Highlights

Tether Engages KPMG for Big Four Audit

Last week, Tether announced it engaged a Big Four audit firm (later revealed to be KPMG) to conduct its first full financial statement audit, covering the $184 billion in assets backing USDT, the world's largest stablecoin. The company also retained PwC to prepare its internal systems ahead of the review. The audit goes well beyond the monthly attestations Tether has published through BDO Italia since 2022, extending to a comprehensive examination of assets, liabilities, internal controls, and governance. The move comes as Tether pursues a U.S. expansion under the GENIUS Act, having already launched USAT, a compliant stablecoin, in January. For a company that has spent a decade resisting this level of scrutiny, the decision to submit to Big Four oversight is a clear signal that the stablecoin market has entered a new phase of institutionalization.

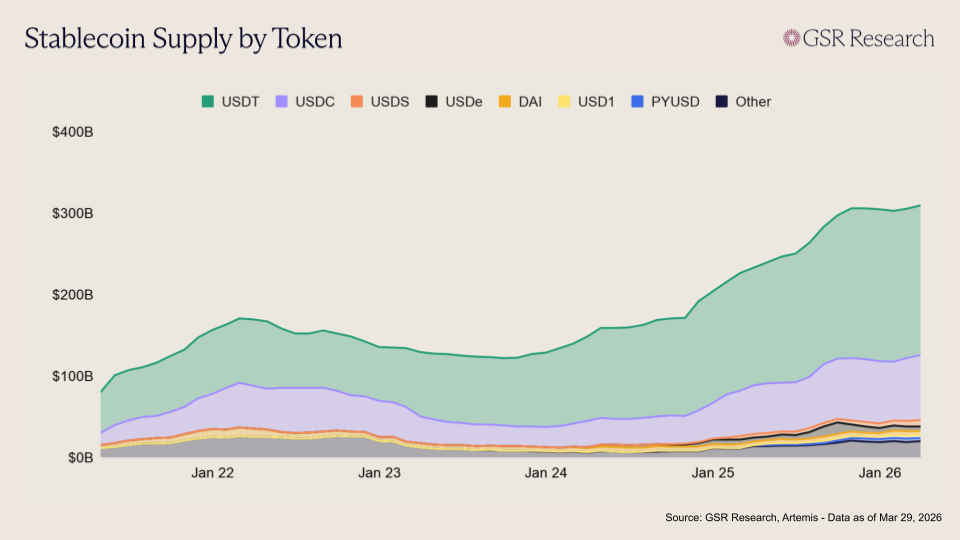

The market's growth supports that reading. Total stablecoin supply has surpassed $300 billion, up from roughly $205 billion at the start of 2025 and less than $30 billion in 2020. The passage of the GENIUS Act in July 2025, which established the first federal regulatory framework for stablecoins in the U.S., has accelerated institutional engagement across the board. SoFi became the first national bank to issue a stablecoin on a public blockchain, JPMorgan launched a deposit token on Coinbase's Base, Fiserv announced its entry into the space, and a consortium of ten European banks including ING, UniCredit, and BNP Paribas began building a MiCA-compliant euro stablecoin, with Bank of America, Wells Fargo, and Citigroup all signaling readiness to follow. More recently, Visa's stablecoin settlement hit a $4.5 billion annualized run rate by January 2026, and just two weeks ago Mastercard acquired stablecoin infrastructure provider BVNK for up to $1.8 billion. The infrastructure layer is maturing rapidly, and Tether's audit represents a meaningful step forward in this process.

However, the headline numbers obscure a more nuanced picture of where stablecoins are actually being used. A joint analysis by McKinsey and Artemis Analytics published in February found that only about $390 billion of the $35 trillion in annual stablecoin transaction volume represents actual payments, including commercial transfers, settlement, payroll, and remittances. The vast majority of on-chain stablecoin activity still consists of trading, internal rebalancing between exchange wallets, automated smart contract interactions, and other crypto-native flows. That $390 billion figure, while more than double the 2024 level, amounts to roughly 0.02% of global payments volumes.

