GSR Weekly Update - May 4th, 2026

S&P 500: 7,230.12 (+10.7%) | Gold: $4,644.50 (-0.7%) | DXY: 27.41 (-1.3%)

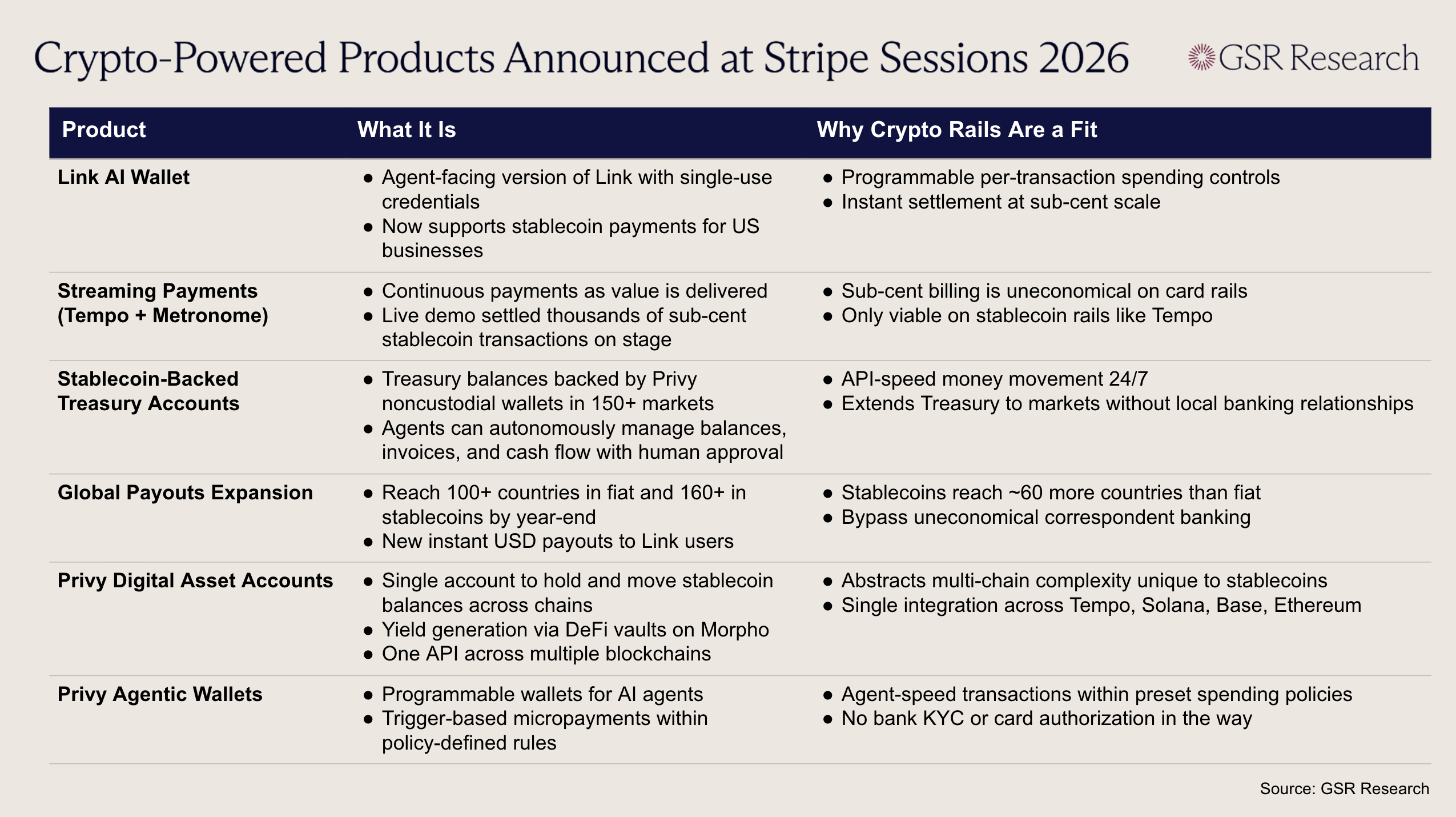

On April 29th, Stripe held its annual Sessions conference, unveiling 288 new products and features to roughly 9,000 builders and business leaders. The framing this year was unmistakable: Stripe is, in CEO Patrick Collison's words, "building economic infrastructure for AI." Most headlines focused on the agentic commerce announcements, including a new Link AI wallet, the Issuing for agents virtual card primitive, and an Agentic Commerce Suite built with Meta and Google. What got less attention is how thoroughly stablecoins and blockchain rails have been threaded through nearly every layer of Stripe's emerging AI stack.

