GSR Weekly Update - June 22nd, 2026

BTC: $64,028 (+0.0%) | ETH: $1,723 (+3.6%) | BTC Dom: 56.2% | Global Cap: $2.28T

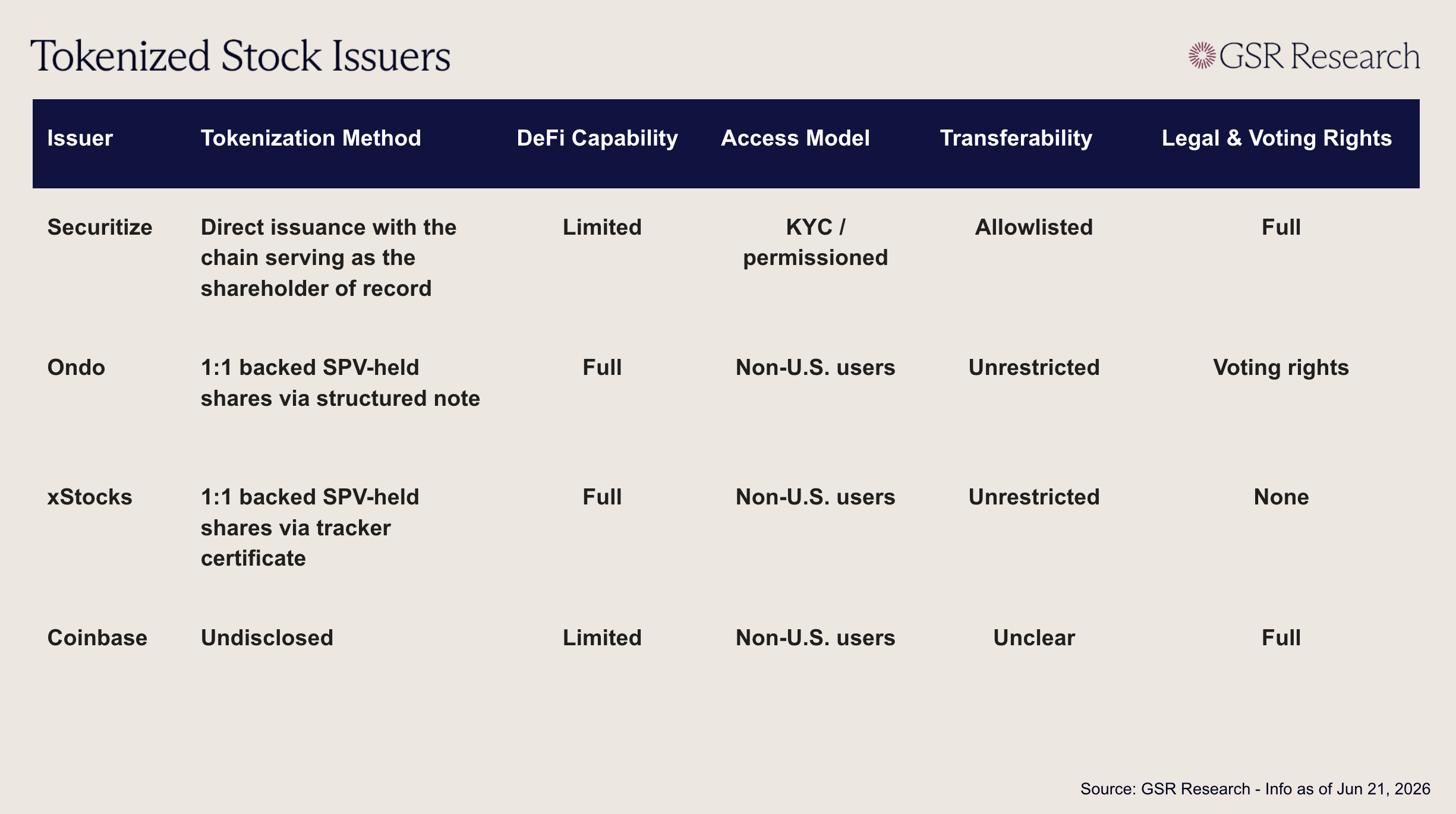

On June 16th, Coinbase announced that it would be introducing tokenized stocks for non-U.S. customers next month, marking one of the exchange’s most direct moves yet into traditional brokerage territory. Coinbase said the products will be backed 1:1 by the underlying assets and represent true equity ownership, including dividend payouts and shareholder rights, while also allowing users to trade stocks 24/7, lend shares for yield, use them as collateral, or transfer them as easily as standard onchain assets. The announcement came as part of a broader “Everything Exchange” product push that also included Coinbase Advisor, an AI-powered SEC-registered investment advisor, agentic trading, expanded prediction-market contracts, stock and crypto options, RWA perpetual futures, pre-IPO perps, and a redesigned Coinbase Advanced interface that will eventually unify Coinbase’s U.S. exchange, international derivatives venues, and Deribit liquidity.