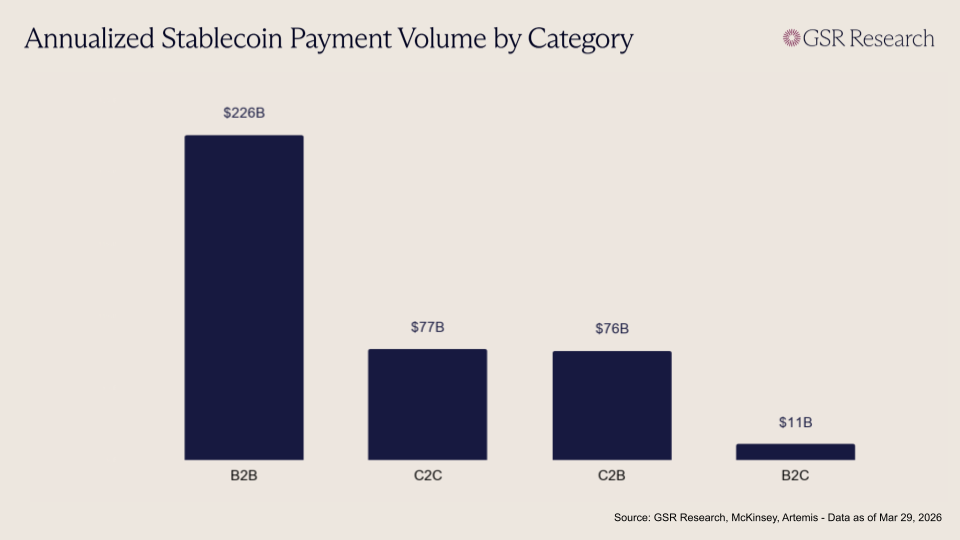

Although actual payment volumes are low compared to total stablecoin transaction volume figures, and compared to payment volumes on traditional financial rails, several use cases are growing rapidly. B2B payments account for the largest share at approximately $226 billion annually, or about 60% of total stablecoin payment volume. This segment has grown 733% year-over-year, driven by businesses using stablecoins to streamline cross-border supply chain payments and improve liquidity management, particularly small and medium-sized enterprises operating in corridors where traditional banking rails are slow and expensive. Stablecoin-linked card spending, while still relatively small in absolute terms at $4.5 billion, grew 673% year-over-year. Geographically, stablecoin payments are heavily concentrated in Asia, with Singapore, Hong Kong, and Japan accounting for approximately 60% of total volume.

Stablecoins are gaining traction where they solve specific, tangible problems such as the cost, speed, and complexity of cross-border business payments; the friction in remittance corridors underserved by traditional banking; and the settlement delays that lock up capital in clearinghouse intermediaries. However, penetration into the broader global payments landscape remains limited. The gap between the market's $310 billion in circulating supply and its $390 billion in annual payment throughput underscores how much of the current ecosystem remains oriented toward trading and DeFi rather than real-economy use cases.

Despite the overall excitement and high expectations for the sector, real adoption is still early. Further growth will likely be unlocked as rules are made clearer and institutions become more comfortable. Key enablers will be the finalization of GENIUS Act technical standards by the OCC and Federal Reserve, and the continued build-out of infrastructure connecting stablecoin rails to existing payment networks. Tether's KPMG audit matters less for what it will reveal about reserve quality and more for what it represents. The largest stablecoin issuer in the world is voluntarily submitting to the same standards that govern traditional financial institutions. This represents a major milestone on the continued path to mainstream adoption, even if the payment volumes have not yet caught up.

ICE Doubles Down on Polymarket Investment

On March 27, Intercontinental Exchange, the parent company of the New York Stock Exchange, announced a $600M investment in Polymarket and declared its intention to purchase up to an additional $40M of shares from existing holders. The tranche completes ICE’s obligations under the investment arrangement first announced in October 2025, when it agreed to invest up to $2B in Polymarket at an approximately $8B pre-money valuation. Key terms, including the valuation of the March 2026 investment, are expected to be disclosed only after Polymarket finishes broader fundraising. With event markets increasingly scaling into meaningful global volume, the investment signals ICE’s desire to close the loop on a partnership that turns crowd-sourced probabilities into institutional-grade datasets.

