GSR Weekly Update - May 11th, 2026

S&P 500: 7,398.93 (+11.8%) | Gold: $4,730.70 (+1.0%) | DXY: 97.84 (-1.3%)

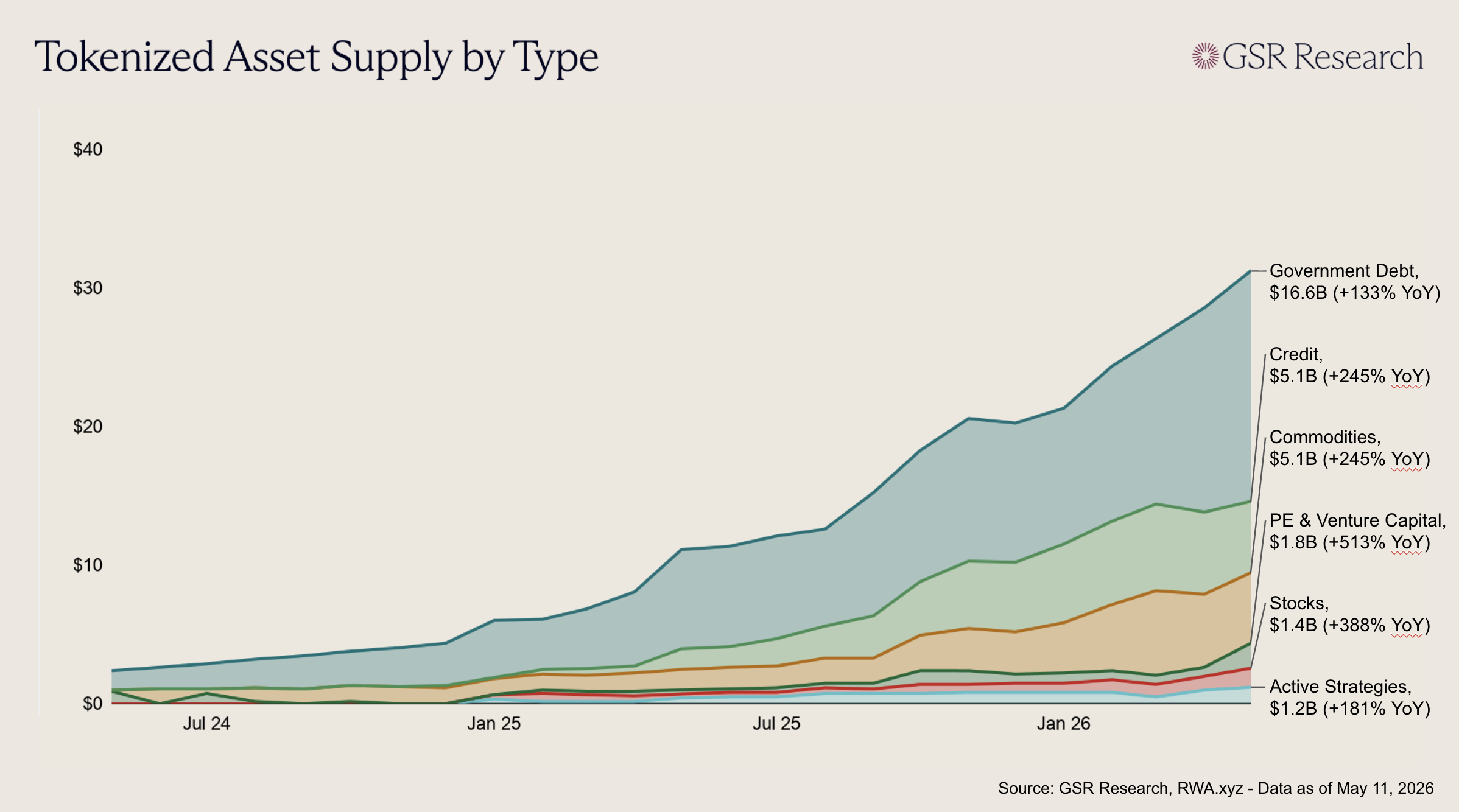

Tokenization has been a popular subject in crypto for years, often with more headline-grabbing announcements than actual progress to show. However, the last few weeks have featured a number of notable moves. Bullish announced a $4.2 billion acquisition of transfer agent Equiniti, DTCC laid out a July go-live for the limited launch of its tokenization service, Coinbase made a strategic investment in Centrifuge and tapped it as its preferred tokenization partner on Base, and Securitize announced a partnership with Jupiter to launch fully onchain, regulated trading for tokenized equities on Solana. Taken together, these developments highlight how the tokenization stack is moving out of its proof-of-concept phase and into real market infrastructure.