Notably, Coinbase is not treating tokenized stocks as a side experiment, but as a large piece of a broader attempt to collapse crypto, equities, derivatives, advice, lending, and payments into a single financial interface. This means that the legal structure they use to pursue that goal is unusually important. Coinbase is claiming direct equity ownership rather than synthetic exposure, while also maintaining that the tokens will be easily transferable and viable within lending and borrowing, yet the company has not yet published full legal documentation on how the tokens will be held, transferred, voted, redeemed, or integrated into DeFi. Given the legal verbiage the product may use a third-party wrapper model (similar to those utilized by xStocks and Ondo), but it is unclear how the tokenized assets will maintain their legal and voting rights. There has been some speculation as to how Coinbase will structure their product to achieve this, but until those details are public, it’s difficult to say whether their model will truly break new ground compared to what others already offer.

The tokenized equity market is often described as one category, but the underlying structures differ meaningfully. xStocks, issued by Backed (and owned by Kraken), sits at the most crypto-native end of the spectrum, as they are freely transferable and composable within DeFi as standard ERC-20 and SPL tokens. Each xStock is fully collateralized by the underlying asset, but legally it is a bearer debt instrument classified as a tracker certificate, not direct equity ownership. Holders receive economic exposure to the stock, but no shareholder voting rights. This structure has helped xStocks become highly portable and DeFi-compatible, but it sacrifices direct issuer rights in exchange for broad transferability and onchain composability.

Ondo Global Markets, the largest platform by distributed value, is also built around economic exposure rather than direct share registration, though its structure is more institutional than xStocks. Ondo’s tokenized stocks are structured notes issued by a BVI SPV, fully backed by the corresponding underlying securities and cash in transit, with tokenholders receiving a first-priority security interest. The tokens are also broadly transferable, with any non-sanctioned wallet able to hold them and standard DeFi integrations available permissionlessly. Ondo designs the products as total-return trackers, meaning dividends are reflected through reinvested economics rather than a simple one-token, one-share model over time. Voting rights are provided through Broadridge, allowing holders to express proportional voting preferences rather than directly vote registered shares.

Securitize represents a different path entirely. Rather than issuing tracker products around equities, Securitize is building tokenization infrastructure closer to the issuer and transfer-agent layer. Its partnership with Computershare allows U.S.-listed companies to issue tokenized equity securities alongside traditional shares, with Computershare acting as transfer agent and processing corporate actions for tokenized holdings. Securitize has also been named NYSE’s first digital transfer agent eligible to mint blockchain-native securities for corporate and ETF issuers on the NYSE’s planned Digital Trading Platform. This model is more permissioned and less naturally DeFi-composable, but it is also closer to the official share register and more likely to preserve traditional corporate rights.

Coinbase’s proposed model appears to be closer to a transfer agent’s direction in ambition, since it is explicitly promising true equity ownership, dividends, and shareholder rights, rather than merely tracker exposure. However, Coinbase’s advantage is not issuer infrastructure, but distribution. If the company can give global users 24/7 access to real U.S. equities inside the same app where they already hold crypto, stablecoins, perps, and eventually AI-managed portfolios, it could become one of the most important consumer distribution channels for tokenized stocks.

On June 11th, the SEC proposed rescinding Regulation NMS Rules 611 and 610(e), which currently underpin trade-through protections and restrictions on locked or crossed markets in U.S. equities. Rule 611 effectively requires trading centers to avoid executing at prices worse than protected quotes elsewhere, tying U.S. equity execution to the national best bid and offer. The structure makes sense for legacy order-book venues, but it sits awkwardly with AMMs and other onchain systems that price assets through pool curves rather than routing against the NBBO.

Benchmark called the proposal the most consequential U.S. crypto rule of the year, arguing that removing these NMS constraints could eliminate one of the largest barriers to tokenized equities trading on AMMs, with Securitize, Coinbase, and Galaxy among the likely beneficiaries. This wouldn’t mean tokenized stocks become suddenly cleared for fully open U.S. DeFi trading, as questions around broker-dealer registration, custody, settlement, corporate actions, and transfer restrictions remain unresolved. However, the direction is notable: the SEC is no longer just evaluating tokenized equities as a crypto product, but reconsidering whether the existing equity market structure itself is too rigid for blockchain-based trading.