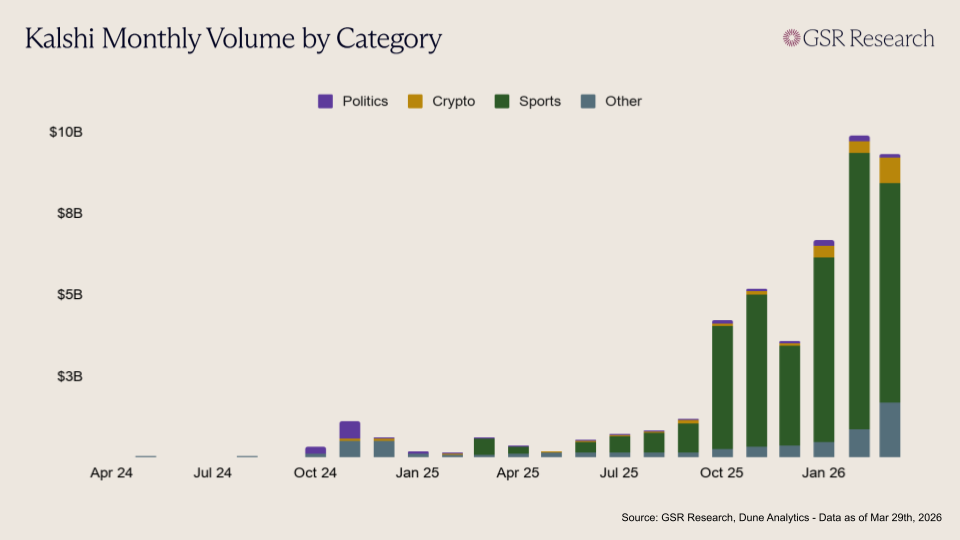

Prediction markets have grown into a meaningful market segment over the past year. TRM Labs noted that prediction market volume grew from roughly $1.2B per month in early 2025 to more than $20B by January 2026, with about 840,000 unique wallets participating monthly. This is primarily due to the rise in popularity of Kalshi, Polymarket’s centralized counterpart. While Polymarket maintains a more diversified mix of event categories, Kalshi remains heavily reliant on sports markets for most of its trading. Despite its core product facing active legal and political challenges over whether certain contracts are better understood as gambling, Kalshi is still effectively valued as exchange infrastructure the same way Polymarket is. The company’s recent $1B raise at a $22B valuation in March was roughly double its prior valuation just three months earlier. Even amidst the regulatory turbulence, private investors are clearly pricing event-contract trading, and prediction markets more generally, as a durable category.

