GSR Weekly Update - March 9th, 2026

BTC: $66,825 (+1.2%) | ETH: $1,930 (-1.7%) | BTC Dom: 56.5% | Global Cap: $2.36T

On Tuesday, Visa and Bridge, the stablecoin infrastructure platform acquired by Stripe for $1.1B in 2025, announced a major expansion of their stablecoin-linked card issuance product. Already live in 18 countries following an initial rollout focused on Latin America, the program will extend to over 100 countries across Europe, Asia Pacific, Africa, and the Middle East by year-end. On the same day, SoFi and Mastercard announced a partnership to enable SoFiUSD, SoFi's bank-issued stablecoin, as a settlement option across Mastercard's global network. Together, the two announcements underscore the rapid emergence of stablecoin-backed cards as one of the most tangible and fast-growing use cases for blockchain-based payments infrastructure.

Stablecoin cards work by connecting a user's onchain stablecoin balance to a traditional card network like Visa or Mastercard. When a cardholder makes a purchase, the card draws from their stablecoin balance, which is converted and routed through the card network to the merchant just like any other card transaction. The fundamental difference between traditional and stablecoin cards lies in the underlying settlement infrastructure. In a traditional card payment, the issuing bank authorizes the transaction and settles funds with the network, typically on a T+1 basis. With stablecoin cards, the issuing bank is effectively replaced by a stablecoin balance on a blockchain, with settlement occurring onchain through infrastructure providers like Bridge or Rain. Visa's stablecoin settlement pilot, in which Lead Bank participates alongside Bridge, is actively exploring how this onchain settlement layer can improve reconciliation, speed up fund movement, and give issuers more flexibility.

This architecture brings several notable advantages. For users, it enables the ability to hold dollar-denominated stablecoins anywhere in the world, whether for savings, yield generation, or DeFi interaction, while still spending seamlessly at any of Visa's 175 million merchant locations. For issuers and merchants, stablecoin settlement can reduce the costs and delays associated with the traditional banking infrastructure that normally sits behind card payments. Cross-border transactions, in particular, stand to benefit, as the current system often involves correspondent banking chains, multiple FX conversions, and multi-day settlement windows that add friction and cost at every step. Stablecoin-based settlement can compress much of this into near-instant, 24/7 finality.

Importantly, the growth of stablecoin cards reveals something counterintuitive about how blockchain-based payments are evolving. For years, the prevailing narrative was that blockchains would disintermediate the card networks entirely, replacing the 2-3% interchange fees with peer-to-peer crypto transactions. In practice, the opposite is happening. Card networks have an enormous, deeply entrenched moat in their global merchant acceptance and consumer trust networks. Stablecoins aren’t replacing Visa or Mastercard, but the bank settlement infrastructure behind them: the issuing banks, correspondent banks, and clearing systems that move funds between parties. The card networks, far from being disrupted, are becoming the distribution layer for stablecoin-based payments.