Tokenized stocks are moving from experiment to competitive requirement. xStocks is proving the open wrapper model, Ondo is building structured-note exposure with institutional controls, Securitize is moving tokenization into issuer and transfer-agent infrastructure, and Coinbase is now trying to bring true equity ownership into a mass-market crypto app. The category is still early and fragmented, but the end state is increasingly clear: equities are widely becoming programmable, transferable, and available outside the constraints of the traditional trading day.

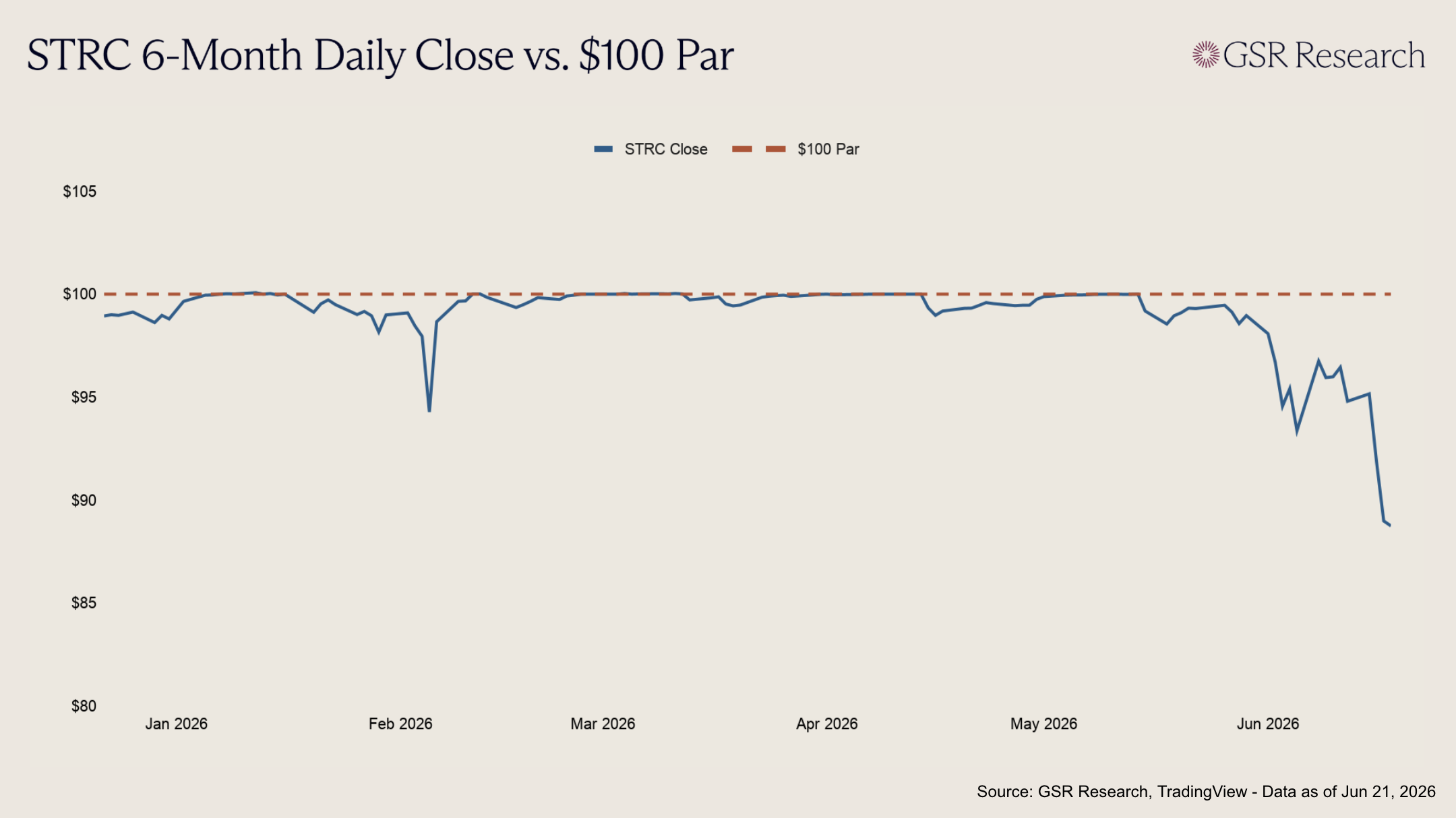

Strategy designed STRC to be the calm corner of its capital structure, a preferred share that would sit at $100 and pay a steady dividend. That hasn’t turned out to be the case over the past month. STRC closed near $89 after falling to $82.53 intraday on June 18, and it has not traded at $100 since mid-May. That is a significant stumble for an instrument whose appeal depends on its stability. It also matters beyond STRC holders, since the peg at par is part of what keeps Strategy's Bitcoin accumulation machine running.