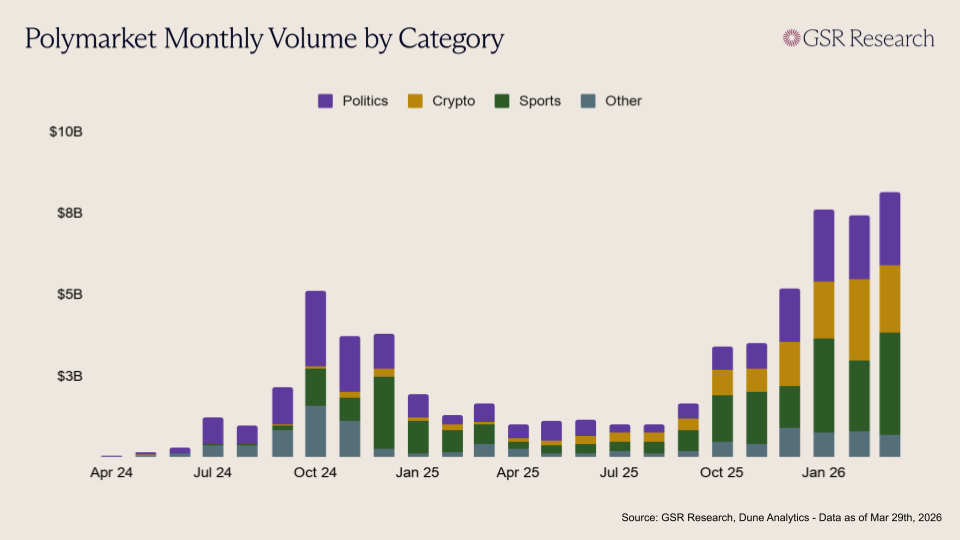

Kalshi’s distribution and regulatory posture have made it the easiest sports-adjacent prediction venue for US users to access at scale. The platform launched sports event contracts in all 50 states in January 2025, and found product market fit through partnerships that surfaced its prediction markets to large retail audiences, most notably through Robinhood. While sports-related markets account for less than 37% of Polymarket’s cumulative volume, 82% of Kalshi’s lifetime activity is tied to sports. Additionally, sports betting comprised nearly 88% of Kalshi’s volume in January and February, illustrating a persistent reliance on the sector rather than a shift toward diversification.

For Polymarket however, recent activity has shifted away from crypto and sports toward politics. Iran-related markets helped the protocol achieve a single-day record of $425M in volume on February 28, with the “Will the US strike Iran?” market alone doing $253M. These markets have increasingly functioned as real-time indicators of global events rather than just simple trading products, underscoring ICE’s continued interest in the platform as an institutional data source.

Polymarket’s lower sports dominance is not because the platform lacks a sports product-market fit. It is simply because Polymarket has already captured an identity as the venue where people express views on politics, macro, and global events, and where those views translate into a live probability feed that is increasingly discussed outside crypto-native circles. That identity is precisely what ICE is buying into when it positions itself as the global distributor of Polymarket’s event-driven data. While ICE benefits from exposure to Polymarket’s surging retail volume, the investment’s primary thesis isn't driven by transaction fees or trading activity. During the announcement of the partnership last year, ICE framed Polymarket less as a wagering product and more as a new data layer whose event-driven probabilities could be distributed to institutional clients and eventually paired with tokenization initiatives. Ultimately, ICE views Polymarket’s real-time predictive data as a highly functional addition to its existing suite of global market information.

Similarly, for Kalshi, institutional investors remain less interested in surging volumes and profits, and more intrigued by the potential data unlocks the platform can offer. Last week, ARK Invest announced a partnership with Kalshi where ARK will use the company's data to inform investment strategy and request markets tied to business metrics, industry developments, and macro outcomes. ARK noted several use cases that go beyond simple speculation, including market-based research signals, KPI-linked forecasting, and event-specific hedging.

Prediction market data is particularly compelling for institutions simply because of how cleanly it maps to tradable outcomes. Traditional instruments like options or swaps bundle together multiple variables, making it difficult to isolate whether a view is truly mispriced or simply already reflected in the market. A hedge fund trading rates, FX, or options around events like CPI prints or Fed decisions can be directionally correct and still lose money due to volatility or positioning dynamics. Prediction markets remove all ambiguity. By expressing a view as a discrete probability, investors know exactly what is being priced and what they are paying for, with no volatility drag or hidden assumptions embedded in the trade. This creates a cleaner form of hedging, where returns are tied directly to a single outcome rather than a basket of correlated factors. In an environment where macro assets increasingly react to a wide range of unpredictable inputs, the ability to isolate specific events is highly valuable. Additionally, there is a growing opportunity set around arbitrage, as probabilities implied in prediction markets often diverge meaningfully from those embedded in traditional options markets. For sophisticated players, this gap represents a new source of alpha, and one that is likely to compress as more institutional capital enters the space.

Regulation remains the biggest swing factor for prediction markets. A bipartisan Senate bill introduced on March 23 would ban sports-related and casino-style contracts on CFTC-regulated prediction platforms, a move that would hit Kalshi’s current mix hardest. At the same time, both Kalshi and Polymarket have already begun tightening insider trading restrictions and market integrity policies as scrutiny rises. If regulation turns restrictive, the sector may be pushed faster toward macro, politics, and KPI-linked markets, which would decimate Kalshi’s current volumes. If it turns permissive, the likeliest outcome is segmentation rather than winner-take-all: Kalshi as the sports-led U.S. retail venue, and Polymarket as the global market for event probabilities.