Although agentic commerce is still in its infancy and remains somewhat speculative, Stripe made it clear that it’s making an aggressive bet on it. Collison stated plainly that "agents will be responsible for most transactions in the not overly distant future," and pointed out that AI agent traffic to Stripe's docs grew from under 5% to nearly 40% across 2025. The launches reflect a company preparing for a world where software transacts, and they expect much of that flow to settle in stablecoins. US businesses can now accept stablecoins through Link, while Bridge will power stablecoin payouts in 160+ countries by year-end versus 100+ on fiat rails, and Privy's programmable wallets will sit underneath Treasury balances in over 150 markets. In a particularly notable moment, Stripe and Metronome demoed live "streaming payments" on Tempo, settling thousands of sub-cent stablecoin transactions on stage.

Stablecoins are a natural fit for agentic payments as AI agents simply do not behave like the SaaS users that traditional payment infrastructure was built around. They burst, consume APIs unpredictably, and often only need a service for a few seconds before going quiet. Monthly subscription don't fit this pattern, and neither do enterprise data contracts with minimum commitments or reserved GPU capacity.

The natural model for an agent is pay-per-use: per API call, per inference, per article, per record pulled from a dataset, per second of compute. Traditional rails make this uneconomical, as per-transaction fees in the tens of cents erase the margin on anything priced below a dollar. Stablecoins on modern blockchains, by contrast, can settle for fractions of a penny, which is what makes pay-per-API-call and pay-per-token pricing viable in the first place.

Once that pricing floor drops, new commerce patterns become possible: agents buying articles or datasets per item rather than per subscription, AI inference billed and immediately paid per token without settlement risk, compute provisioned per second rather than per instance, and continuous micropayment streams alongside real-time data feeds. Most consequentially, the model unlocks direct agent-to-agent payments, where one specialized agent pays another with no human or shared billing account in the middle. Additional unlocks like programmable escrow, instant 24/7 settlement, and global reach without banking hours further make stablecoins the most natural fit for cases where the customer is an autonomous piece of software.

One of the most noteworthy aspects of Stripe’s efforts is how aggressively they’re treating stablecoins less as a crypto category and more as invisible settlement infrastructure underneath its stack. Henri Stern, who runs Privy inside Stripe, put it directly on stage: the work is "not about crypto, for crypto's sake," but about building better experiences for customers and their money. Users see dollars in their Link wallet, merchants see balances in their Stripe dashboard, and the blockchain sits quietly behind it as a faster, cheaper, programmable rail. For an industry that has spent years debating institutional adoption, Sessions 2026 showed that plenty of the workflows envisioned for the future of payments are already being built on blockchain rails, even if most end users will never see them.

Last week Pump.fun burned every PUMP token it had repurchased over the prior nine months, eliminating a stash worth roughly $370M that represented 36% of its circulating supply. Since launch, Pump.fun has been routing all net revenue into systematic buybacks, turning the platform’s consistently high cash flow into automatic demand for PUMP. However, going forward, only 50% of net revenue will fund buybacks and burns, while the other 50% will be retained for operations and development. While the burn is the major headline, the larger story is Pump.fun moving away from pure buybacks in favor of reinvesting in the protocol.

The reaction to Pump.fun’s decision has been mixed. Existing holders understandably like the burn, especially given how much cash the platform was willing to devote to supporting its token. However, there is also a vocal user base that was disappointed that the tokens were burned instead of redistributed to active users. Traders argued that if the $370M in PUMP tokens had been redistributed to the most active and influential users instead of burned, the resulting influx of attention around the large airdrop would have led to greater interest in the protocol and its token. Users were also quick to point out that only half of the protocol’s revenue will be used for buybacks going forward, while it had previously been 100%.

However, Pump.fun’s pivot is directionally aligned with what several commentators and venture investors have been arguing for some time contra the token buyback zeitgeist: projects should not spend all of their revenue on token buybacks, and instead should reinvest in product, distribution, and ecosystem growth. Pump’s decision to retain half their revenue looks less like a betrayal of users and more like an admission that growth requires retained earnings.