To see why, it helps to understand how STRC works. It is perpetual, so no maturity pulls it back to $100, and holders cannot redeem on demand, which leaves only Strategy's monthly dividend resets and the company’s issuer-side redemption features to anchor it near par. The rate has risen from 9% at launch to 11.5% today, but the reset mechanism is not a hard peg. The model works best when Strategy can issue STRC near par through its ATM program, because that turns preferred-share demand into capital without forcing sales at a discount. Once STRC trades materially below $100, that channel becomes less attractive, and dividends must be supported by the USD reserve, other capital-markets activity, software-business cash generation, or, in some circumstances, bitcoin sales.

The discount to par is a clear signal that the market has concerns about the instrument. Since Strategy appears well equipped to cover STRC-related obligations in a hypothetical liquidation event, it seems the market concern is mostly about the company’s ability to continue to pay dividends. Strategy's roughly 847,363 Bitcoin are worth around $54 billion today, compared with roughly $6.7 billion of convertible notes, and about $15.5 billion in aggregate preferred notional outstanding as of the latest disclosure in May 25th. Even though the preferred’s are not Bitcoin-collateralized, given the substantial asset coverage it’s likely STRC could return to par in a wind-down, so the discount most likely reflects concerns about the dividend mechanism, and about how long the company can keep defending the peg as conditions tighten.

The unease regarding the dividend payments is understandable. Defending the peg now means lifting a coupon that already sits at 11.5%, where the discount has pushed the effective yield close to 13%, and each hike both adds to the cash bill and signals strain, so the one lever designed to hold par has lost much of its power. Income investors also have alternatives now that the debt-free Bitcoin treasury Strive has launched the higher-yielding preferred share SATA. On top of that, with Bitcoin now trading below Strategy's roughly $75,000 average cost, the question of where the dividend cash ultimately comes from has become harder to wave away.

Compounding the challenge, Strategy’s common-equity funding channel is also less powerful than it was when MSTR traded at a large premium to the value of its Bitcoin holdings. At a compressed equity premium, common issuance generates less incremental Bitcoin per share and can become dilutive if it flips into a discount. With the common at a compressed premium and the preferred below par, both funding channels have weakened at the same time, which is what ultimately pushed the company to sell Bitcoin in late May, parting with 32 BTC in its first sale since 2022. When Saylor opened the door to selling bitcoin last month, this is the dynamic that was foreshadowed.

None of this amounts to a crisis just yet. Strategy still holds more Bitcoin than any other company, has built a dedicated dollar reserve of around $1.4 billion, earns over a hundred million in revenue a year from its legacy software business, and has some options, including holding or raising the dividend rate, leaning on its designated dollar reserve, issuing other securities when market conditions allow, or selectively selling BTC. Because STRC dividends are cumulative, even a deferred dividend would accrue rather than trigger a default. However, it’s worth pondering what the episode says about the preferred-equity playbook that so many digital-asset treasuries have rushed to copy. For now the discount looks survivable, but whether Strategy can walk STRC back toward par without a punitive rate hike will tell us whether the model holds up when Bitcoin moves sideways or lower, rather than only when it climbs.