The two leading platforms now appear to be carving out different positions. Kalshi looks best suited to high-frequency U.S. retail flow, particularly through sports, which remains its dominant volume engine. Polymarket looks better positioned to own the information markets narrative, especially in politics and macro, where the product doubles as a monetizable data feed. Rather than treating Polymarket as just another trading venue, ICE is effectively treating it as a new probability layer for institutional finance. In either case, the latest funding rounds underscore a clear point: prediction markets are no longer being treated as simple speculative platforms. They are increasingly being valued as both a separate data product, and a potential building block of modern institutional finance.

Market Update

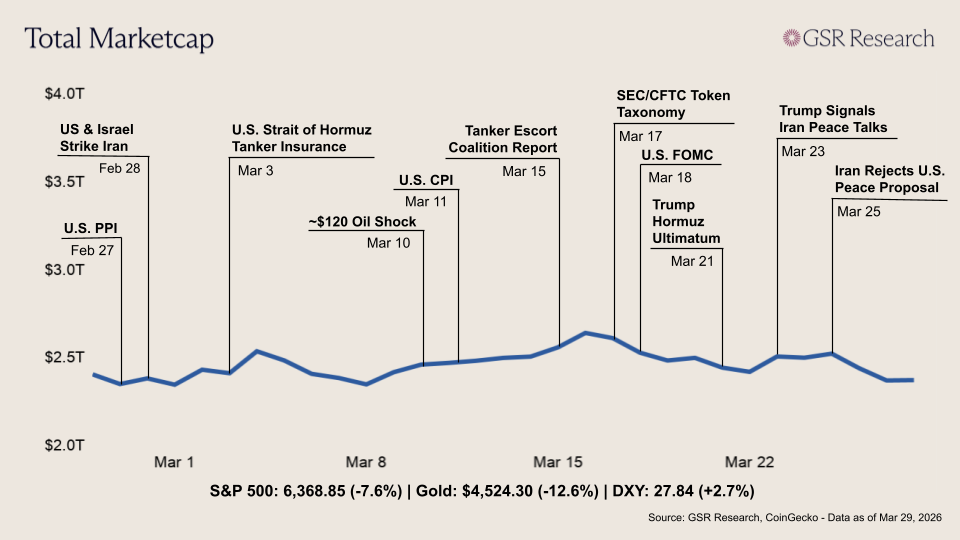

Crypto markets extended their decline for a second consecutive week as the Iran war's economic fallout intensified and diplomatic hopes faded. The total crypto market cap opened near $2.4T, and BTC initially rallied back above $72,000 after Trump signaled "very good and productive conversations" with Iran over the weekend into Monday. But the reprieve proved short-lived. By midweek, Iran had formally rejected the U.S. peace proposal and outlined five conditions for ending the conflict, while Israel launched a fresh wave of strikes on Iranian infrastructure and reportedly killed the head of the IRGC's navy. Trump responded on Thursday by extending his threat to destroy Iran's power plants by ten days to April 6, removing the near-term tail risk of imminent escalation but keeping the overhang firmly in place. Brent crude, which had briefly dipped below $100 early in the week on diplomatic optimism, surged back to close above $110 on Friday as a return to open commercial shipping remains distant.

The oil shock's second-order effects began to surface in U.S. economic data. The University of Michigan's final March consumer sentiment reading, released Friday, fell to 53.3, marking the lowest level since late 2025. Year-ahead inflation expectations jumped to 3.8% from 3.4%, the largest monthly increase since April 2025, with the survey director citing escalating gas prices and volatile financial markets as the primary drivers. Meanwhile, the S&P Global U.S. Manufacturing PMI came in at 52.4 on Tuesday, above expectations, though the internals were less encouraging as input and output prices surged on war-related cost pressures. Against this backdrop, the S&P 500 posted its fifth consecutive losing week, closing at 6,369 at its lowest level of 2026. BTC slid to around $66,500 by Sunday.