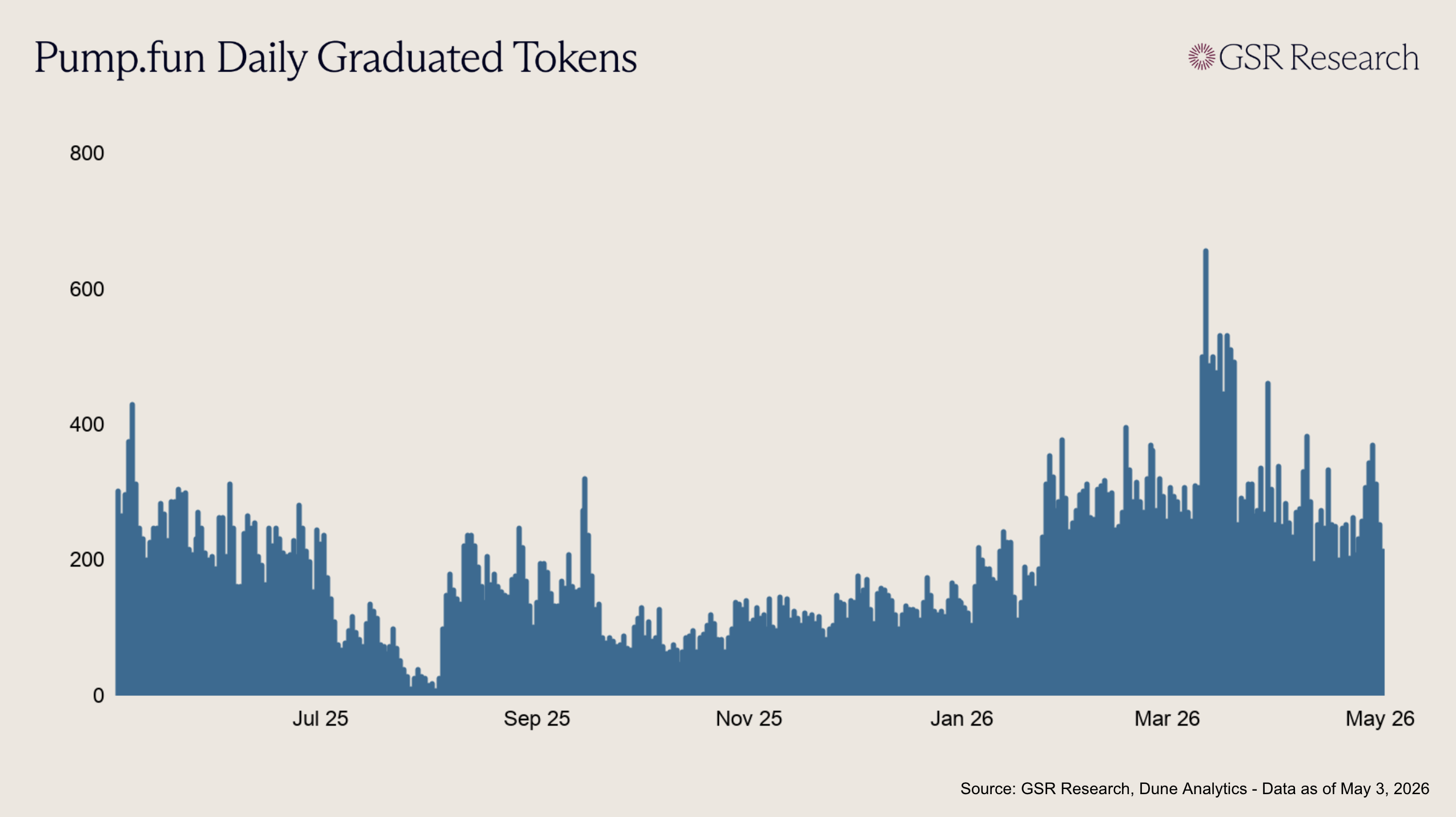

Despite the widespread narrative that memecoins have cooled, Pump.fun graduations have actually been rising. After bottoming in late summer 2025, daily graduations began rebuilding through the fall, stepped materially higher in early 2026, and briefly spiked above 600 in March before settling back into a much higher range than the second half of last year.