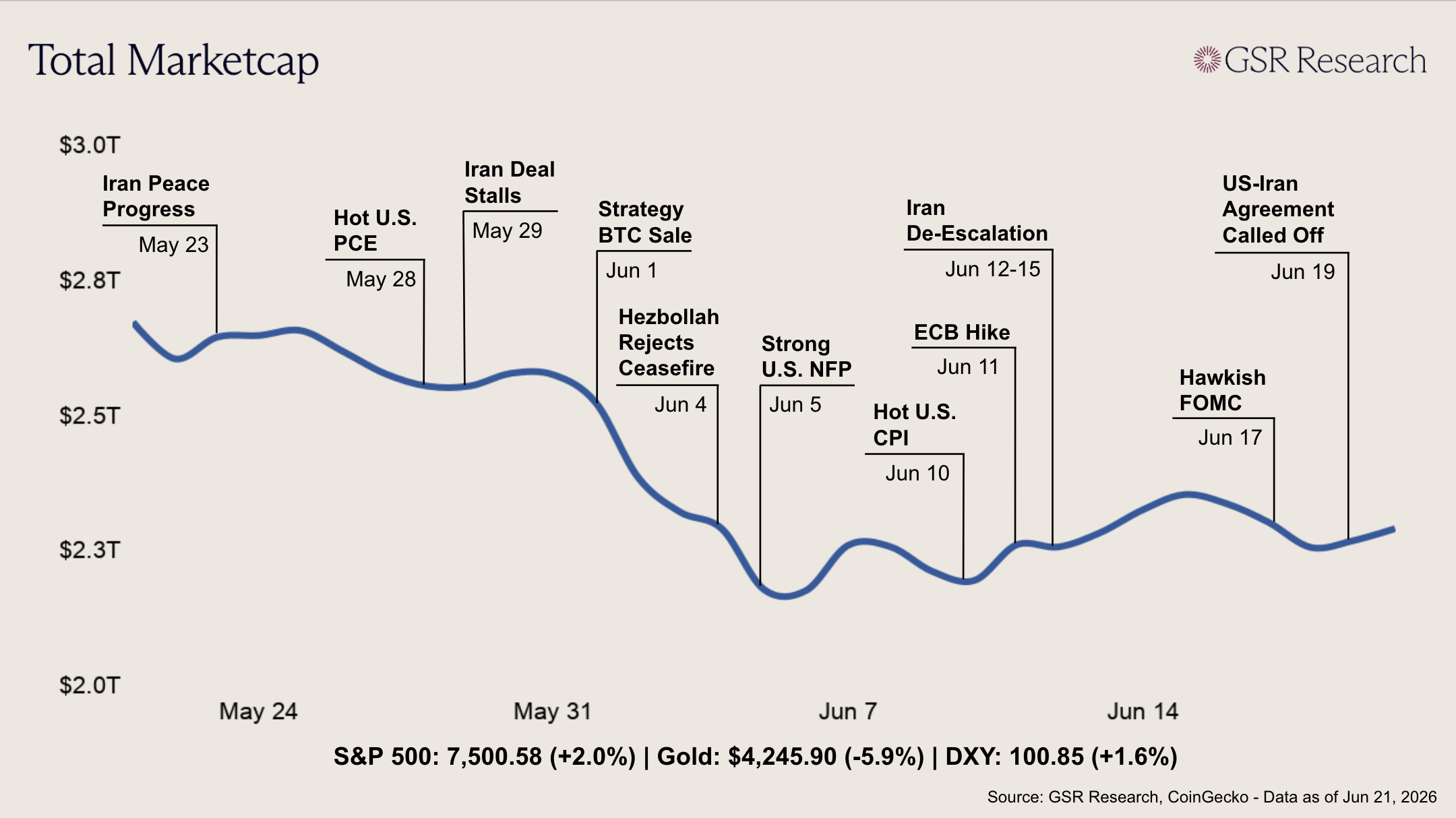

Crypto ended last week close to where it started, though it took a rocky path to get there, caught between Kevin Warsh's first meeting as Fed chair and an on-again, off-again peace deal between the US and Iran. Total market cap opened near $2.27T, sagged through the middle of the week, and finished close to where it started around $2.28T, with Bitcoin tracing a wide round trip from roughly $64,000 up toward $66,000 ahead of the Fed, down near $62,000 by Friday, and back to about $64,000 by Monday. Ether traced a similar path but finished firmer, ending near $1,723 (up about 3.6% on the week), with digital assets again trading as the high-beta end of the risk trade.

The Fed was the bigger of the two forces. As expected, Warsh's committee left rates at 3.50% to 3.75%, but the projections that came with the decision told a more hawkish story, as the median official now sees rates ending the year higher than they sit today, a clear reversal from March, with nine of eighteen policymakers projecting at least one hike before year-end. Markets immediately adjusted rate expectations, pricing roughly two-thirds odds of a hike by September, sending the dollar to a one-year high and knocking gold to a third straight weekly loss. Crypto fell along with other risk assets, with hopes for rate cuts now gone, removing the cheaper liquidity that had helped carry the rally earlier in the year.

