem is built for this kind of integration. The protocol deploys capital through a modular structure of semi-autonomous 'Stars', each focused on a different sector. Spark, the first and largest Star, is a DeFi lending protocol and capital allocator managing roughly $5B in TVL, deploying stablecoin liquidity across DeFi, CeFi, and tokenized treasuries. Grove focuses on institutional credit strategies like collateralized loan obligations, having secured $1B in allocations from Sky. Keel operates as Sky's capital allocator on Solana, backed by a $2.5B commitment to bring real-world assets onchain across that ecosystem. Better is entering the Sky ecosystem through Obex, an incubator administered by Framework that identifies and onboards new Stars into the network. Its addition brings a major new asset class, U.S. conforming mortgages (a $12T+ market) onto Sky's growing balance sheet.

Source: Dune Analytics (Steakhouse Financial) - Data as of Mar 1, 2026

Importantly, the mortgage-backed tokens that emerge from this model don't exist in a vacuum. Once onchain, they become composable within the broader DeFi ecosystem, opening up novel possibilities. Token holders could potentially use them as collateral in lending markets like Morpho, or trade the associated yields in rates markets like Pendle, financial use cases that are difficult or impossible to replicate efficiently in traditional markets. This composability is one of the key advantages that tokenization brings to traditional asset classes, enabling a broader range of financial products and participants to interact with what would otherwise be siloed, illiquid instruments. If this model proves successful, it could serve as a template for bringing other large real-world asset classes into DeFi's composable financial infrastructure.