A key trend in the development of the tokenization stack is the merging of traditional financial plumbing with public blockchains. Tokenized assets will only reach parity with their offchain counterparts once the legal, custody, and record-keeping rails behind them also move onchain. Until that happens, RWA tokens will continue to be little more than IOUs sitting on top of actual share registers, with the friction and fragility that implies.

In this regard, DTCC’s efforts are among the most consequential, given the company’s central role in US securities settlement. Its July pilot and broader October launch will allow firms to issue digital versions of assets already held in custody at DTC, with the same ownership rights and protections preserved. More than 50 firms, including BlackRock, Goldman Sachs, JPMorgan, Circle, and Anchorage, are providing feedback and collaborating to shape the service.

Bullish and Securitize are also making strides. Bullish’s acquisition of Equiniti folds a regulated transfer agent serving nearly 3,000 issuer clients and 20 million shareholders into a crypto-native platform. Securitize and Computershare’s partnership from the prior week seeks the same outcome. Computershare, which serves close to 60% of the S&P 500, will act as transfer agent for Securitize’s Issuer-Sponsored Tokens, enabling public companies to issue tokenized equity that represents direct ownership rather than a wrapped derivative. All of these efforts help unlock the benefits of tokenization for thousands of existing securities currently limited to traditional rails.

Last week’s announcements pose another question: what can tokenized assets actually do onchain? With crypto issuance and record-keeping working toward compliant solutions, the focus shifts from removing barriers to defining utility. A possible answer to this question: plugging them into the same composability and liquidity primitives that give crypto-native products distinctive utility.

Coinbase’s deal with Centrifuge is about bringing tokenized equity ETFs, fixed-income funds, and other assets onto Base, where they can plug into the broader DeFi stack of lending markets, perps collateral, rates markets, vaults, and structured product infrastructure. Tokenized assets that can be borrowed against, used as margin, or composed into new strategies are more useful than those that sit in a wallet.

Securitize and Jupiter’s partnership is aimed at addressing the liquidity requirements of tokenization. PropAMMs have been quietly beating centralized exchange execution across crypto pairs on Solana. This partnership aims to extend propAMM infrastructure to tokenized US equities, with Jupiter routing flow to propAMMs and Securitize handling the regulated broker-dealer, ATS, and transfer agent layers underneath. The bet is that the market structure innovations that delivered tight onchain spreads in crypto will translate to equities, and that execution on public blockchains can eventually rival centralized venues.

Compliance and utility in the tokenization space go hand in hand. Plugging tokenized equities into DeFi or propAMM liquidity only really matters if those tokens carry the same legal weight as their offchain counterparts, which is exactly what the transfer agent and depository moves aim to deliver. Overall, last week’s announcements make a fairly persuasive case that tokenization is finally graduating from theory to utilized market infrastructure.