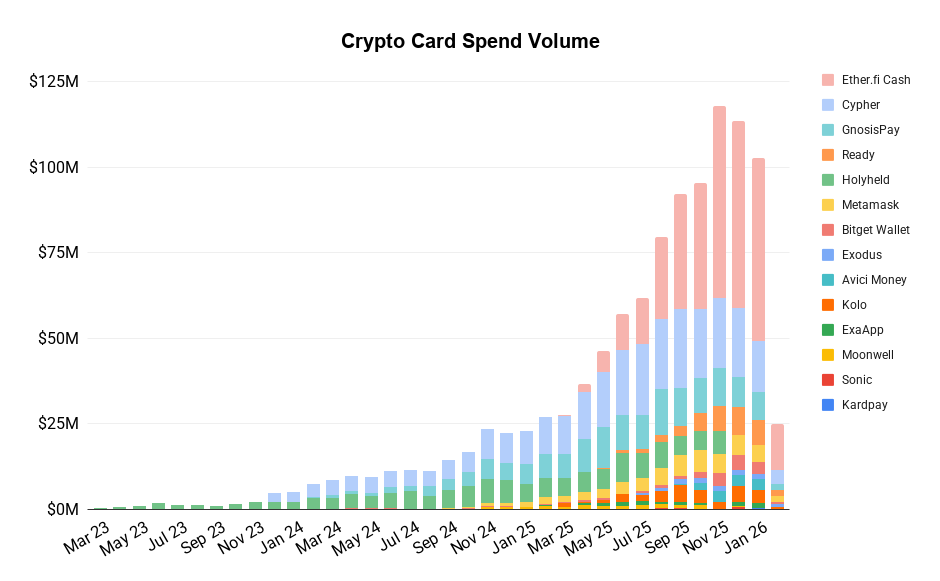

Source: Dune Analytics (@obchakevich) - Data as of Mar 8, 2026

The market is responding accordingly. Rain, a stablecoin card infrastructure provider and Visa Principal Member, raised $250M in January at a $1.95B valuation, led by ICONIQ with participation from Bessemer, Lightspeed, and Dragonfly. Rain's active card base grew 30x over the preceding year, with annualized payment volume increasing 38x to over $3B. Onchain data from Dune Analytics shows total crypto card spend volume surging from roughly $10M per month in early 2024 to over $100M per month by early 2026, with a growing number of providers entering the space. The fact that ICONIQ, a traditional growth-stage fintech investor, led Rain's round signals that this segment is increasingly viewed as a category with mainstream fintech scale potential, no longer just a crypto-native experiment.

The convergence of stablecoin rails and card networks is still in its early stages, but the trajectory is clear. As regulatory frameworks like the GENIUS Act provide greater clarity and firms like Bridge secure banking charters, the infrastructure for stablecoin-powered payments is maturing rapidly. The next frontier will likely be the acquiring side: once merchants grow comfortable receiving settlement in stablecoins, the entire bank settlement stack behind card payments could be progressively replaced by onchain infrastructure, a shift that would represent one of the most significant structural changes to global payments in decades.

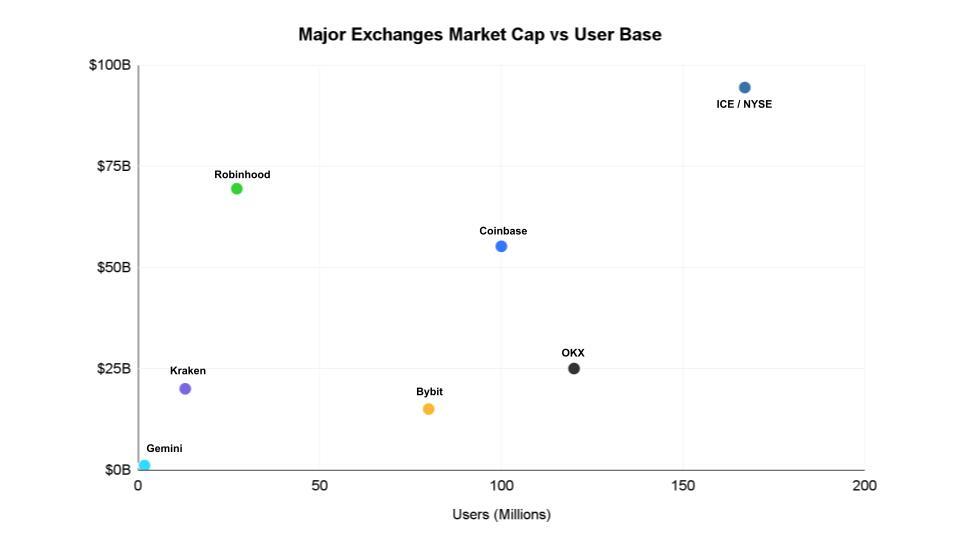

On March 5th, Intercontinental Exchange, the parent company of the New York Stock Exchange, announced an undisclosed investment in crypto exchange OKX at a $25 billion valuation. In addition to the investment, ICE will take a board seat on OKX’s Board of Directors in the hopes of furthering strategic collaboration between the two firms. According to a press release from ICE, the partnership aims to enable the two firms to build out the infrastructure necessary for institutions to engage with digital assets. The investment marks the global trading giant's fourth foray into the digital asset space. ICE notably agreed to invest up to $2 billion in Polymarket at an $8 billion pre-money valuation in October 2025, and has a minority stake in Coinbase. ICE was also one of the original founding partners behind digital asset trading platform Bakkt, which they created in collaboration with BCG, Microsoft, and Starbucks in 2018.

