GSR Weekly Update - July 13th, 2026

BTC: $64,084 (+2.1%) | ETH: $1,819 (+2.6%) | BTC Dom: 56.2% | Global Cap: $2.29T

Carlos Guzman

Research Analyst

Slater Santer

Research Analyst

BTC: $64,084 (+2.1%) | ETH: $1,819 (+2.6%) | BTC Dom: 56.2% | Global Cap: $2.29T

Carlos Guzman

Research Analyst

Slater Santer

Research Analyst

Gauntlet announced a $125M Series C last week funded solely by SBI Holdings at an undisclosed valuation, marking one of the largest raises ever for a DeFi risk and curation protocol. Gauntlet, originally a protocol consulting firm focused on consensus and agent-based modeling, later pivoted to risk management and curation as lending markets became more modular. In Morpho V2 and similar systems, curators are the entities that decide where capital goes, what collateral is accepted, how exposures are capped, which markets receive liquidity, and how quickly portfolios adjust when conditions change. They do not custody user assets in the traditional sense, but they increasingly perform the underwriting, monitoring, and portfolio construction functions that make onchain credit usable for institutions and retail distribution partners.

The raise is significant because it lands directly in the curator layer, which has quietly become one of the most important parts of the DeFi stack. A lending protocol can provide the rails, but the curators on top of the platform are responsible for providing the true onchain asset management product. Investors are now directly underwriting the thesis that risk curation, rather than base-layer lending code, is a durable value accrual model in modular DeFi credit.

Curators are easiest to understand through their economic function rather than their contract roles. In Morpho's Vault V2 architecture, the protocol provides the balance-sheet rails, accounting, and execution interfaces, while the curator provides underwriting policy and portfolio construction: which collateral and markets are approved, how large each exposure can get, what LTVs and oracles apply, and how quickly capital gets reallocated when conditions change. Deposits stay noncustodial and major actions sit behind timelocks, but the substantive decisions about where user capital goes are made by the curator. A curator’s function is best understood as running a credit fund in 24/7 composable markets, monetized with a simple performance fee, with most curator fees ranging from 0% to 20% of native APY.

Gauntlet’s raise therefore matters less because of the headline number and more because of where it lands in the stack. The $125M raise is one of the clearest signs yet that the market is beginning to value curation as its own category of onchain asset management. Gauntlet spent years as a protocol risk advisor before recentering around curation, scaling to just under $1B on Morpho in roughly 18 months, and now curates more than $1.5B across Morpho, Kamino, Aera, and Symbiotic while integrating with 150+ fintechs and institutions. The newly raised funds will support broader stablecoin coverage, including non-dollar markets like yen and pesos, global hiring, and capital deployment into new onchain offerings.