Despite the challenging macro environment, the week delivered notable progress on the regulatory and institutional front. SEC Chairman Paul Atkins keynoted the Digital Asset Summit in New York on Tuesday, calling the prior week's SEC/CFTC token taxonomy "the end of the beginning" and emphasizing ongoing inter-agency collaboration to build a broader framework for digital assets. On the same day, the NYSE and Securitize announced a memorandum of understanding to develop a tokenized securities platform supporting 24/7 trading and on-chain settlement, with Securitize named as the first digital transfer agent eligible to mint blockchain-native securities. However, the CLARITY Act's path forward hit a fresh obstacle. Just days after Senators Tillis and Alsobrooks announced what appeared to be a breakthrough agreement in principle on stablecoin yield, Coinbase rejected the updated compromise, citing significant concerns over provisions that would prohibit exchanges from paying rewards on stablecoin balances. The pushback was a sharp reversal from the optimism of a week earlier and complicates the legislative timeline, though White House crypto adviser Patrick Witt sought to play down the setback. As with the prior week, the regulatory progress was largely overshadowed by macro headwinds, but the accelerating convergence between traditional finance infrastructure and crypto rails continues to lay groundwork that markets will likely reprice once the geopolitical fog lifts.

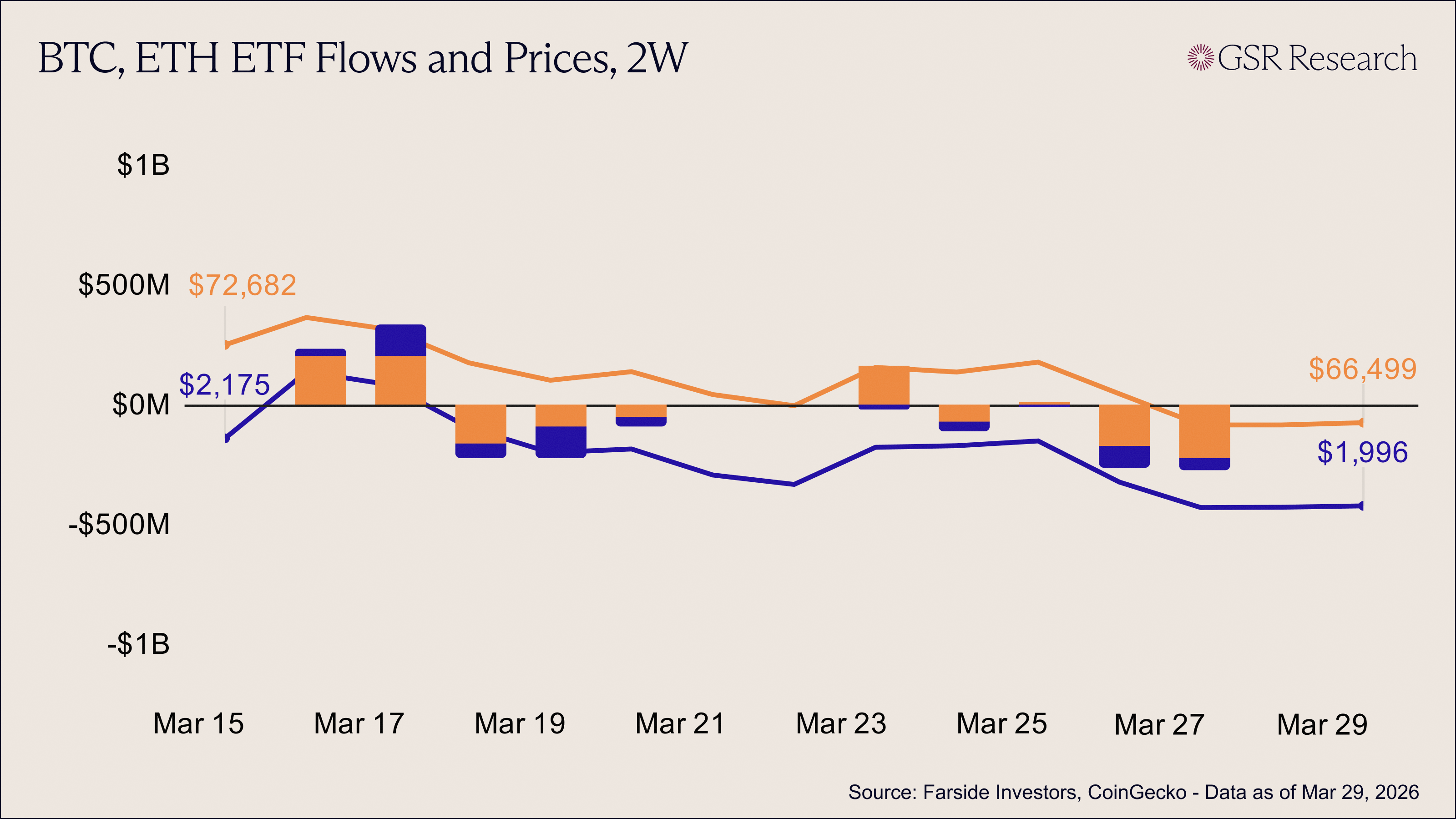

Source: Farside Investors, CoinGecko - Data as of Mar 29th, 2026