This partnership is a direct byproduct of OKX’s successful regulatory pivot following their $504 million settlement with the U.S. Department of Justice in February 2025. By resolving legacy AML and KYC gaps, which included paying an $84.4 million fine and forfeiting $420.3 million in fees, OKX has transitioned from a high-risk offshore entity to a U.S. regulatory compliant exchange. Now, amidst a friendlier regulatory environment, the equities and crypto trading giants will begin to integrate their products. For ICE, the board seat acts as the ultimate compliance seal of approval, providing the governance necessary to merge OKX's crypto-native rails with traditional clearing frameworks. As part of their announcement, ICE revealed their intent to license OKX spot crypto prices and launch regulated futures contracts tied to those markets. This approach will give institutions that were previously unable to invest in digital assets a compliant and trusted route to enter the space. In return, OKX will support the trading of ICE's U.S. futures and NYSE tokenized equities markets, expanding coverage to OKX’s 120 million global users.

Source: ICE Investor Relations, SEC Filings, Gallup Shareholder Data - Data as of Mar 8, 2026

Note on NYSE User Base: User count for ICE/NYSE reflects the total estimated number of U.S. individual stock market participants. Unlike retail-direct platforms, exchange users access the venue via intermediary broker-dealers.

After ICE announced their investment in OKX, commentators were quick to question why the equities platform was partnering with an offshore exchange with limited U.S. regulatory approval when there are many fully functioning pre-approved U.S. exchanges at similar or slightly higher valuations. Kraken recently raised a round at a $20 billion valuation, while Coinbase, which ICE already has a minority stake in, was trading at under $50B in public markets during the announcement. Why then, was ICE partnering with an offshore exchange with limited regulatory approval? The answer likely lies in a combination of factors that distinguish OKX from its U.S. competitors, the most important of which are global distribution, tokenization infrastructure, and strategic positioning.

The most compelling factor is distribution. ICE already dominates U.S. markets through the NYSE, but it lacks a direct channel to international retail and crypto-native traders. OKX’s 120 million global users, primarily concentrated in Asia, the Middle East, and Latin America, give ICE an immediate pipeline to distribute tokenized NYSE equities and ICE futures products to a new generation of investors that neither Coinbase nor Kraken can match internationally. For perspective, roughly 167 million Americans participate in the U.S. stock market, meaning ICE is acquiring access to a secondary, global audience that is more than two-thirds the size of its primary domestic market for a relatively low cost. Unlike Coinbase and Kraken, which remain heavily concentrated in Western regulated markets, OKX’s dominance in high-growth emerging economies gives ICE something genuinely additive rather than redundant to its existing portfolio of crypto investments.

Equally important is the tokenization and on-chain infrastructure roadmap at the heart of this deal. OKX will let its users trade tokenized stocks and derivatives listed on the New York Stock Exchange, with the feature likely launching in the latter half of 2026. Simultaneously, ICE will license OKX’s spot crypto prices to launch U.S.-regulated futures contracts. This creates a two-way bridge between traditional finance and crypto.

OKX’s success in derivatives markets may have also played a role. ICE is known for being the parent company of the NYSE, the largest spot equities market in the world, but most of their revenue actually comes from derivatives and clearing. In 2025, ICE earned $5.4 billion from their exchange services, however, equities and equity options comprised only $467 million, with the bulk of the rest coming from its global futures and options segments focused on energy, rates, and commodities. Coinbase and Kraken have spent years perfecting the retail spot experience and have only more recently started to focus on growing their derivatives footprint. In contrast, OKX was built from the ground up as a high-leverage engine, specializing in perpetual swaps and sophisticated futures products. By choosing OKX, ICE is aligning with a platform whose core competency, derivatives, mirrors its own.

Finally, there is also a strategic optionality component: OKX has previously signaled interest in pursuing a U.S. IPO, and ICE’s investment serves as an institutional endorsement ahead of such a process. If OKX were eventually to list on the NYSE, ICE would benefit not only from listing fees but also from trading activity and data licensing tied to the platform. Taken together, the deal suggests ICE chose OKX not for any single reason, but because it offered the best combination of global reach, tokenization ambition, derivatives capability, and long-term strategic upside.