Source: CoinGecko, GSR - Data as of Mar 1, 2026

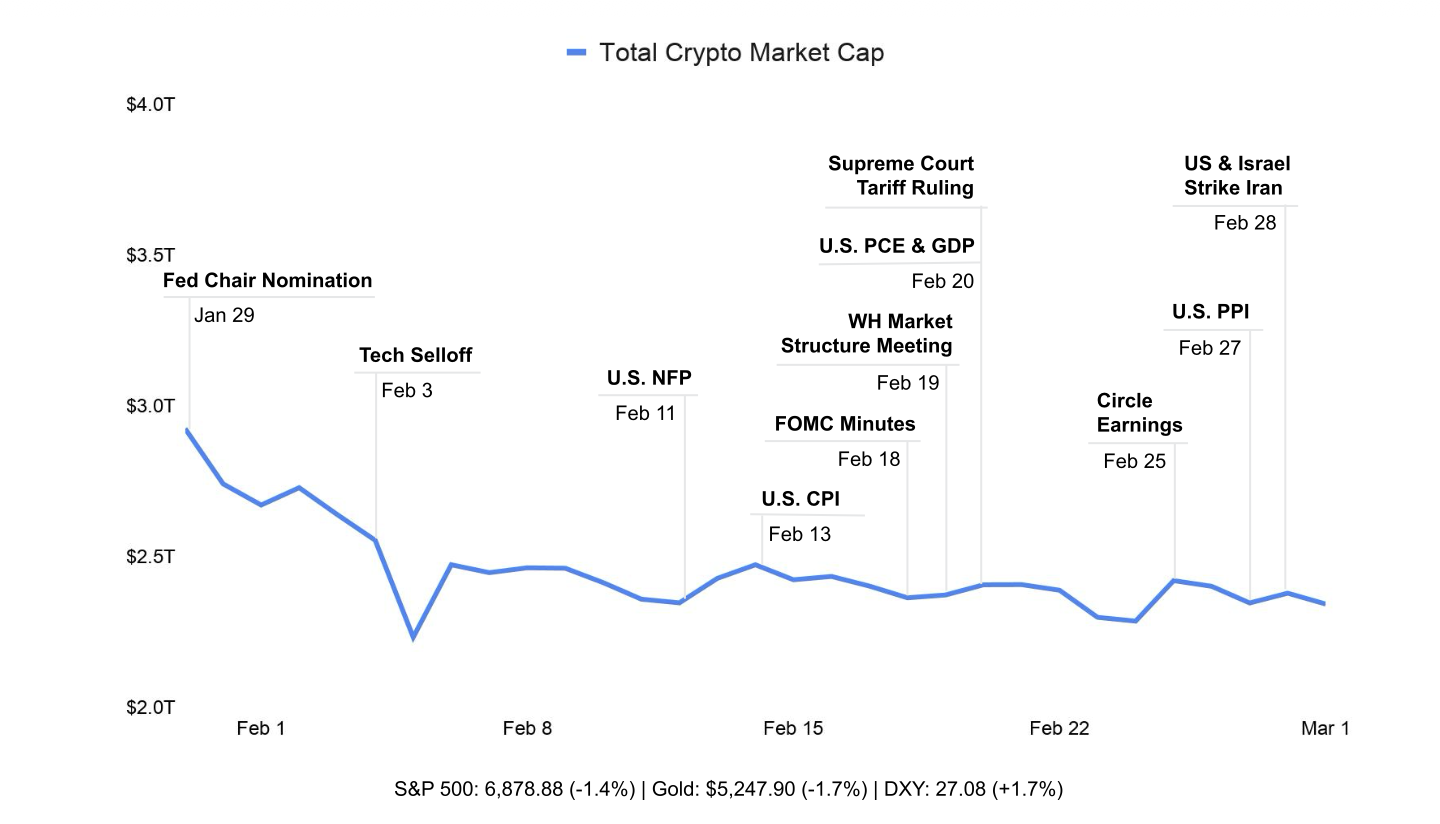

After a period of cautious consolidation, crypto markets experienced a volatile, but largely range-bound, final week of February, with a rally mid-week and a geopolitically-led correction over the weekend. The total market cap spent the early part of the week hovering near $2.3T before a decisive catalyst arrived on Wednesday. Many participants had anticipated volatility surrounding President Trump’s State of the Union address, but perhaps the larger driver of positive momentum was Circle’s blockbuster Q4 2025 earnings report, which acted as a powerful validation of the stablecoin-driven business model and sparked a broad-based recovery.

Circle’s results comfortably beat Wall Street expectations, with the company reporting $770 million in total revenue and reserve income, a 77% year-over-year increase, and highlighting that on-chain USDC transaction volume reached $11.9 trillion in the final quarter of 2025, representing explosive 247% growth. Following the release, Bitcoin recovered from its early-week lows to test the $69,000 level as risk appetite briefly returned to the market. This rally was further aided by a significant regulatory milestone on Wednesday, when the OCC issued a 376-page proposal to implement the GENIUS Act. The proposal creates a formal federal framework for stablecoin issuers, effectively bringing them into the regulatory fold. Notably, the proposal blocks several workarounds to the GENIUS Act’s prohibition on stablecoin yield, a move that appears to have cleared a major hurdle for the market structure legislation being debated in the Senate. By removing this long-standing point of contention, the OCC's stance boosted market expectations for the passing of the Clarity Act, with Polymarket odds for the bill's passage jumping to over 70%.

However, this optimism was curtailed by persistent macro headwinds on Friday. The release of higher-than-expected Producer Price Index (PPI) data pointed to persistent inflation, cooling expectations for Fed easing. This sent the DXY (Dollar Index) climbing to 27.08, a 1.7% increase on the week, which exerted immediate downward pressure on Bitcoin and other risk assets. The tightening environment was further strained by the week's most significant event: coordinated U.S. and Israeli military strikes against Iran on February 28. The geopolitical shock triggered a weekend risk-off liquidation, sending Bitcoin back toward $66,000.