Geopolitics was the other source of volatility, and arguably its most dramatic moment came on Friday, when the ceasefire framework between the U.S. and Iran that had been calming energy markets nearly came undone, as the talks due to take place in Switzerland to implement a peace agreement were called off after the conflict between Israel and Hezbollah flared up, prompting Iran to pull its delegation and briefly raising fears of a rough Monday open. Those fears eased in the early hours of Monday, when the two sides agreed a 60-day roadmap toward a final deal, and oil held well below its conflict highs throughout (Brent near $80, down by roughly a third from the peak), so the relief on energy prices largely stuck even as the diplomacy wobbled. With that shock mostly behind it, attention turns back to the data, leaving this week's GDP and PCE readings as the next test of whether crypto can find its footing.

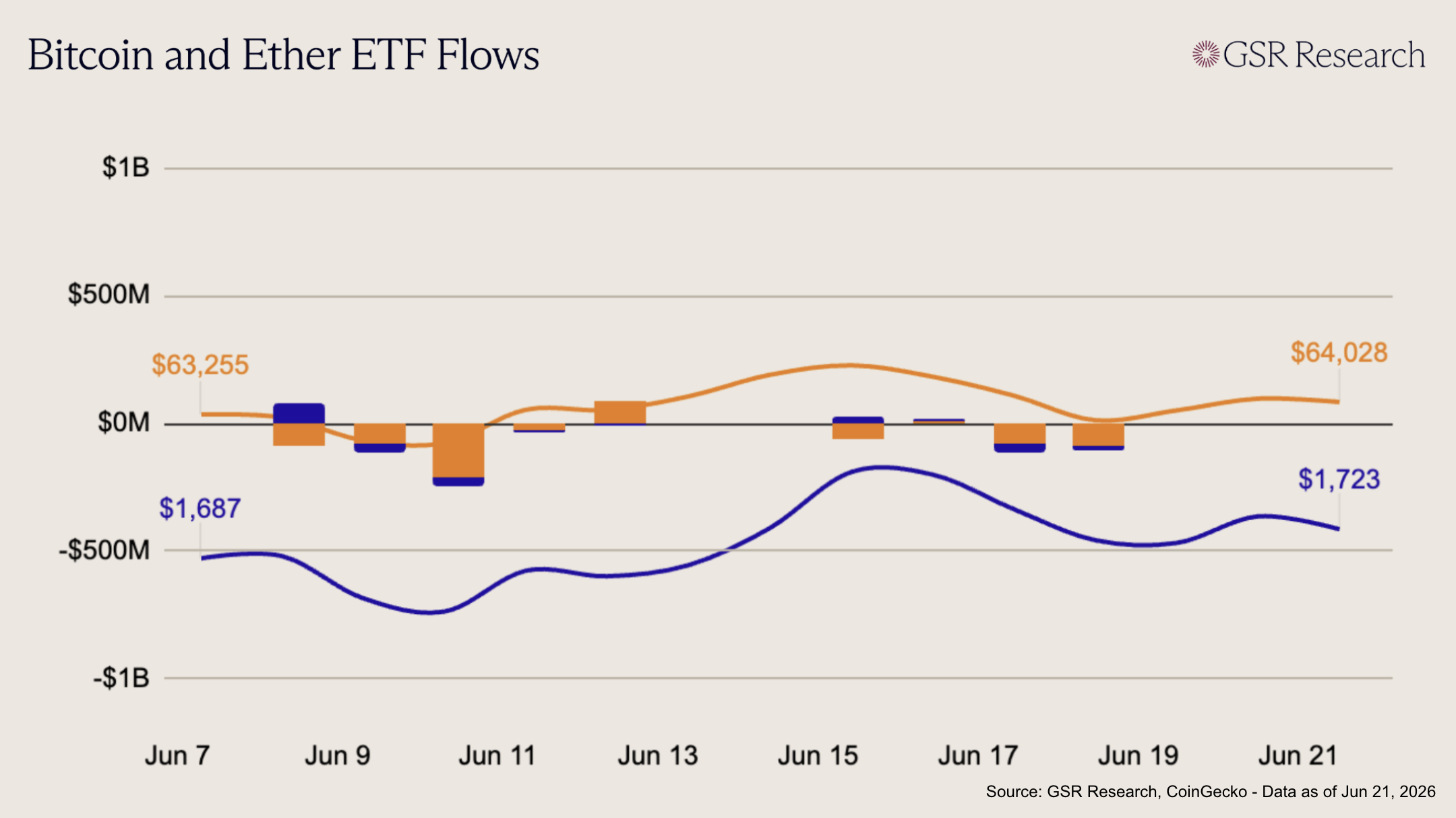

Bitcoin ETFs remained under pressure this week, with the rebound attempt from Jun 16 failing to hold. The week opened with a negative print on Jun 15 (-$65M), driven largely by GBTC outflows (-$124M), despite a partial offset from IBIT (+$66M). Flows briefly turned positive on Jun 16 (+$10M), but the stabilization proved short-lived, with redemptions returning on Jun 17 (-$82M) and deepening on Jun 18 (-$91M). The later-week pressure was led primarily by renewed IBIT weakness, which lost -$31M on Jun 17 and -$97M on Jun 18, while ARKB and HODL also added to the drag. Across the four trading sessions, BTC ETFs lost roughly -$228M, indicating that demand remains fragile and that last week’s Friday inflow did not translate into a sustained reversal.

Ether ETFs were closer to flat but still ended the week slightly negative, with early inflows offset by back-half redemptions. The week began constructively, with inflows on Jun 15 (+$23M) and Jun 16 (+$10M), led mainly by ETHA, which added +$18M and +$17M across those sessions. However, momentum faded midweek, with ETH ETFs posting outflows on Jun 17 (-$29M) and Jun 18 (-$13M), driven by renewed weakness in ETHA and smaller redemptions across FETH, ETHW, TETH, ETHV, ETHE, and ETH. Across the week, ETH ETFs lost roughly -$10M. While the magnitude of selling was much lighter than BTC, the inability to sustain early-week inflows points to continued caution, with ETH demand stabilizing but not yet showing durable follow-through.