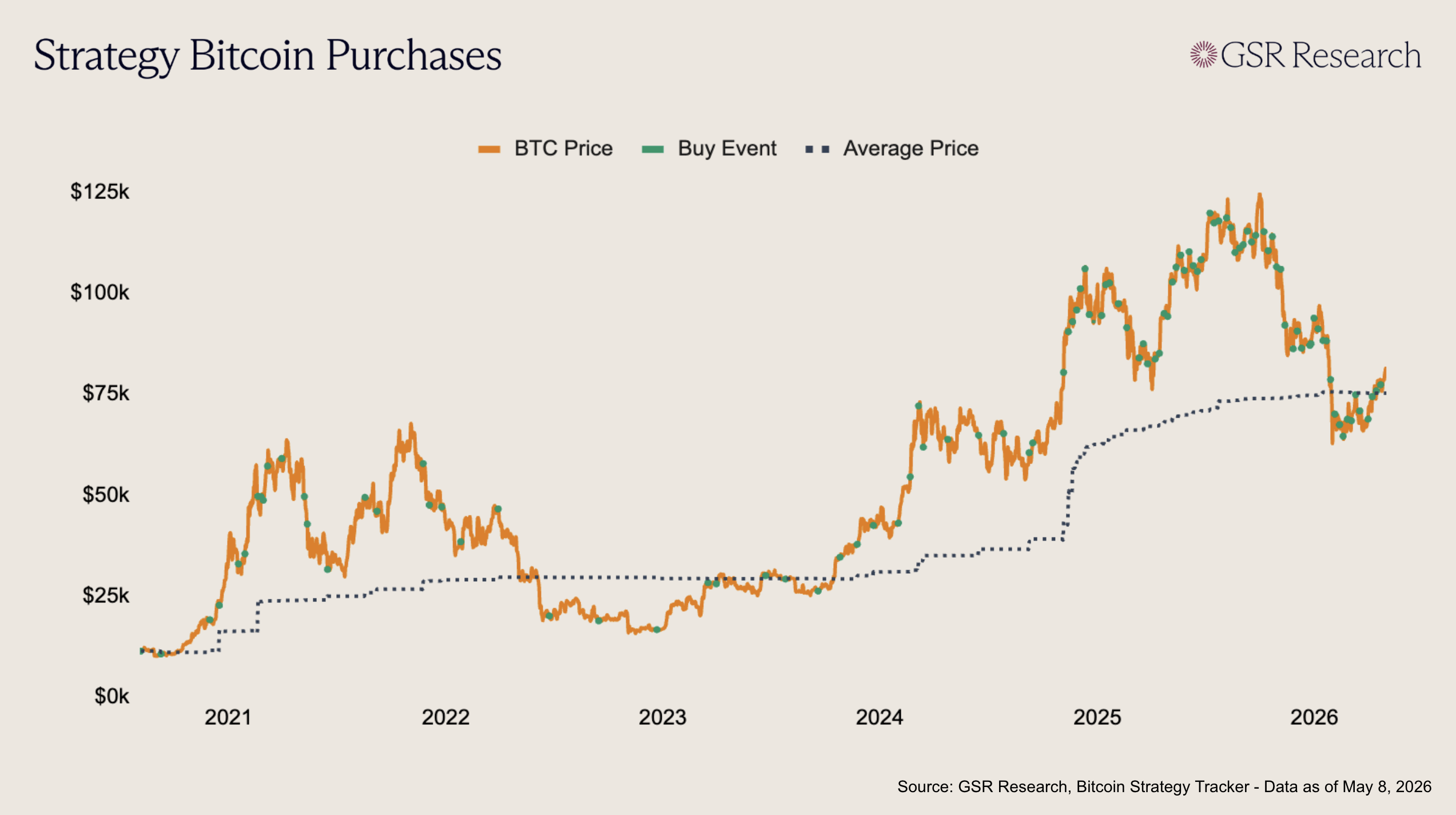

For years, Strategy has operated as the market’s most outspoken Bitcoin accumulator, buying regardless of price, timing, or sentiment. Michael Saylor’s purchases have unfailingly drawn the industry’s attention, serving as both bullish and bearish signals, a constant topic of debate, and a steady reminder of the company’s singular Bitcoin strategy. Now, despite Bitcoin’s recent strength, investors are being forced to consider something previously unthinkable: a Strategy Bitcoin sale.

Last week, Strategy executives opened the door to selling Bitcoin under certain conditions, an action Saylor spent years telling the market his company would never take. On the company’s first-quarter earnings call CEO Phong Le clarified that the company would sell bitcoin to fund dividends, repurchase convertible debt, or replenish its dollar reserve, as long as the trade improves the company’s Bitcoin per share ratio. Saylor himself said that “We will probably sell some bitcoin to pay a dividend just to inoculate the market and send the message that we did it.” His messaging is a clear break from his earlier dogma; in February he insisted that Strategy would not sell even if Bitcoin fell to $8,000.