Source: Farside Investors, CoinGecko - Data as of Mar 1, 2026

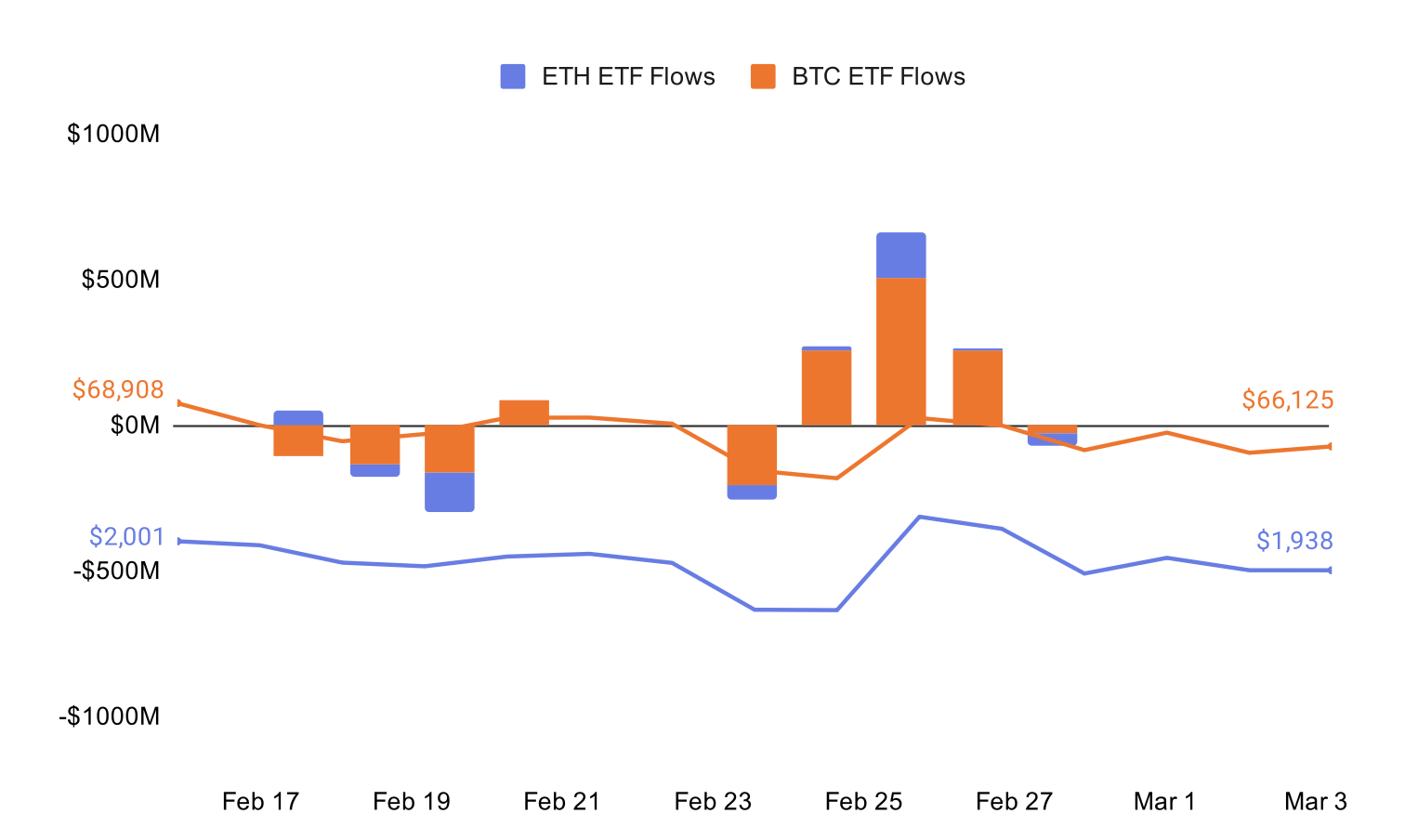

ETF flows were more constructive this week, shifting from the prior run of mostly-red sessions. U.S. spot Bitcoin ETFs experienced a high Monday redemption (-$204M on Feb 23), but then logged three outsized creation days midweek (+$258M on Feb 24, +$507M on Feb 25, and +$254M on Feb 26) before finishing with a small Friday giveback (-$28M on Feb 27), for a net +$787M across the five sessions. U.S. spot ETH ETFs also flipped positive, driven by a strong Feb 25 print (+$157M) that outweighed outflows on Feb 23 (-$50M) and Feb 27 (-$43M), leaving net +$81M on the week. Despite the improved ETF tape, majors were still choppy: BTC moved from ~$68.7k to ~$66.1k, while ETH was roughly flat from ~$1,964 to ~$1,970, after briefly reclaiming the $2k handle midweek.