ETF flows took a decidedly bearish turn this week, as an early-session attempt at a recovery was swiftly overwhelmed by a heavy wave of late-week redemptions. U.S. spot Bitcoin ETFs began the period on a high note, logging a strong +$167.2M inflow on Monday (Mar 23), but the momentum collapsed as the week progressed. After a choppy midweek that saw a sharp exit on Tuesday (-$74.5M) and a negligible bounce on Wednesday (+$7.8M), there was a sharp selloff across the final two sessions. Massive outflows on Thursday (-$171.3M) and Friday (-$225.5M) left the weekly net at a staggering -$296.3M, marking one of the more aggressive institutional retreats in recent months.

Ether ETF flows remained under pressure, failing to post a single positive session across the entire five-day trading window. The week was characterized by a consistent bleed, starting with modest redemptions (-$16.2M and -$40.7M) before accelerating into a significant capitulation event on Thursday with a -$92.5M print. By the time the Friday closing bell rang with another -$48.5M exit, ETH ETFs had shed a total of -$206.4M for the week. This relentless selling pressure highlights a continued lack of appetite for Ether relative to Bitcoin, as investors appear to be de-risking from the second-largest asset more aggressively during periods of macro uncertainty.

Against this backdrop of deteriorating liquidity, price action for the majors was predictably bleak. Bitcoin, which started the week showing strength near $70.9k and briefly touched $71.3k, suffered a near-vertical descent as the ETF redemptions accelerated, finishing the week at $66.3k (a -6.5% WoW drop). Ethereum’s struggle was even more pronounced; after failing to hold the $2,100 level early in the week, it plummeted to $1,992 by Friday. By losing the psychologically significant $2,000 handle, ETH has once again entered a range of technical weakness, underperforming BTC as the ETH/BTC cross continues to face headwinds.