Source: CoinGecko, GSR - Data as of Mar 8, 2026

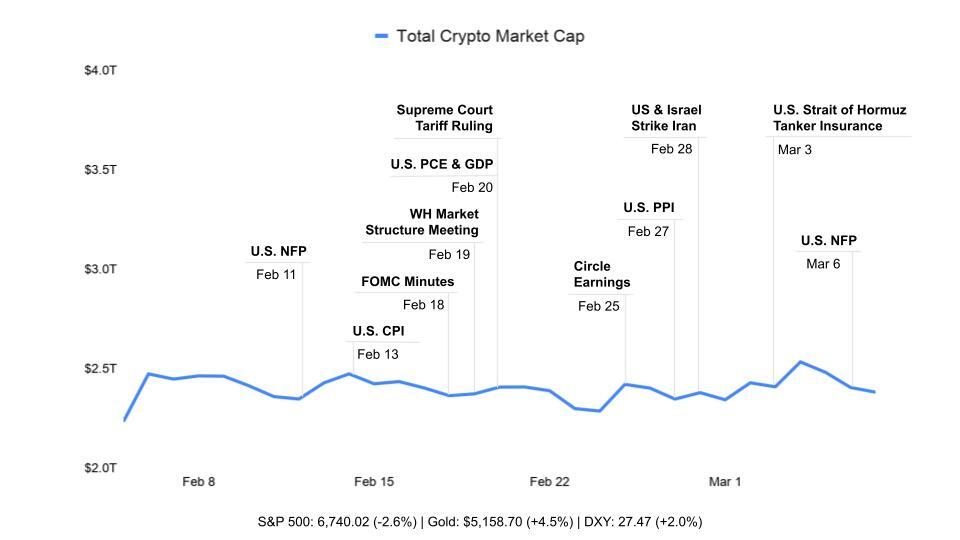

Crypto markets experienced a volatile, round-trip week dominated by shifting expectations around the U.S.-Iran war and a dismal labor market report. Total market cap opened near $2.3T, still reeling from the prior weekend's coordinated strikes on Iran, before surging above $2.5T by midweek as markets briefly priced in the possibility of a contained, short-duration conflict. That optimism evaporated in the back half of the week as the war escalated and Friday's jobs report painted a stagflationary picture, sending markets back toward $2.3T and leaving Bitcoin roughly flat on the week near $67,000.

The early-week recovery was driven primarily by signs that the economic fallout from the conflict might be managed. On Tuesday, with the war in its fourth day and equities down sharply, the S&P 500 fell as much as 2.5% intraday. President Trump announced that the U.S. would provide risk insurance and naval escorts for all maritime trade through the Strait of Hormuz, an effort to keep oil flowing and contain the energy price shock. Markets staged a dramatic intraday reversal, with the S&P 500 recovering to close down just 0.94% and oil pulling back from its highs. The rally extended into Wednesday, with the S&P 500 gaining 0.78% and the Nasdaq adding 1.29% as Goldman Sachs' David Solomon noted the ‘benign’ market reaction relative to the severity of the conflict. Bitcoin surged from the mid-$66,000s to briefly touch $74,000, its highest level in over a month. The move was amplified by a quick succession of positive crypto-native headlines, with Kraken securing Federal Reserve payment access, ICE investing in OKX at a $25B valuation, Morgan Stanley advancing in its efforts to launch a spot Bitcoin ETF, and the CFTC signaling a path for regulated perpetual futures.

The midweek optimism proved premature. On Thursday, Iran struck an oil tanker with a missile, sending crude surging past $80 per barrel and shattering the narrative that the Strait of Hormuz could be kept open without incident. The S&P 500 fell 0.56%, with the sell-off led by airlines, industrials, and other names most exposed to a global slowdown, while energy stocks surged to 52-week highs. Then on Friday, the February nonfarm payrolls report came in dramatically below expectations at -92,000 jobs versus the consensus estimate of +58,000, the worst print since the pandemic. The unemployment rate ticked up to 4.4%, while average hourly earnings held firm at +0.4% MoM, the combination of a contracting labor market and persistent wage pressure reinforcing stagflationary fears. With oil elevated and labor markets cracking, any remaining hopes for near-term Fed easing were effectively extinguished.