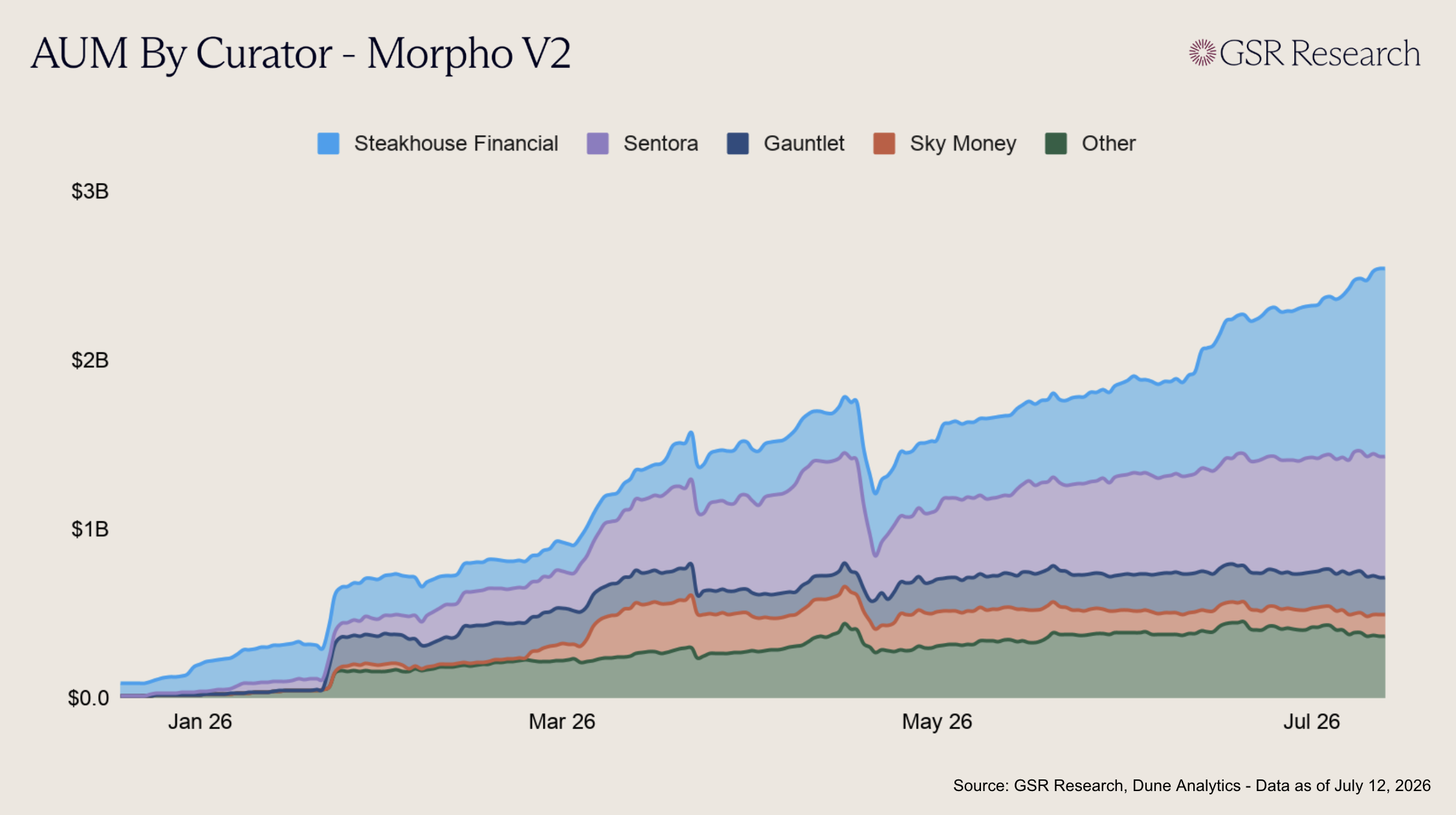

Morpho launched Vaults V2 last September, and AUM has remained heavily concentrated, with Steakhouse Financial at over $1B, Sentora at roughly $700M, and Gauntlet at $230M, putting roughly 80% of capital in the hands of 3 curators. Steakhouse's dominance is the clearest evidence that distribution, not headline APY, remains the real contest among managers as it curates both Coinbase's high-yield USDC vault and Robinhood Earn (which we covered here), with some of its steepest periods of growth lining up with those two launches in June and July respectively.

The important caveat is that this data captures Morpho V2 curators only. It excludes legacy Morpho vaults, curation on Solana through Kamino (which added Gauntlet as an official curator last November), and mandates on platforms like Aera and Symbiotic. The data also shows why curation is risk capital rather than sticky fund management. In late April, V2 curator AUM fell by roughly a third in under a week, a drawdown that lines up with the KelpDAO exploit and April's record hack wave (we covered that here), before recovering to new highs. With 3 firms intermediating most of the flow, a model error or slow reaction for one curator propagates quickly. If distribution platforms treat vaults as interchangeable yield backends, curation fees will compress toward infrastructure pricing, but if branded risk management keeps earning trust even through events like April, the top curators will end up owning a significant layer of onchain credit.