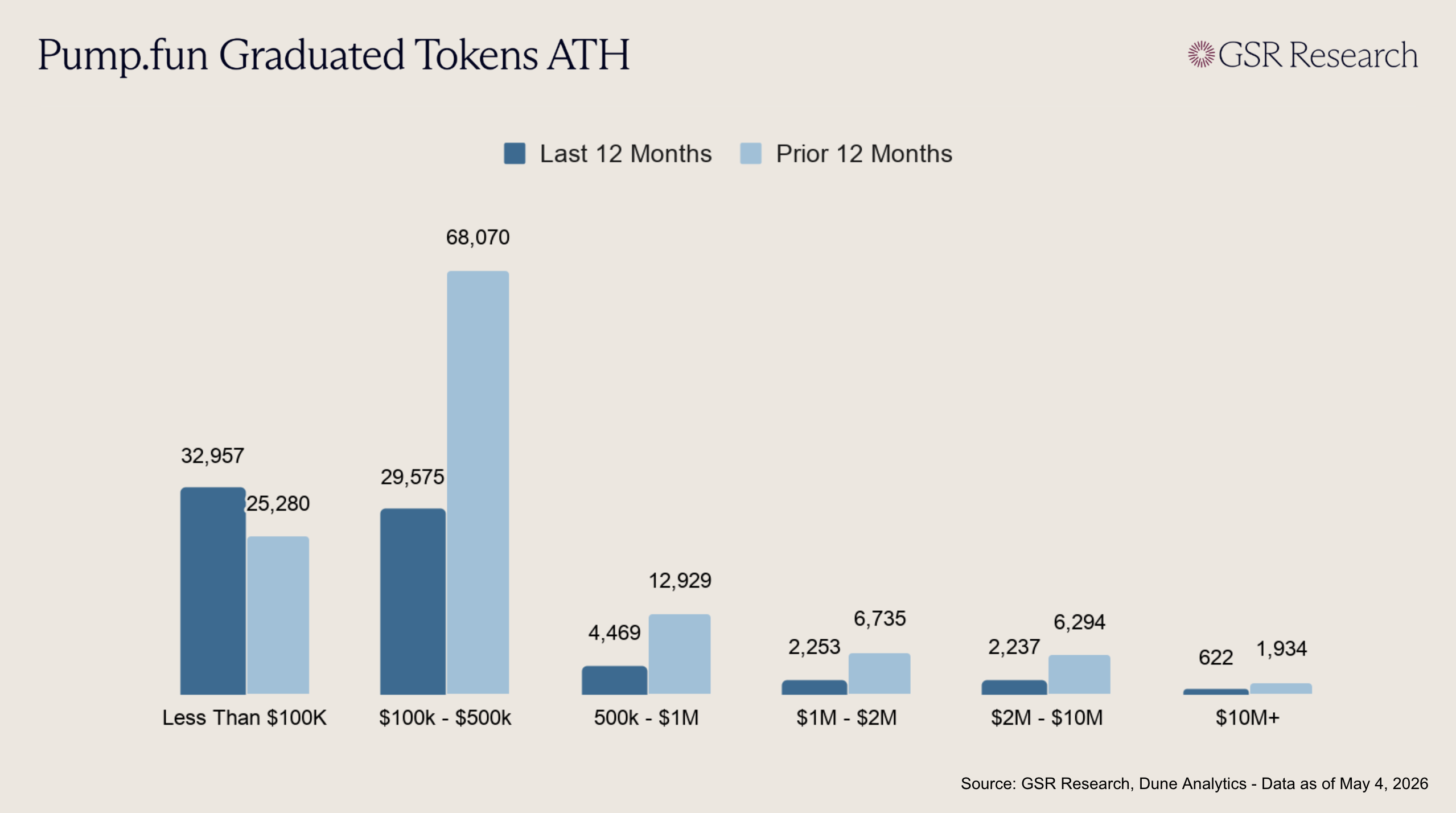

Despite the increase in graduations, recent Pump.fun launches lack the cultural impact they were once defined by. Of the more than 70,000 tokens that have graduated from the launchpad in the last year, only 622 have reached an all-time high of $10M or greater. The vast majority of graduated tokens top below the $500k level due to the increasing “PvP” aspect of memecoin trading. Liquidity is fragmented, attention is thinner, and secondary trading has become far more zero-sum.

However, Pump.fun has not suffered as a result of this. The protocol’s revenue is not determined by the number of cultural icons like PNUT that top at hundreds of millions of dollars, but rather from the daily churn of graduating tokens that generate consistent fees. This has allowed Pump.fun to maintain hundreds of thousands in daily revenue despite falling out of the attention sphere. While PvP traders ensure that almost every token fails to reach a defensible marketcap, they also give devs a reason to continue deploying fresh tokens every day. The memecoin factory is still running, but the market it feeds has changed.

