The following article was written by GSR's research team for Finery Market's Stablecoins 2035 (Special Report).

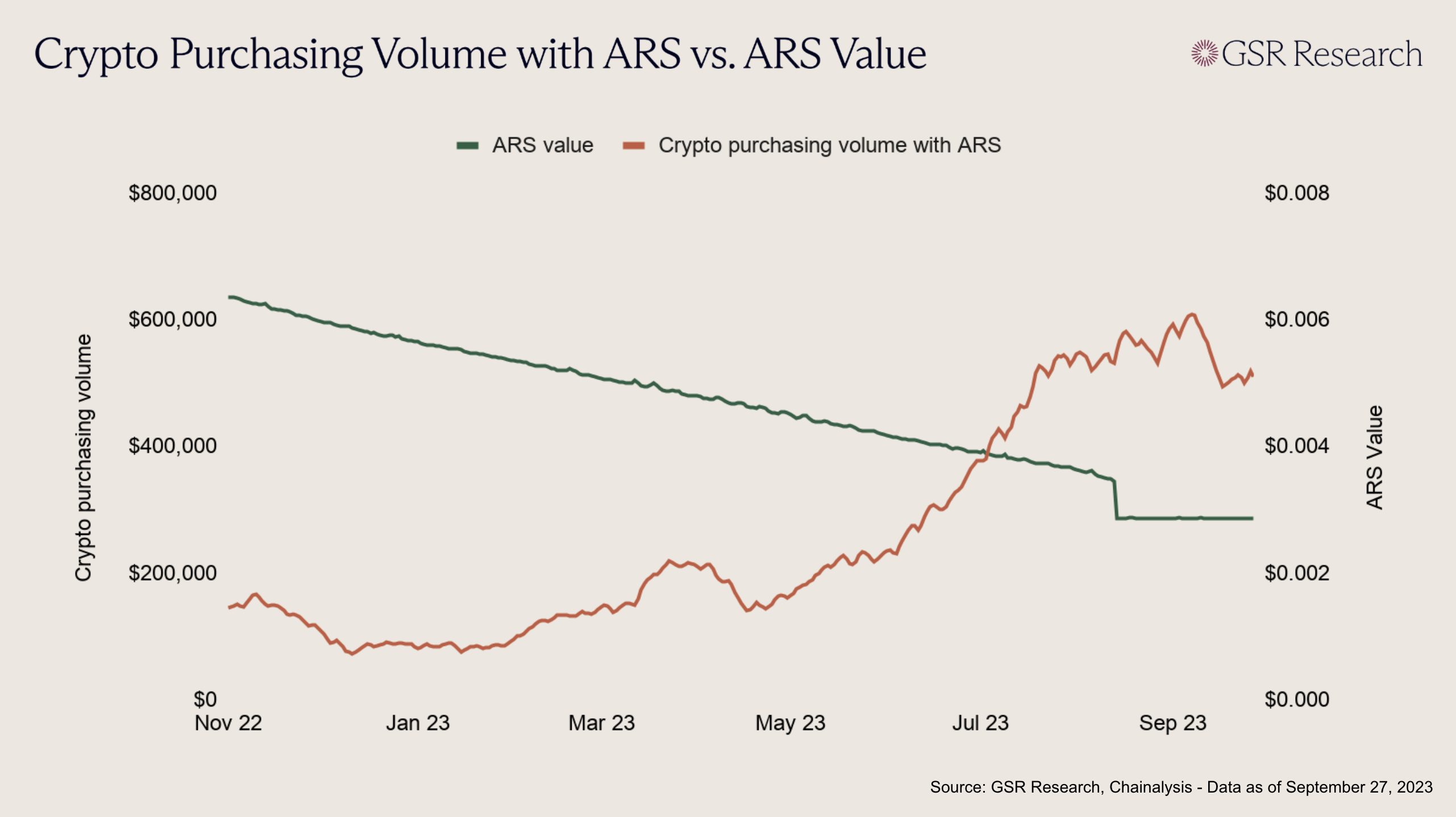

U.S. dollar stablecoins are perhaps crypto’s most striking growth story. Total supply now sits north of $300 billion, and the sector’s growth has decoupled from crypto markets’ speculative boom and bust cycles. Dollar stablecoins have found real, enduring product-market fit. Notably, a large portion of their adoption has been driven by emerging markets. By Goldman Sachs’ estimate, roughly two-thirds of stablecoin supply is held in emerging markets. In Argentina, for example, stablecoins are around 62% of all crypto activity. For many, dollar stablecoins are a way to protect their savings from a local currency they can't rely on. A recent survey across five emerging economies found that 47% of users turn to them mainly to save in USD. In 2023, Chainalysis noted a suggestive correlation between rising crypto purchasing volume in Argentina around the time the country’s inflation crossed 100% inflation for the first time in three decades, amid an otherwise quiet period for crypto markets. The usefulness of dollar stablecoins for providing stability in unstable economies is clear, however, as we look ahead to 2035, this savings use case points to a deeper shift than just the dollarization of emerging market economies that appears on the surface.