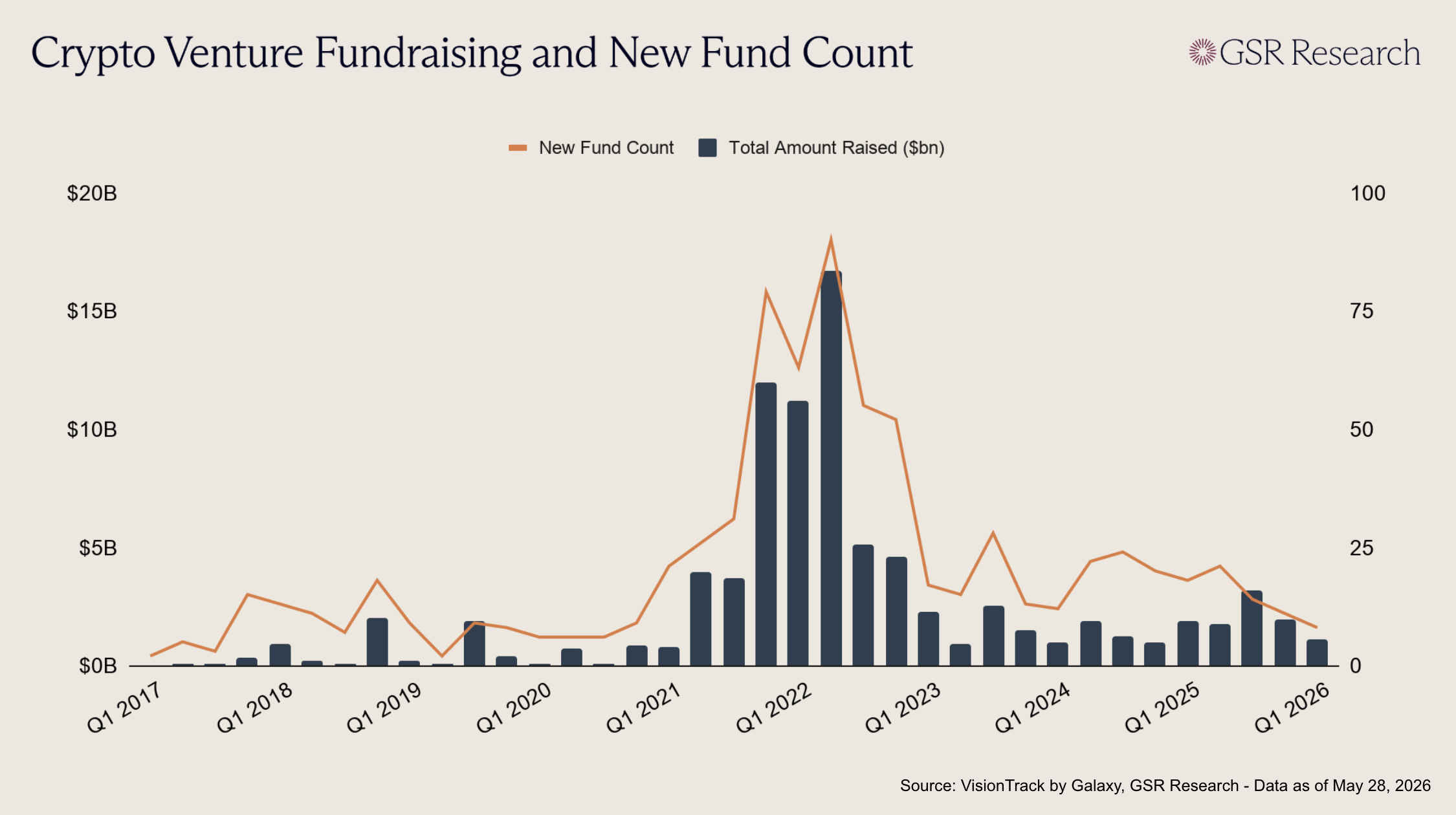

On July 8, Paradigm announced the close of its fourth fund at $1.2 billion, with co-founder Matt Huang framing the vehicle as an investment across the "technical frontier" of crypto, AI, and robotics. The raise marks a meaningful recovery from the firm's $850 million second venture fund in 2024, though it came in below the $1.5 billion target the Wall Street Journal reported earlier this year and well below the $2.5 billion flagship that made Paradigm one of the largest crypto VCs in late 2021. That trajectory, a peak during the boom followed by a reset and then a partial rebound, mirrors the crypto venture landscape more broadly.