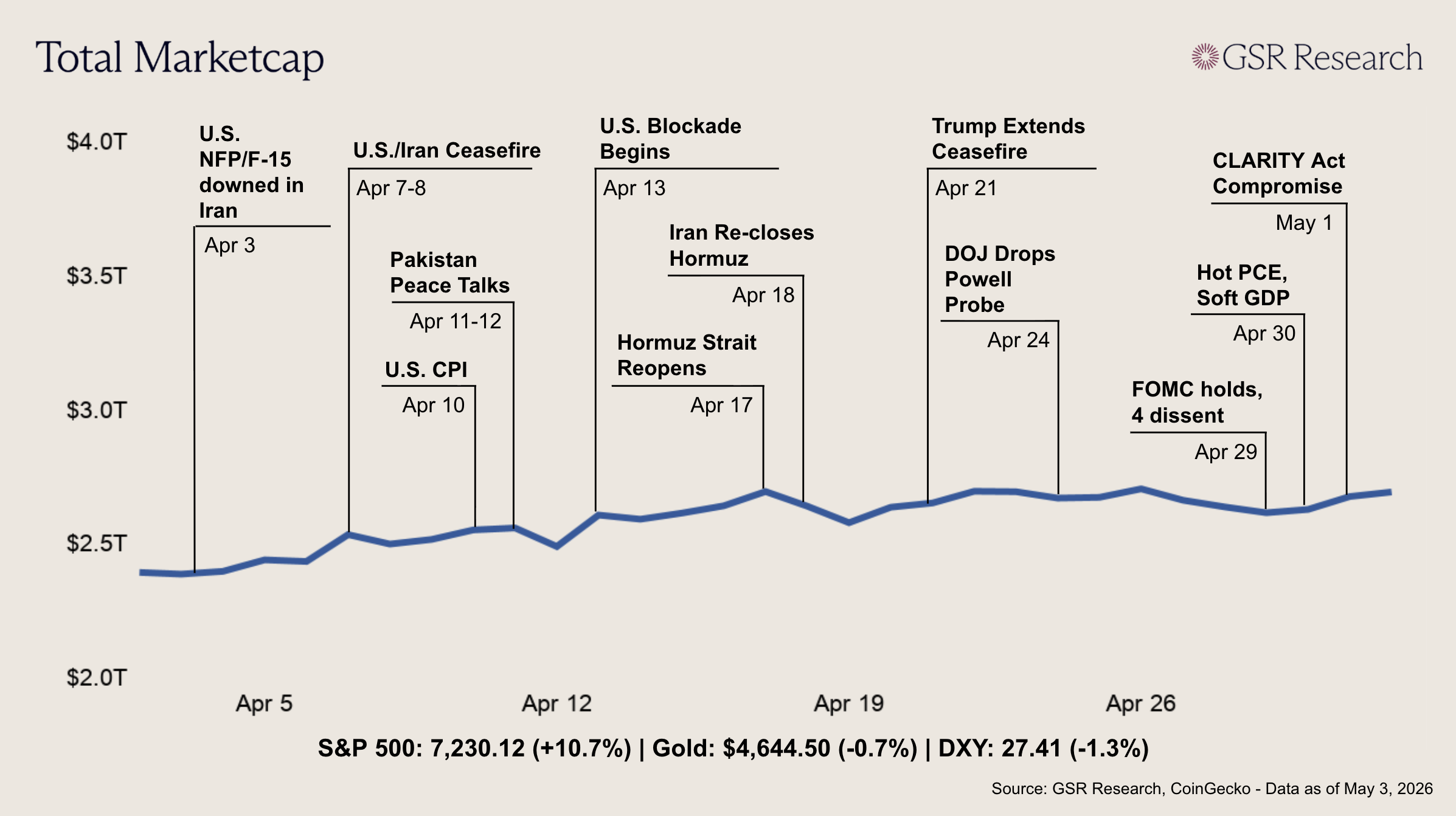

Crypto markets navigated two competing forces over the past week: a stagflationary US backdrop that left the Fed openly split on policy, and a late-week run of strong earnings, tentative Iran diplomacy, and crypto-specific legislative progress that brought risk appetite back. BTC ended the week roughly flat near $78,000 after a round trip between $74,900 and $79,500, with total crypto market cap ending the week near $2.7T.