Although Bitcoin’s price action has been favorable as of late, Strategy’s broader financial backdrop explains the shift in his sentiment. The company posted a $12.5B Q1 net loss on a $14.5B unrealized digital asset loss, generated $124.3M in revenue, and ended March with $2.2B in cash. At the same time it raised $5.6B through STRC year to date, paid $692.5M in cumulative preferred dividends, and faces roughly $1.49B in annual dividend obligations with only 18 months of USD coverage. While the accounting losses are non-cash, the preferred dividends are not and have come due, forcing Saylor to renege his public promise.

Prior to the announcement, Strategy’s flywheel was simple: issue common stock, preferred stock, or convertible debt, use the proceeds to buy Bitcoin, let the treasury appreciate, and never touch the Bitcoin pile itself. This strategy worked as external capital remained cheap and available, yet each new funding layer made the never sell constraint harder to sustain by adding obligations that had to be serviced in cash.

On the earnings call, Le outlined Strategy’s new playbook: issue MSTR when it trades at a sufficiently high mNAV, sell STRC to build its USD reserve or buy back debt, and crucially, sell bitcoin when it is more accretive to Bitcoin per share than raising fresh capital. He even quantified the shift, saying that with Strategy’s current capital stack, the breakeven sits around 1.22x mNAV. Below that level, it is more accretive for Strategy to sell bitcoin and pay dividends than to issue common stock and buy more BTC.

The bear case is that Strategy’s new flywheel inverts into a Bitcoin liquidation engine. In a prolonged bear market obligations would remain fixed, equity issuance could become punitive, preferred financing would dry up, and BTC sales might become the only way to repay debt. While it seems unlikely that Saylor would sell any meaningful portion of Strategy’s Bitcoin stack, the mere possibility could spook the market, given the company now controls roughly 1 in every 25 Bitcoin that will ever exist.

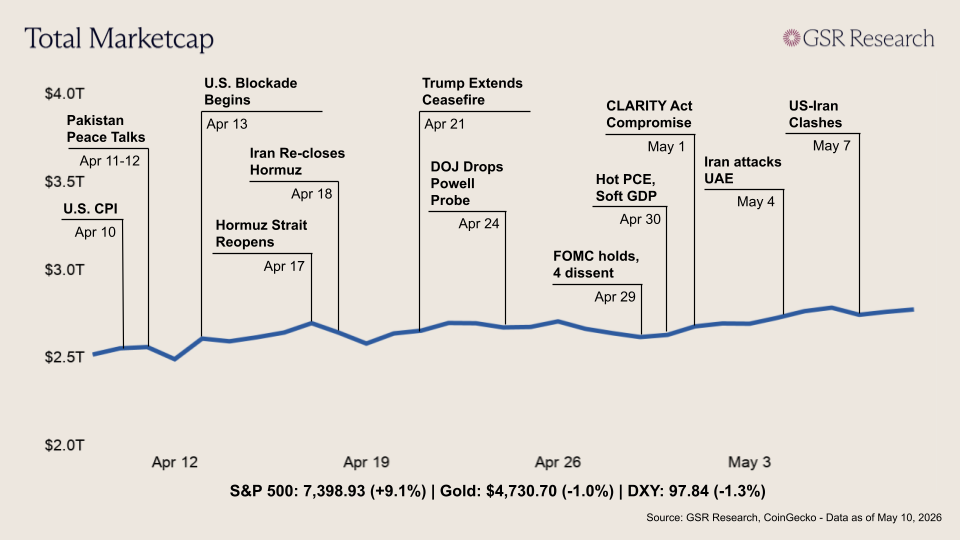

Crypto markets pushed higher through a turbulent week shaped by a fragile US-Iran ceasefire that nearly unraveled midweek and economic data releases that reinforced a stagflationary macro backdrop. Risk assets largely shrugged both off. The S&P 500 logged its sixth straight winning week, while BTC ended the week up roughly 5% near $82,000 after a round trip between $77,400 and $82,800, with total crypto market cap near $2.8T as oil retraced and AI earnings further buoyed equities.