Paradigm is one of several top-tier firms that have raised new funds in recent months. a16z crypto closed $2.2 billion for its fifth vehicle in May, Haun Ventures raised $1 billion around the same time, Framework Ventures brought in $400 million in June, Variant raised $222 million, and Dragonfly opened the year with a $650 million close in February. Those six funds account for roughly $5.7 billion in fresh commitments, evidence that institutional appetite for crypto has not disappeared.

Set against the 2021-2022 cycle, however, the fundraising picture has changed substantially. a16z crypto's previous fund was $4.5 billion, making the new one less than half that size. Paradigm itself has shrunk by more than half from its peak. Investment into crypto startups overall topped $33 billion in 2022, collapsed to around $14 billion by 2024, and while 2025 saw some recovery, new fund formation in Q1 2026 hit its lowest quarterly count since late 2020, with only eight new funds started during the quarter. The capital that does flow in has been concentrating heavily among proven firms, with the mid-tier struggling to raise or quietly stepping back. Dragonfly general partner Rob Hadick has described the environment as a "mass extinction event" for crypto VCs. Amid a crypto bear market, we’re looking at fundraising environment that is rewarding the firms that have survived long enough to build real track records.

One of the most notable features of these recent raises is how many of them are expanding beyond pure crypto investing. Paradigm explicitly added AI and robotics to its scope, pointing to portfolio companies like autonomous drone firm Zipline and AI research lab Nous Research. Framework is deploying into AI, robotics, and energy alongside its stablecoin and tokenization bets. Haun organized its fund around three pillars, one of which it calls the "agentic economy," where AI systems transact autonomously and may need crypto-native payment and identity infrastructure. Variant reframed its thesis entirely around "autonomy" to encompass both decentralized ownership and AI agent coordination.

Some of this is pragmatic, since LPs are easier to court with a frontier-tech mandate than a pure crypto pitch in the current environment. However, it arguably also reflects a genuine convergence these firms are identifying between crypto infrastructure and AI. As autonomous agents grow more capable and begin managing payments, coordinating resources, and transacting with each other at machine speed, the programmable financial rails that blockchains provide become a natural fit. Nearly every major crypto fund is making some version of this bet, positioning at the intersection where AI agents meet onchain finance, and while the thesis still needs real product traction to prove itself out, the convergence in conviction among the industry's top allocators is a signal that is hard to dismiss.