The stagflation theme came through clearly in the data, with both growth and inflation readings tied to the ongoing Iran conflict. Q1 GDP came in at 2.0% against 2.3% consensus, while March headline PCE accelerated to 3.5% YoY, the highest since spring 2023, driven by energy costs. The April ISM Manufacturing prices index hit 84.6, its highest reading since 2022. Wednesday's FOMC decision exposed the resulting policy tension: the Committee held at 3.5-3.75% in an 8-4 vote, the most dissents since October 1992, with Governor Miran preferring a cut and three regional presidents pushing back on the statement's easing bias. In his final press conference as chair, Powell announced he would stay on the Board of Governors past his May 15 term expiry, the first chair to do so since 1948, complicating the handover to Kevin Warsh.

The offsetting catalysts landed in quick succession on Friday. Apple's earnings beat and upbeat guidance pushed the S&P 500 and Nasdaq to record closes, capping the best month for both indices since 2020. Brent fell to $108 after Iran sent an updated peace proposal through Pakistani mediators, though Trump rejected the offer over the weekend. The most direct crypto catalyst came Friday evening, when Senators Tillis and Alsobrooks released compromise text on the CLARITY Act's stablecoin yield provision, removing the bill's biggest remaining obstacle. Polymarket's 2026 passage odds jumped to 70% on the news. Focus now turns to Friday's April payrolls and the state of US-Iran talks.