When someone in Buenos Aires or Caracas moves savings into a dollar stablecoin, they are effectively buying properties their own financial system cannot provide: a stable store of value, money that is hard to inflate away or freeze, and a link to the global economy. The dollar is simply the most liquid instrument that bundles these properties, so it is where demand has flowed first. It is the first clear instance of a broader capability, and we think that capability is what will reshape emerging-market finance over the coming decade.

That broader capability is the ability to hold, move, hedge, borrow against, and earn on almost any asset from anywhere, at a cost that keeps falling. It’s a capability that blockchains have unlocked by making the movement of value permissionless, global, and increasingly frictionless. For example, thanks to blockchains, a saver outside the U.S. can hold tokenized U.S. Treasuries and other fixed-income instruments and collect a yield that would be almost impossible to access via a local bank account. They can hold tokenized equities and funds to get exposure to global growth, which has historically been challenging in regions with limited brokerage and banking access. They can use a wide range of assets as collateral to secure access to credit onchain, unlocking potential for formerly inaccessible capital efficiency. And they can trade derivatives, enabling them to hedge risk, use leverage, and access structured payoffs in ways that similarly were previously reserved for sophisticated investors. In sum, blockchains are unlocking the capabilities to build portfolios of customized exposures tailored to each individual or business’ unique situation, substantially expanding their ability to grow their capital and reach their goals.