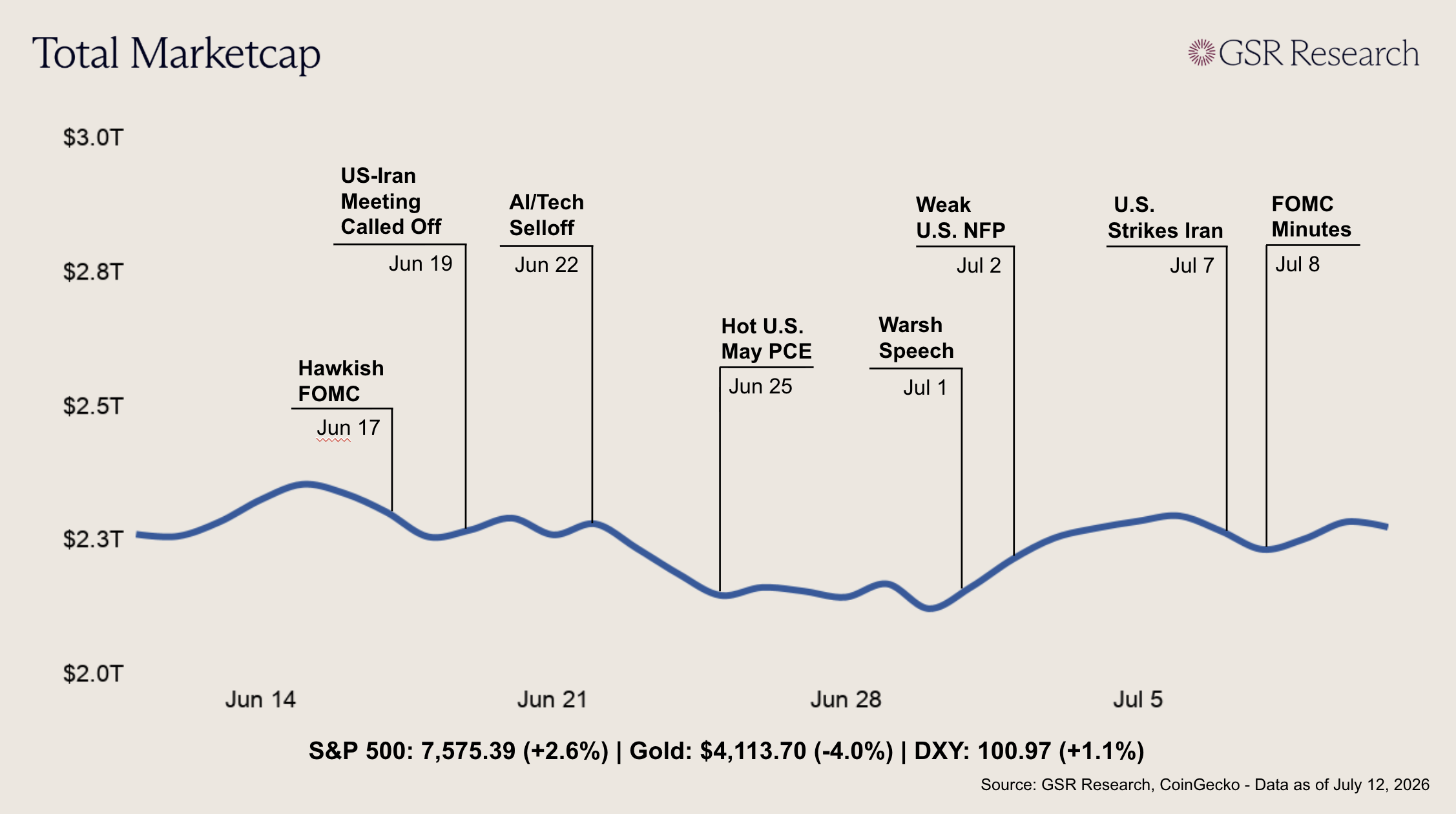

The conflict in the Middle East retook center stage this week for crypto markets. Bitcoin started the week around $62,500 and held up into Tuesday, then fell below $62,000 on Wednesday after the U.S. launched a second round of strikes on Iran and President Trump said the ceasefire was over. Prices steadied later in the week, and Bitcoin recovered to about $64,300 by Friday before slipping to roughly $62,800 on Monday, when fresh strikes over the weekend and an Iranian threat to close the Strait of Hormuz reignited selling pressure. Total market value ended near where it began, around $2.27 trillion.

The fighting affected crypto mostly through a spike in oil prices, as Brent gained more than 5% on the week to trade near $79 and WTI settled around $74. About a fifth of the world's oil passes through Hormuz, and shipping there is still disrupted. Higher energy prices feed back into inflation, which is the main reason the Federal Reserve has stayed on hold. Minutes from the June meeting, released Wednesday, showed policymakers split over whether the next move is a cut or a hike, with inflation above the 2% target and the funds rate steady at 3.50% to 3.75%. Equities took the same headlines in stride and set new records on continued enthusiasm for AI, while crypto stayed well below the highs it reached late last year.

June inflation figures are set to be released on Tuesday and will provide an important read on how higher energy prices are filtering through to inflation. Other upcoming events to watch will be the July 24 expiry of the temporary 10% import tariff and the Fed's meeting on July 28 and 29, which could both shape how much rate-hike risk stays in the market.