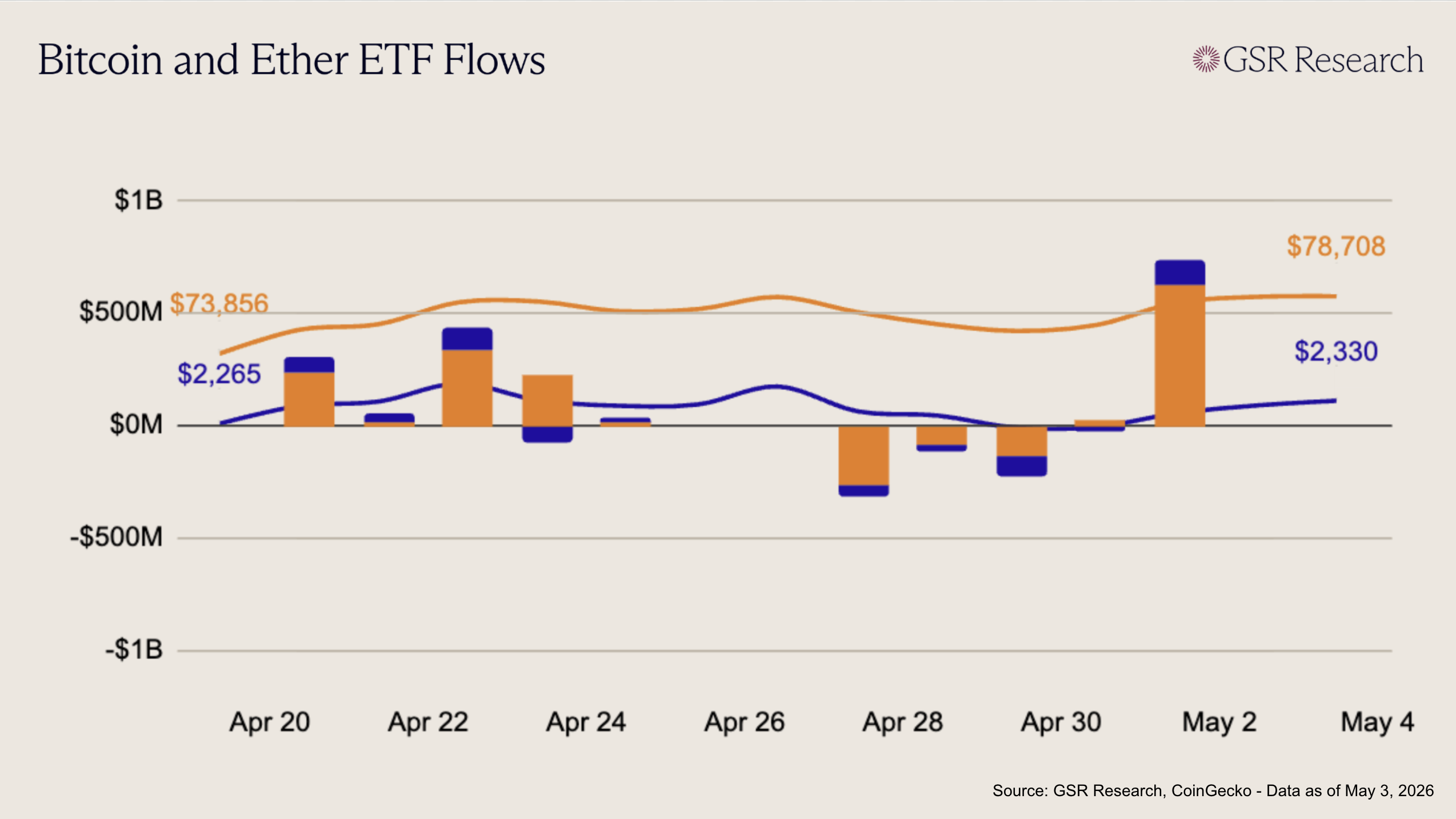

U.S. spot Bitcoin ETFs saw a clear shift toward risk-off positioning early in the week, with consistent and accelerating outflows across most sessions. After a modestly positive close the prior Friday (+$14M), flows turned decisively negative on the 27th, with three consecutive days of heavy redemptions (-$263M, -$90M, and -$138M). The pressure eased slightly into Apr 30 (+$24M), but the rebound was not sustained. A sharp reversal into May 1 (+$630M) capped the week, marking one of the largest single-day inflows in recent periods and suggesting rapid re-engagement after the brief liquidation phase.

Ether ETFs exhibited a more consistently negative trend throughout the week, with limited evidence of sustained demand. Following a small inflow on Apr 24 (+$23M), flows turned and remained negative across Apr 27 to Apr 30 (-$50M, -$22M, -$88M, and -$24M), indicating persistent selling pressure. Unlike BTC, there was no meaningful stabilization phase midweek, and outflows were spread across multiple issuers rather than concentrated in a single product. While May 1 saw a recovery (+$101M), the magnitude was notably smaller relative to BTC and came after a more prolonged drawdown. The overall pattern continues to highlight weaker institutional conviction in ETH, with flows more consistently skewed toward outflows and less responsive to short-term shifts in sentiment.