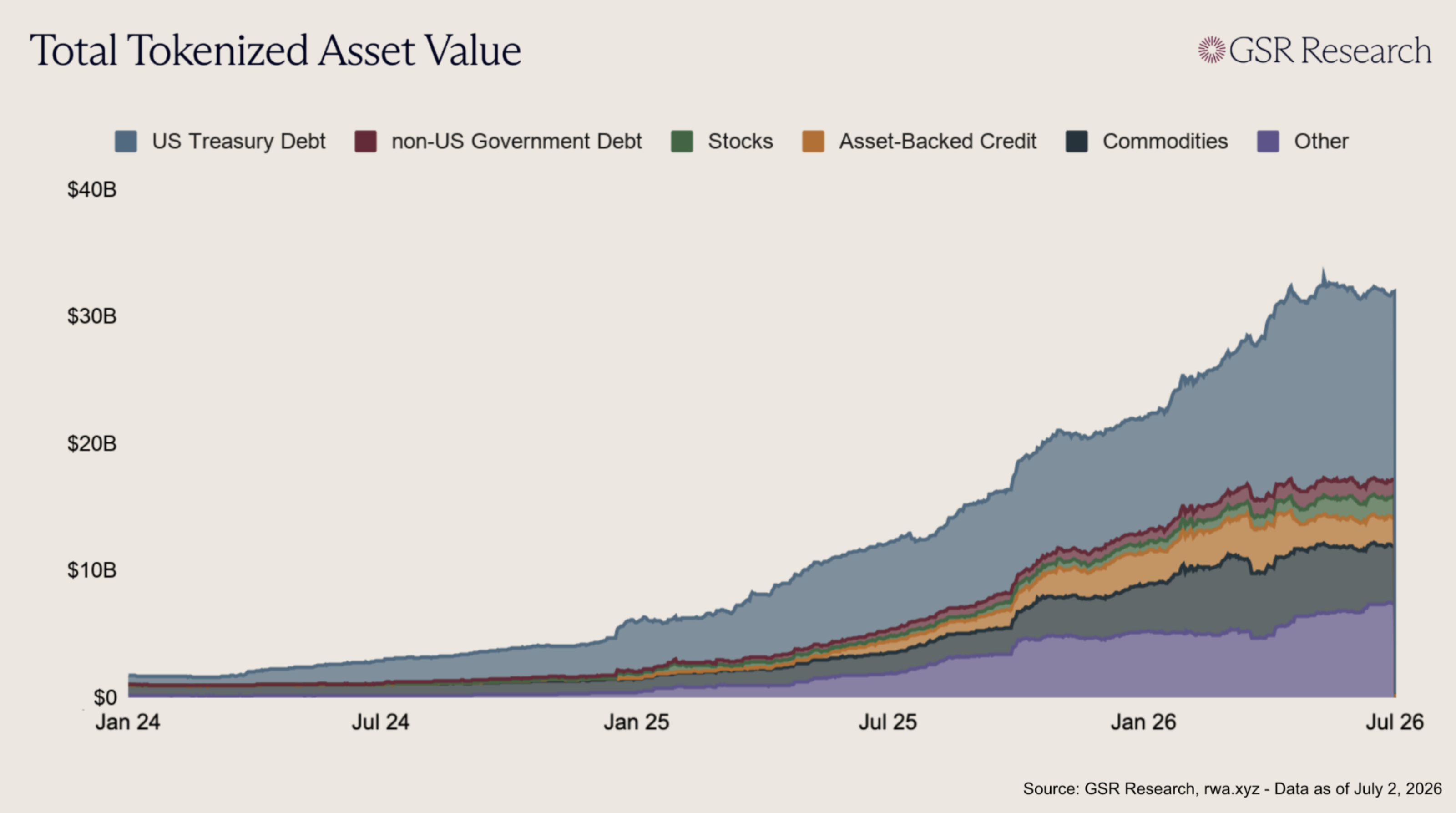

The final form of this capability is still far off, but we’re starting to see its shape. Stablecoins led the way by providing a global avenue for dollar savings, with their supply growing into the hundreds of billions as a result. Tokenized U.S. Treasuries are following suit as holders of onchain capital seek yield. Though still dwarfed by stablecoins, their supply eclipsed $15 billion this year, growing roughly 150% in the span of twelve months. Tokenized equities are further behind, but growing even faster. According to rwa.xyz, total tokenized stock supply now sits around $1.5 billion, up around 400% from $300 million around June of last year. This pattern extends to commodities, private credit, corporate credit and beyond as more and more assets come onchain. The onchain infrastructure to custody, trade, and manage assets has largely been built, the piece that’s still missing is onboarding the supply of tokenized assets that users will want to hold and trade.

Allowing ourselves to speculate a bit, we think one of the most consequential developments of the coming decade will be the convergence of this onchain capability with artificial intelligence. The infrastructure blockchains provide is powerful, but infrastructure alone is not enough. Building a portfolio of customized exposures, knowing when to rebalance, how to hedge a currency, which assets to pledge as collateral and on what terms, has historically required the intelligence and knowhow of advisors and wealth managers, services that are effectively out of reach for most savers in emerging markets. Just as blockchains collapse the cost of moving and holding value, AI will collapse the cost of financial intelligence. A saver in Lagos or Ankara will be able to describe their situation and goals in plain language and have an AI agent construct, monitor, and adjust a portfolio on their behalf, executing across tokenized treasuries, equities, credit, and derivatives onchain. The division of labor is a natural one, with AI supplying the judgment that currently rests with human advisors and blockchains providing the underlying rails. Together they will offer something that has never existed at scale: private-banking-grade financial management available to anyone with a smartphone.

For this vision to work, however, one more piece of infrastructure is essential, and that is liquidity. A tokenized asset that cannot be traded at a fair price on demand is little more than a wrapper. The portfolios we describe only function if users can rebalance positions as their circumstances change, liquidate holdings in moments of need, trade derivatives to hedge risk and access leverage, and borrow against collateral without fear that a liquidation will cascade through a thin order book. That requires deep, continuous, two-sided markets, not just in stablecoins and major assets but across the growing long tail of tokenized treasuries, equities, funds, and whatever comes onchain next. However, liquidity of that breadth does not appear on its own. It is furnished by professional liquidity providers and market makers willing to quote prices around the clock, warehouse risk across venues, and connect onchain markets with the traditional markets where the underlying assets trade. As the supply of tokenized assets grows, the firms doing this work will be as fundamental to the system as the blockchains themselves, serving as a key part of the plumbing of frictionless finance in 2035.

Stepping back, the current story of stablecoins is best understood as the opening chapter of a much larger one. Savers in emerging markets adopted stablecoins because they were the first instruments to deliver properties their local financial systems could not. We expect that same demand to pull in each new asset class as it arrives onchain. By 2035, we think the remarkable thing about someone in Lagos or Buenos Aires holding a globally diversified, intelligently managed, deeply liquid portfolio will be that it is not remarkable at all. Stablecoins showed that hundreds of millions of people will reach for better financial infrastructure the moment it is offered to them. The industry’s task over the next decade will be to finish building it, onboarding the assets, deepening the liquidity, and layering on the intelligence, so that the reinvention of emerging-market finance, already well underway, can run its course.