US economic data painted a mixed picture with labor markets exhibiting unexpected strength, but consumer sentiment nonetheless weakening further. Friday's April nonfarm payrolls came in at +115K against a +62K consensus, with the unemployment rate holding at 4.3%. However, wage growth has now slowed to 3.6% YoY as oil feeds through to headline prices. The University of Michigan's preliminary May sentiment reading fell to 48.2, a second consecutive record low going back to 1952, with one-third of respondents citing gas prices and roughly 30% citing tariffs.

Geopolitics continues being the main macro driver. Brent opened near $115 after Iran fired missiles at the UAE over the weekend, then reversed as Defense Secretary Hegseth reaffirmed the ceasefire on Tuesday and ran US ships through the Strait of Hormuz under destroyer escort. The calm broke Thursday, when US officials said Iranian forces attacked three US destroyers in the strait, prompting strikes from US forces. Iran struck the UAE again Friday, but Brent still finished the week lower near $101 as markets bet on a Pakistan-mediated diplomatic exit. The biggest crypto-specific catalyst came as the week closed, when the Senate Banking Committee scheduled the CLARITY Act markup for Thursday, May 14, the first forward step after months of delay.

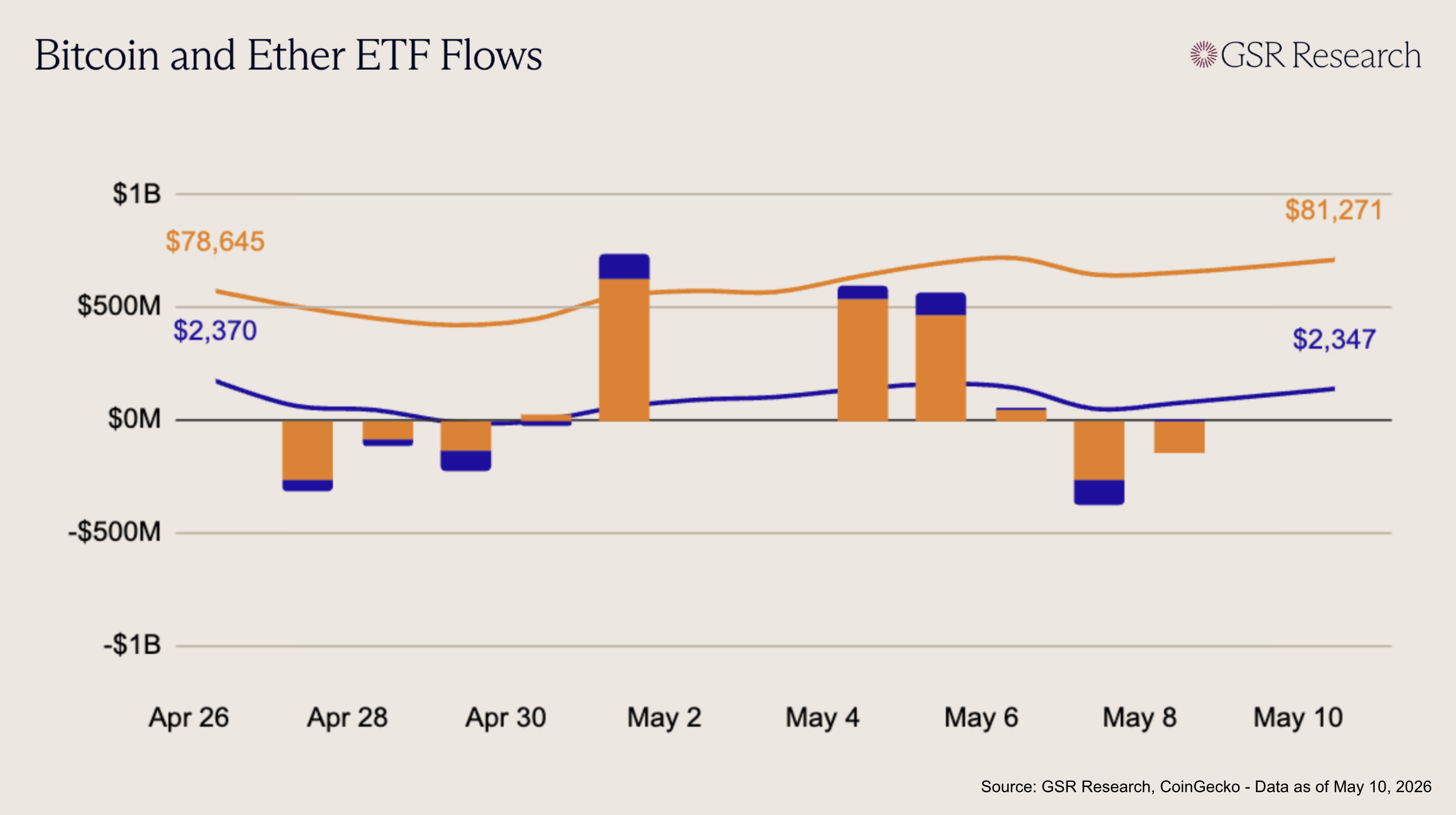

U.S. spot Bitcoin ETFs saw a strong start to the week, with three consecutive days of inflows (+$532M on May 4, +$467M on May 5, and +$46M on May 6) reflecting strong demand across major issuers. Flows flipped decisively negative on May 7 and May 8 (-$269M and -$146M), indicating a coordinated pullback in positioning rather than isolated rotation. The speed of the shift highlights how quickly allocators moved from accumulation to de-risking after the early-week surge. Overall, the flow profile points to a reactive market structure, where strong inflow momentum struggled to sustain and was met with aggressive profit-taking.

Ether ETFs followed a similar but more fragile trajectory. The week opened with consistent inflows (+$61M on May 4, +$98M on May 5, and +$12M on May 6), signaling improving participation after the prior volatility. However, this strength faded quickly as flows turned sharply negative on May 7 (-$104M), before stabilizing modestly into May 8 (+$4M). Compared to BTC, the reversal was more abrupt relative to the prior inflow base, reinforcing the pattern of less durable demand. The overall flow dynamic continues to reflect a more tentative stance toward ETH, with participation remaining more sensitive to short-term shifts in sentiment.