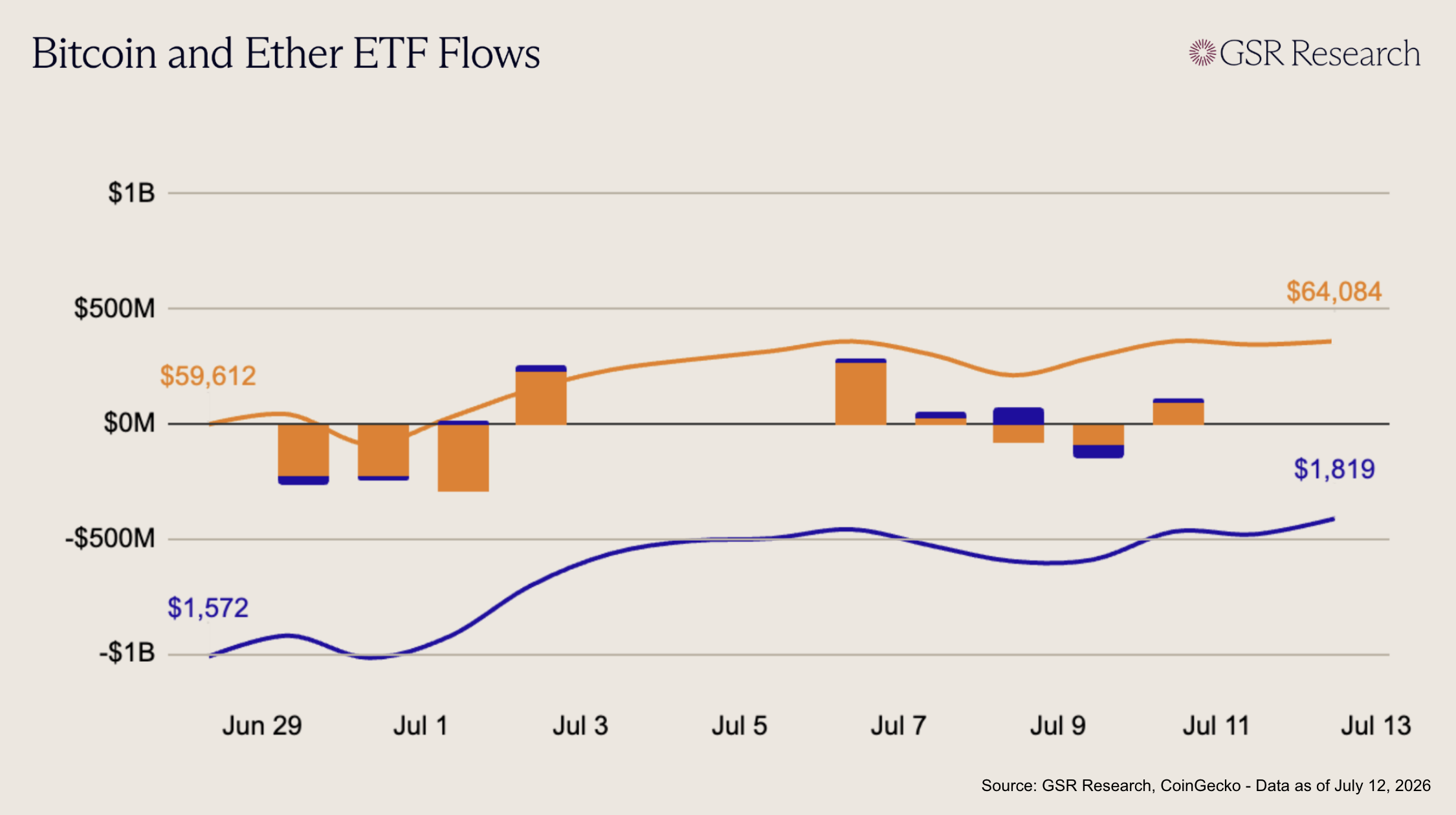

Bitcoin ETFs stabilized this week, breaking from the prior redemption-heavy pattern with a modestly positive aggregate flow profile. The week opened with a strong inflow on Jul 6 (+$266M), led by IBIT (+$209M), followed by a smaller positive print on Jul 7 (+$22M). Momentum weakened midweek, with outflows on Jul 8 (-$85M) and Jul 9 (-$95M), driven primarily by renewed pressure in FBTC, ARKB, and GBTC. However, flows turned positive again into the close, with Jul 10 adding +$90M as IBIT returned to inflow territory. Across the week, BTC ETFs gained roughly $197M, suggesting that demand has improved from the late-June drawdown, though the choppy midweek reversals show that institutional conviction remains uneven.