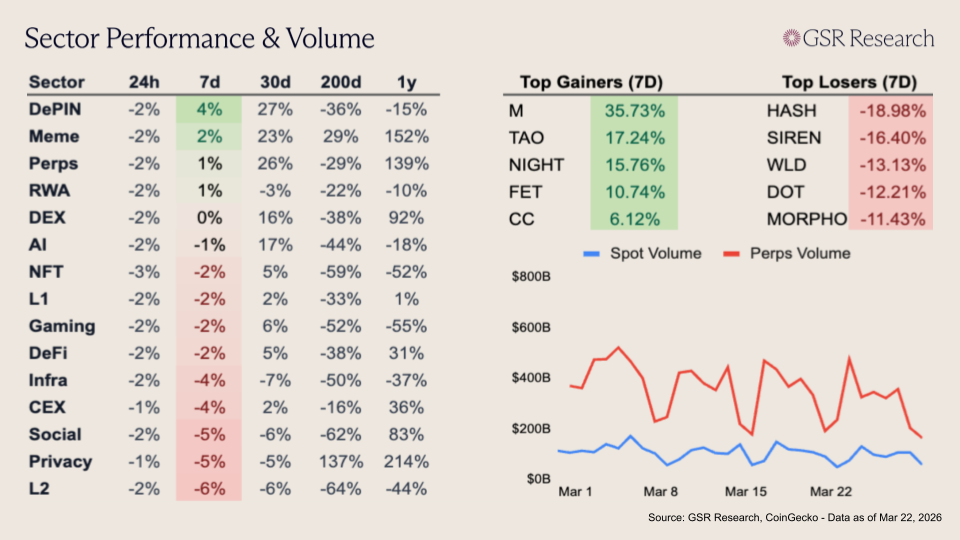

Sector Performance & Volume

Despite a relatively muted week for the broader market, a few sectors managed to post modest gains. The DePIN sector is this week’s winner, led by rallies in TAO (+17.24%) and RNDR (+6.0%). The sector’s surge is largely a spillover from the increasing agentic AI narrative, where decentralized hardware is increasingly viewed as a foundational component in the next wave of AI evolution. Bittensor specifically continues to capture institutional attention through its subnet ecosystem (now exceeding 120 subnets), and is additionally bolstered by recent technical collaborations with Intel on decentralized hardware.

MORPHO (-11.4%) was among the top losers this week, giving back recent gains as momentum around DeFi names cooled despite continued progress on institutional integrations and lending market expansion. Meanwhile, HASH (-19.0%) was the worst performer on the week, alongside SIREN (-16.4%), which saw a sharp reversal after leading gains last week. Worldcoin and Polkadot also experienced significant losses, down 13.13% and 12.21% on the week respectively.

The Week Ahead: What to Watch

- Tuesday, Mar 31 – Fourth FTX Creditor Distribution ($2.2B)

- Tuesday, Mar 31 – Tokyo CPI

- Tuesday, Mar 31 – Europe HICP Inflation

- Wednesday, Apr 1 – U.S. ADP Employment Change Report

- Wednesday, Apr 1 – U.S. Retail Sales

- Wednesday, Apr 1 – ISM Manufacturing PMI

- Friday, Apr 3 – U.S. Nonfarm Payrolls

- Friday, Apr 3 – ISM Services PMI

- Sunday, Apr 5 – OPEC+ Meeting

Other Stories

- Coinbase declines to support updated market structure bill draft

- White House clears review of rule allowing alternative 401(k) investments

- Fanny Mae announces it will accept crypto-backed mortgages

- Morgan Stanley prices most affordable Bitcoin ETF

- NYSE partners with Securitize on 24/7 tokenized securities platform

- Franklin Templeton teams up with Ondo on tokenized ETFs

- Invesco takes over management of Superstate’s USTB fund

Download the PDF of the full report here.

This material is provided by GSR (the “Firm”) solely for informational purposes. It is not intended to be advice or a recommendation to buy, sell or hold any investment mentioned. Investors should form their own views in relation to any proposed investment.

It is intended only for sophisticated, institutional investors and does not constitute an offer or commitment, a solicitation of an offer or commitment, or any advice or recommendation, to enter into or conclude any transaction (whether on the terms shown or otherwise), or to provide investment services in any state or country where such an offer or solicitation or provision would be illegal. The Firm is not and does not act as an advisor or fiduciary in providing this material.

This material is not an independent research report, and has not been prepared in accordance with any legal requirements by any regulator (including the FCA, FINRA or CFTC) designed to promote the independence of investment research.

This material is not independent of the Firm’s proprietary interests, which may conflict with the interests of any counterparty of the Firm. The Firm may trade investments discussed in this material for its own account, may trade contrary to the views expressed in this material, and may have positions in other related instruments. The Firm is not subject to any prohibition on dealing ahead of the dissemination of this material.

Information contained herein is based on sources considered to be reliable, but is not guaranteed to be accurate or complete. Any opinions or estimates expressed herein reflect a judgment made by the author(s) as of the date of publication, and are subject to change without notice. The Firm does not plan to update this information.

Trading and investing in digital assets involves significant risks including price volatility and illiquidity and may not be suitable for all investors. The Firm is not liable whatsoever for any direct or consequential loss arising from the use of this material. Copyright of this material belongs to GSR. Neither this material nor any copy thereof may be taken, reproduced or redistributed, directly or indirectly, without prior written permission of GSR.

Please see here for additional Regulatory Legal Notices relevant to US, UK and Singapore.🇸🇬