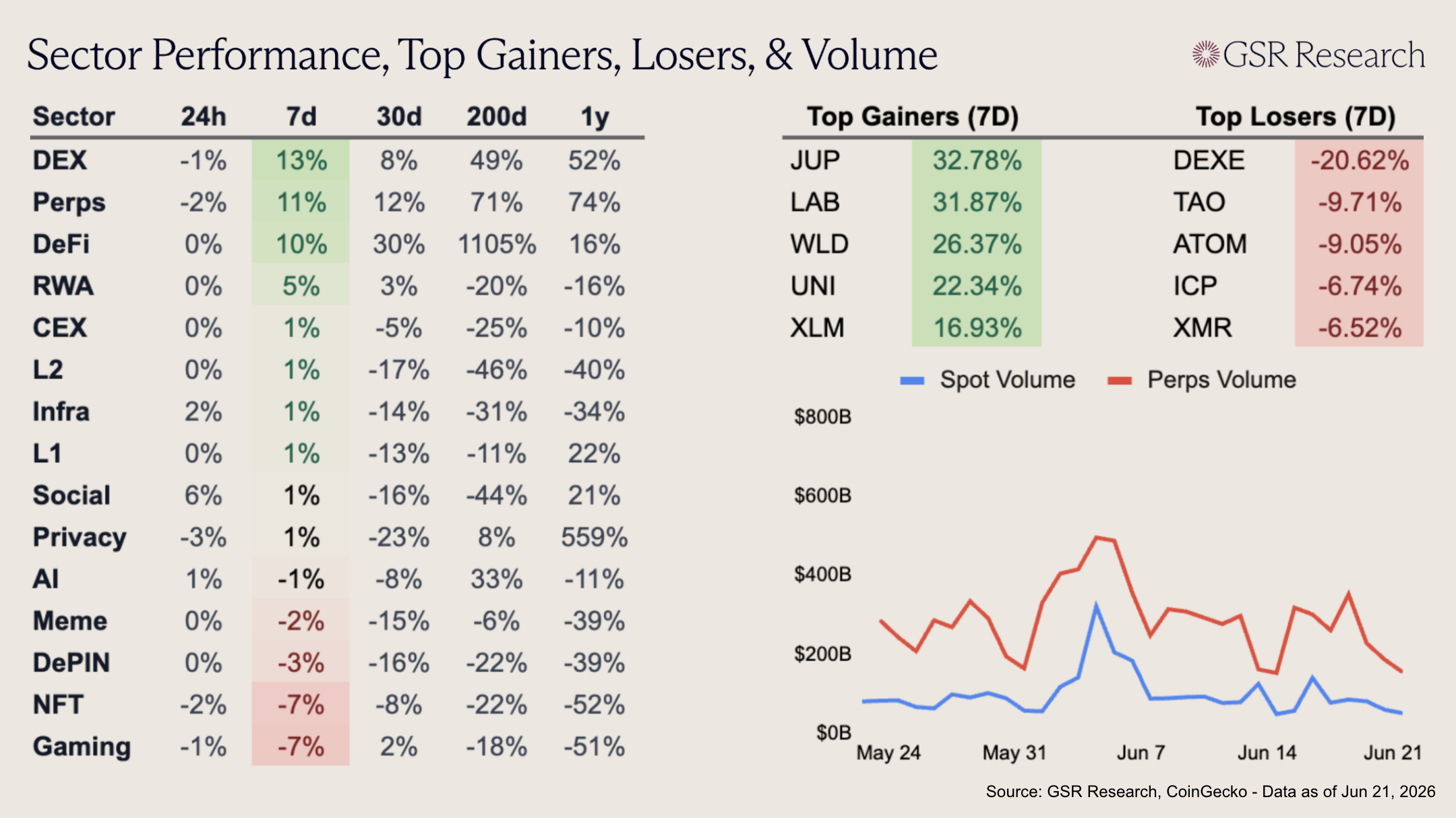

DEX, Perps, and DeFi led this week, up 13%, 11%, and 10%, respectively, as spot DEX and value-accrual trades outperformed a mostly mixed tape. JUP (+32.78%) was the top gainer and the main driver of strength across all 3, with traders rotating back into Jupiter as attention returned to its protocol-fee buyback model and a community proposal to increase the Litterbox allocation from 50% to 70%. UNI (+22.34%) also rallied after Standard Chartered initiated coverage with a $100 2030 price target, framing Uniswap as a core beneficiary of tokenized assets moving into DeFi. Perps were supported by DYDX (+8.13%), which has benefited from renewed focus on its 75% protocol-fee buyback program. WLD (+26.37%) gained as traders continued to price its upcoming 43% reduction in daily emissions, while XLM (+16.93%) helped RWA rise 5% as fresh Stellar RWA integrations extended the DTCC/Stellar narrative.

Weakness was more idiosyncratic. DEXE (-20.62%) was the week’s biggest loser after breaking below $15 support, reversing part of its earlier short-squeeze rally as selling pressure picked up. TAO (-9.71%) gave back part of its Anthropic/export-control move as debate around Bittensor’s Root Reborn proposal and whale selling weighed on the token, pulling DePIN down 3%. ATOM (-9.05%) retraced after last week’s Robinhood re-listing rally, with volume fading as the initial retail-access bid failed to carry into a second week. ICP (-6.74%) underperformed amid broader risk-off flows and weak buyer conviction, while XMR (-6.52%) pulled back after its mid-June spike tied to roughly $120m of USDT being routed through Monero left the token vulnerable to profit-taking. Gaming and NFT were also weak, both down 7%, as BEAT’s prior parabolic rally reversed sharply.

Click here to download the PDF of the report

This material is provided by GSR (the “Firm”) solely for informational purposes. It is not intended to be advice or a recommendation to buy, sell or hold any investment mentioned. Investors should form their own views in relation to any proposed investment.