Ether ETFs showed a more constructive flow profile, finishing the week positive despite one sharp midweek outflow. The week began with three consecutive inflow sessions: +$21M on Jul 6, +$27M on Jul 7, and +$71M on Jul 8, with the Jul 8 print driven largely by FETH (+$69M). Flows briefly reversed on Jul 9 (-$52M), led by outflows from FETH, ETHA, ETHB, and ETHW, but the weakness proved short-lived as Jul 10 returned to positive territory (+$18M). Across the five sessions, ETH ETFs gained roughly $84M. While the absolute inflow total remains modest, the consistency of positive sessions suggests that ETH demand is continuing to stabilize and is showing better follow-through than in the prior redemption cycle.

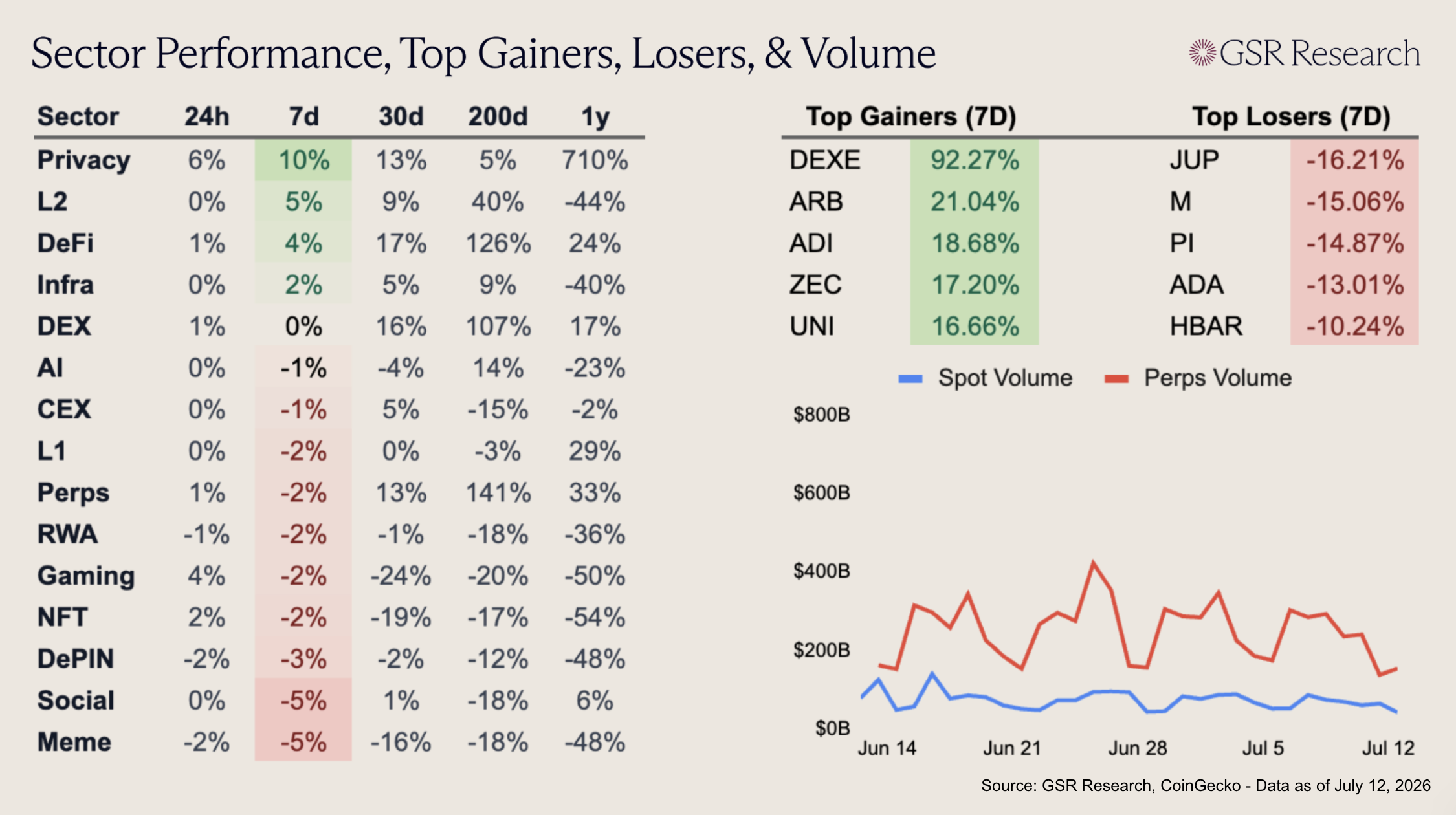

Sector performance was modestly positive this week, with Privacy, L2, and DeFi leading the market, up 10%, 5%, and 4%, respectively. Privacy strength was driven by ZEC (+17.20%), which continued to recover after the Orchard disclosure as investors looked ahead to the Ironwood upgrade. L2s also outperformed as ARB (+21.04%) rallied on Robinhood Chain’s mainnet launch on the Arbitrum platform, while ADI (+18.68%) extended gains after LetsExchange listed the institutional RWA and stablecoin-focused L2 token. DeFi gained 4% as DEXE (+92.27%) surged to new highs on record whale activity, new wallet growth, and a ChangeNOW listing, while UNI (+16.66%) benefited from Uniswap’s day-one Robinhood Chain integration as the network’s primary public AMM.

Downside was mostly concentrated in a few prior leaders. DEX finished flat despite UNI’s rally as JUP (-16.21%) retraced amid renewed debate over tokenomics and the effectiveness of buybacks against high staking inflation. Meme was down 5% as M (-15.06%) gave back part of last week’s $10m buyback-driven rebound, while PI (-14.87%) stayed under pressure from its July unlock schedule. ADA (-13.01%) slipped back toward multi-year lows as the market continues to price in Hoskinson's departure, and HBAR (-10.24%) rounded out the top losers after Hedera-based Bonzo Lend suffered a roughly $9m oracle exploit.