The week closed with further geopolitical deterioration. President Trump posted on Truth Social that areas of Iran were under consideration for ‘complete destruction’ and demanded that the country surrender, dashing any expectations for a near-term diplomatic resolution. Oil prices continued climbing, Goldman Sachs warned that crude could exceed $100 per barrel if no resolution emerges, while gold pulled back from a record intraday high of $5,419 earlier in the week. Bitcoin, having briefly touched $74,000 on Wednesday, gave back the bulk of its gains to trade near $67,500 heading into the weekend, with the broader crypto market following equities lower in a move that underscored how thoroughly macro and geopolitical forces are dominating price action in the current environment.

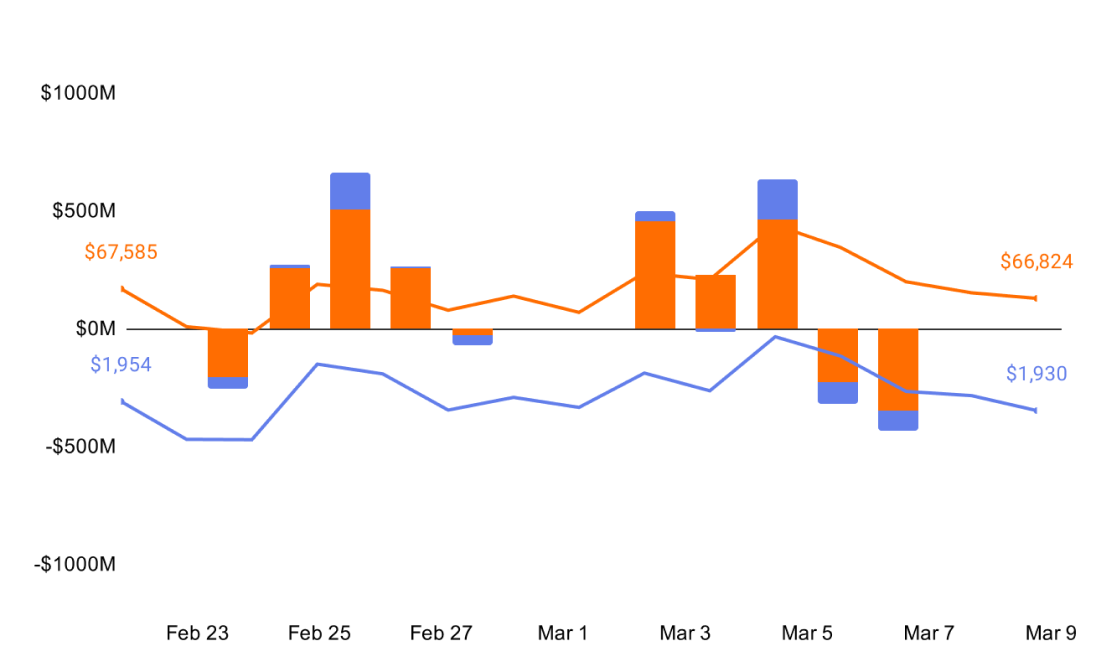

Source: Farside Investors, CoinGecko - Data as of Mar 8, 2026

ETF flows remained generally positive this week, though the momentum shifted significantly as the sessions progressed. U.S. spot Bitcoin ETFs started with a commanding lead, logging three consecutive days of heavy creations (+$458M, +$225M, and +$462M) before the tide turned late in the week. Caution ahead of the weekend led to a notable Thursday redemption (-$228M) and a sharper Friday exit (-$349M), leaving the weekly net at a healthy +$568M. U.S. spot ETH ETFs tracked a similar, albeit more muted, trajectory. The week was anchored by a standout midweek print (+$169M) that provided enough cushion to absorb modest outflows on Tuesday (-$11M) and more pronounced selling toward the close (-$91M and -$83M). Ultimately, ETH ETFs managed a net +$23M for the five-day period. Despite the net-positive flow environment, the majors struggled to translate the demand into significant price appreciation. BTC gained slightly, drifting from $65.7k to finish near $66.3k, while ETH traded flat from $1,938 to $1,930, remaining largely range-bound despite the midweek volatility.