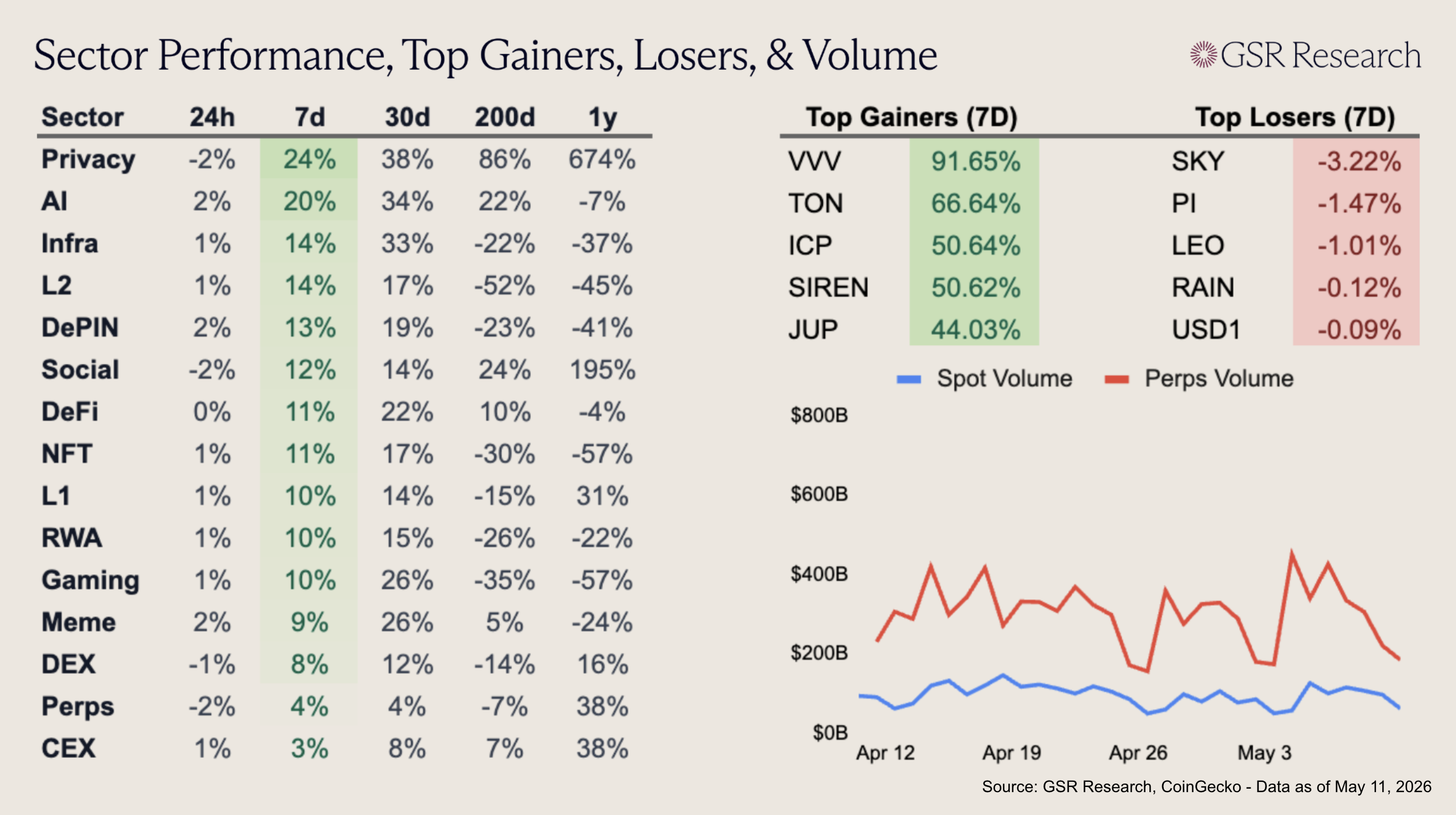

It has been a fruitful week for altcoins, with all sectors posting positive returns over the past 7 days. Privacy is the category leader, up 24% due to gains in Zcash (+39.7%) and Monero (+5.8%). As of today, privacy is the top performer on the 7d, 30d, 200d, and 1 year timeframes, and by a wide margin. The AI sector also outperformed, up 20% on the week due to gains in Venice (+91.65%) and ICP (+50.64%).

TON rallied (+66.64%) after founder Pavel Durov announced that Telegram would succeed the TON Foundation as the network’s main driving force while also becoming the chain’s largest validator. JUP also gained (+44.03%) following the announcement of a three-way partnership between Jupiter, Securitize, and Jump Trading Group that will see the exchange launch fully onchain, regulated trading for tokenized equities on Solana.

This material is provided by GSR (the “Firm”) solely for informational purposes. It is not intended to be advice or a recommendation to buy, sell or hold any investment mentioned. Investors should form their own views in relation to any proposed investment.

It is intended only for sophisticated, institutional investors and does not constitute an offer or commitment, a solicitation of an offer or commitment, or any advice or recommendation, to enter into or conclude any transaction (whether on the terms shown or otherwise), or to provide investment services in any state or country where such an offer or solicitation or provision would be illegal. The Firm is not and does not act as an advisor or fiduciary in providing this material.

This material is not an independent research report, and has not been prepared in accordance with any legal requirements by any regulator (including the FCA, FINRA or CFTC) designed to promote the independence of investment research.

This material is not independent of the Firm’s proprietary interests, which may conflict with the interests of any counterparty of the Firm. The Firm may trade investments discussed in this material for its own account, may trade contrary to the views expressed in this material, and may have positions in other related instruments. The Firm is not subject to any prohibition on dealing ahead of the dissemination of this material.

Information contained herein is based on sources considered to be reliable, but is not guaranteed to be accurate or complete. Any opinions or estimates expressed herein reflect a judgment made by the author(s) as of the date of publication, and are subject to change without notice. The Firm does not plan to update this information.

Trading and investing in digital assets involves significant risks including price volatility and illiquidity and may not be suitable for all investors. The Firm is not liable whatsoever for any direct or consequential loss arising from the use of this material. Copyright of this material belongs to GSR. Neither this material nor any copy thereof may be taken, reproduced or redistributed, directly or indirectly, without prior written permission of GSR.

Please see here for additional Regulatory Legal Notices relevant to US, UK and Singapore.