This material is provided by GSR (the “Firm”) solely for informational purposes. It is not intended to be advice or a recommendation to buy, sell or hold any investment mentioned. Investors should form their own views in relation to any proposed investment.

It is intended only for sophisticated, institutional investors and does not constitute an offer or commitment, a solicitation of an offer or commitment, or any advice or recommendation, to enter into or conclude any transaction (whether on the terms shown or otherwise), or to provide investment services in any state or country where such an offer or solicitation or provision would be illegal. The Firm is not and does not act as an advisor or fiduciary in providing this material.

This material is not an independent research report, and has not been prepared in accordance with any legal requirements by any regulator (including the FCA, FINRA or CFTC) designed to promote the independence of investment research.

This material is not independent of the Firm’s proprietary interests, which may conflict with the interests of any counterparty of the Firm. The Firm may trade investments discussed in this material for its own account, may trade contrary to the views expressed in this material, and may have positions in other related instruments. The Firm is not subject to any prohibition on dealing ahead of the dissemination of this material.

Information contained herein is based on sources considered to be reliable, but is not guaranteed to be accurate or complete. Any opinions or estimates expressed herein reflect a judgment made by the author(s) as of the date of publication, and are subject to change without notice. The Firm does not plan to update this information.

Trading and investing in digital assets involves significant risks including price volatility and illiquidity and may not be suitable for all investors. The Firm is not liable whatsoever for any direct or consequential loss arising from the use of this material. Copyright of this material belongs to GSR. Neither this material nor any copy thereof may be taken, reproduced or redistributed, directly or indirectly, without prior written permission of GSR.

Please see here for additional Regulatory Legal Notices relevant to US, UK and Singapore.