Source: CoinGecko, GSR - Data as of Mar 1, 2026

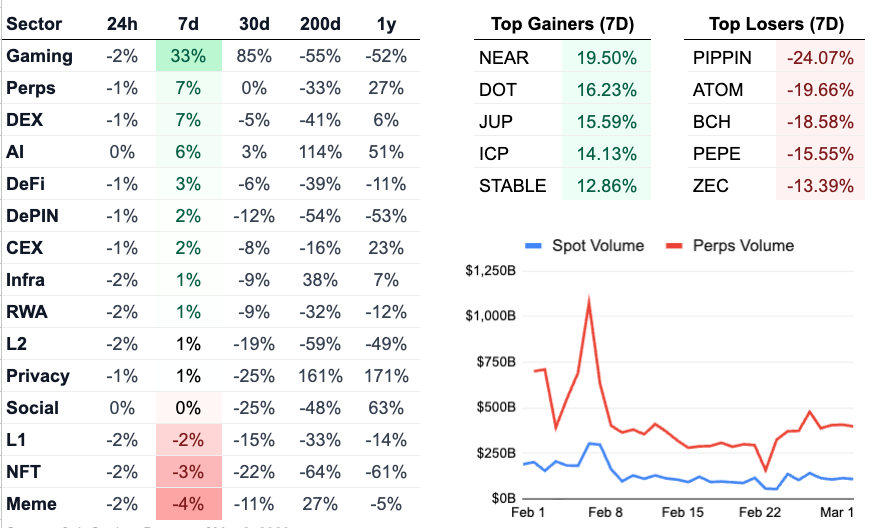

The gaming sector is the clear winner this week, up 33%. The surge in the gaming sector is driven by a 308% increase in Power protocol, an entertainment infrastructure layer. The recent performance of the sector also means that it is now the top performing category on a 30d time frame, and by a wide margin. The AI and Perps sectors remain the only other positive performers over the past month.

The social sector continues to bleed, due to losses in Zora (-12%) and Decentralized Social (-9.4%). The SocialFi category has failed to generate positive momentum after Farcaster reportedly sold for much less than its prior $1B valuation venture round.

NEAR (+20%) was the top performer this week following its successful NearCon event in San Francisco, which included the reveal of several AI-related products and features, along with important protocol upgrades. The same cannot be said for Zcash (-13%), which is once again among the top losers. GSR has published 4 updates since we first debuted our weekly newsletter on February 9th, and while Zcash was a top performer for our second edition, the token was among the top losers for the other 3. The project has recently been undergoing a correction following its historic rally last year, and has lost momentum amid the ongoing governance uncertainty following the resignation of the core development team and their subsequent spin-out to launch the cashZ wallet.

This material is provided by GSR (the “Firm”) solely for informational purposes. It is not intended to be advice or a recommendation to buy, sell or hold any investment mentioned. Investors should form their own views in relation to any proposed investment.

It is intended only for sophisticated, institutional investors and does not constitute an offer or commitment, a solicitation of an offer or commitment, or any advice or recommendation, to enter into or conclude any transaction (whether on the terms shown or otherwise), or to provide investment services in any state or country where such an offer or solicitation or provision would be illegal. The Firm is not and does not act as an advisor or fiduciary in providing this material.

This material is not an independent research report, and has not been prepared in accordance with any legal requirements by any regulator (including the FCA, FINRA or CFTC) designed to promote the independence of investment research.

This material is not independent of the Firm’s proprietary interests, which may conflict with the interests of any counterparty of the Firm. The Firm may trade investments discussed in this material for its own account, may trade contrary to the views expressed in this material, and may have positions in other related instruments. The Firm is not subject to any prohibition on dealing ahead of the dissemination of this material.

Information contained herein is based on sources considered to be reliable, but is not guaranteed to be accurate or complete. Any opinions or estimates expressed herein reflect a judgment made by the author(s) as of the date of publication, and are subject to change without notice. The Firm does not plan to update this information.

Trading and investing in digital assets involves significant risks including price volatility and illiquidity and may not be suitable for all investors. The Firm is not liable whatsoever for any direct or consequential loss arising from the use of this material. Copyright of this material belongs to GSR. Neither this material nor any copy thereof may be taken, reproduced or redistributed, directly or indirectly, without prior written permission of GSR.

Please see here for additional Regulatory Legal Notices relevant to US, UK and Singapore.