It is intended only for sophisticated, institutional investors and does not constitute an offer or commitment, a solicitation of an offer or commitment, or any advice or recommendation, to enter into or conclude any transaction (whether on the terms shown or otherwise), or to provide investment services in any state or country where such an offer or solicitation or provision would be illegal. The Firm is not and does not act as an advisor or fiduciary in providing this material.

This material is not an independent research report, and has not been prepared in accordance with any legal requirements by any regulator (including the FCA, FINRA or CFTC) designed to promote the independence of investment research.

This material is not independent of the Firm’s proprietary interests, which may conflict with the interests of any counterparty of the Firm. The Firm may trade investments discussed in this material for its own account, may trade contrary to the views expressed in this material, and may have positions in other related instruments. The Firm is not subject to any prohibition on dealing ahead of the dissemination of this material.

Information contained herein is based on sources considered to be reliable, but is not guaranteed to be accurate or complete. Any opinions or estimates expressed herein reflect a judgment made by the author(s) as of the date of publication, and are subject to change without notice. The Firm does not plan to update this information.

Trading and investing in digital assets involves significant risks including price volatility and illiquidity and may not be suitable for all investors. The Firm is not liable whatsoever for any direct or consequential loss arising from the use of this material. Copyright of this material belongs to GSR. Neither this material nor any copy thereof may be taken, reproduced or redistributed, directly or indirectly, without prior written permission of GSR.

Please see here for additional Regulatory Legal Notices relevant to US, UK and Singapore.