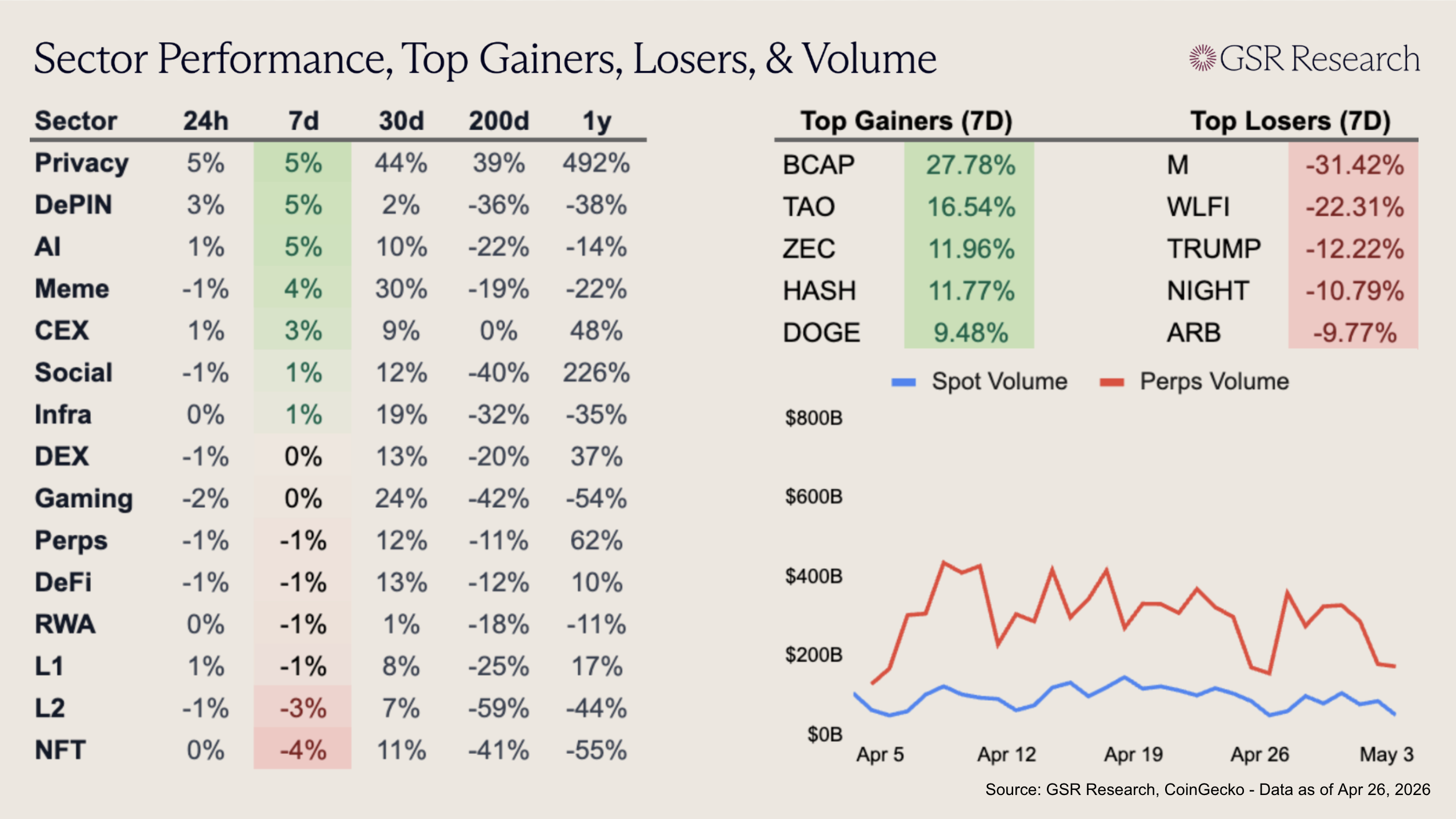

Privacy is the top-performing sector this week, due to a midweek Zcash rally (+11.96%). The privacy-focused layer-one continues to be one of the most volatile assets in the top 100 by market cap, outperforming again this week following its recent Robinhood listing. Bittensor (+16.54%) also rallied this week, with the network stabilizing following the departure of major subnet operator Covenant AI last month.

WLFI (-22.31%) and TRUMP (-12.22%) both fell sharply as a result of Tron CEO and Founder Justin Sun suing World Liberty Financial in California federal court. Justin Sun claimed that the Trump-backed institution wrongfully froze about 540 million unlocked WLFI tokens, blocked governance rights, and threatened to burn his holdings after he resisted pressure to invest more. As of today, WLFI hit back, filing a defamation suit alleging that Sun made false claims about backdoors and governance and harmed a major deal.

Download the PDF of the full report here.

This material is provided by GSR (the “Firm”) solely for informational purposes. It is not intended to be advice or a recommendation to buy, sell or hold any investment mentioned. Investors should form their own views in relation to any proposed investment.

It is intended only for sophisticated, institutional investors and does not constitute an offer or commitment, a solicitation of an offer or commitment, or any advice or recommendation, to enter into or conclude any transaction (whether on the terms shown or otherwise), or to provide investment services in any state or country where such an offer or solicitation or provision would be illegal. The Firm is not and does not act as an advisor or fiduciary in providing this material.

This material is not an independent research report, and has not been prepared in accordance with any legal requirements by any regulator (including the FCA, FINRA or CFTC) designed to promote the independence of investment research.

This material is not independent of the Firm’s proprietary interests, which may conflict with the interests of any counterparty of the Firm. The Firm may trade investments discussed in this material for its own account, may trade contrary to the views expressed in this material, and may have positions in other related instruments. The Firm is not subject to any prohibition on dealing ahead of the dissemination of this material.

Information contained herein is based on sources considered to be reliable, but is not guaranteed to be accurate or complete. Any opinions or estimates expressed herein reflect a judgment made by the author(s) as of the date of publication, and are subject to change without notice. The Firm does not plan to update this information.

Trading and investing in digital assets involves significant risks including price volatility and illiquidity and may not be suitable for all investors. The Firm is not liable whatsoever for any direct or consequential loss arising from the use of this material. Copyright of this material belongs to GSR. Neither this material nor any copy thereof may be taken, reproduced or redistributed, directly or indirectly, without prior written permission of GSR.

Please see here for additional Regulatory Legal Notices relevant to US, UK and Singapore.