Source: CoinGecko, GSR - Data as of Mar 8, 2026

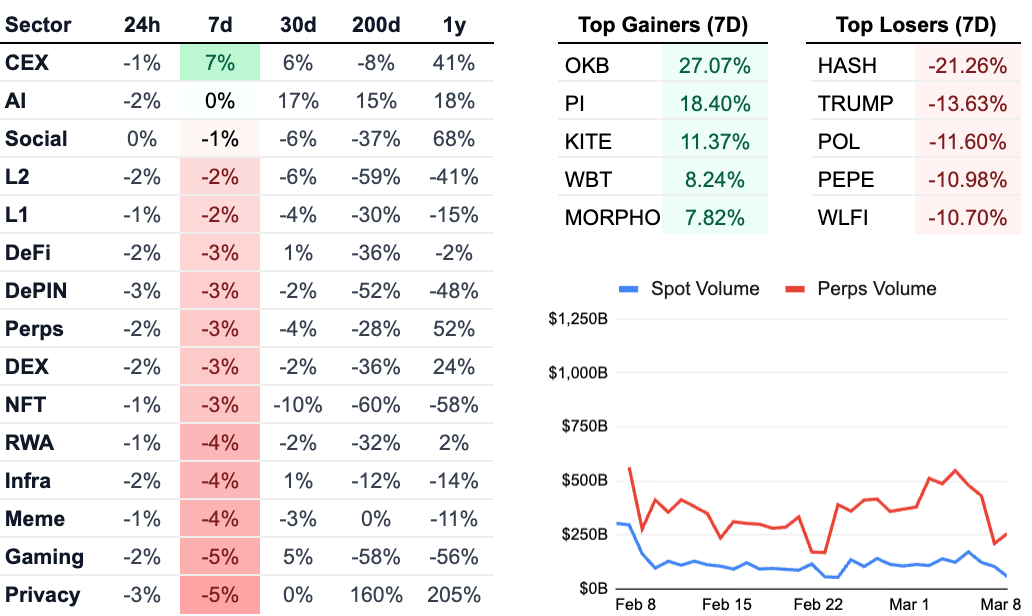

Although the majors traded flat once again, the broader market is primarily red on the week. The centralized exchange sector was the only sector with positive returns, due to a 27% increase in OKB price following the OKX and ICE partnership announcement. Morpho (+7.82%) is once again among the top gainers following the announcement of their partnership with global asset manager Apollo. Institutional announcements remain one of the few catalysts driving up token prices in the current environment. Additionally, the AI sector has quietly become the top performer on a 30-day timeline, beating out perpetuals, which was previously dominating week to week.

The privacy sector continues to underperform, once again due to losses in Zcash (-8.5%). Despite its recent performance, Zcash’s price action over the last year has allowed the privacy sector to remain the clear winner on a 200 and 365-day timeframe. The gaming sector is also down 5%, following its 33% increase the prior week. Power Protocol crashed 93% after its previous 308% increase last week.

This material is provided by GSR (the “Firm”) solely for informational purposes. It is not intended to be advice or a recommendation to buy, sell or hold any investment mentioned. Investors should form their own views in relation to any proposed investment.

It is intended only for sophisticated, institutional investors and does not constitute an offer or commitment, a solicitation of an offer or commitment, or any advice or recommendation, to enter into or conclude any transaction (whether on the terms shown or otherwise), or to provide investment services in any state or country where such an offer or solicitation or provision would be illegal. The Firm is not and does not act as an advisor or fiduciary in providing this material.

This material is not an independent research report, and has not been prepared in accordance with any legal requirements by any regulator (including the FCA, FINRA or CFTC) designed to promote the independence of investment research.

This material is not independent of the Firm’s proprietary interests, which may conflict with the interests of any counterparty of the Firm. The Firm may trade investments discussed in this material for its own account, may trade contrary to the views expressed in this material, and may have positions in other related instruments. The Firm is not subject to any prohibition on dealing ahead of the dissemination of this material.

Information contained herein is based on sources considered to be reliable, but is not guaranteed to be accurate or complete. Any opinions or estimates expressed herein reflect a judgment made by the author(s) as of the date of publication, and are subject to change without notice. The Firm does not plan to update this information.

Trading and investing in digital assets involves significant risks including price volatility and illiquidity and may not be suitable for all investors. The Firm is not liable whatsoever for any direct or consequential loss arising from the use of this material. Copyright of this material belongs to GSR. Neither this material nor any copy thereof may be taken, reproduced or redistributed, directly or indirectly, without prior written permission of GSR.

Please see here for additional Regulatory Legal Notices relevant to US, UK and Singapore.