GSR Weekly Update - July 6th, 2026

BTC: $62,574 (+4.6%) | ETH: $1,769 (+12.0%) | BTC Dom: 55.6% | Global Cap: $2.26T

On June 30, Open Standard announced Open USD (OUSD), a new dollar stablecoin backed by more than 140 companies spanning nearly every corner of payments and finance, with Visa, Mastercard, American Express, Stripe, BlackRock, BNY, Coinbase, Shopify, and Google among the names on the list. The venture will be run by Open Standard, an independent company headed by Bridge co-founder Zach Abrams, and is built around three core pillars: partners can mint and redeem at no cost and without volume limits, reserve earnings flow back to partners less a small management fee, and governance sits with a board drawn from the partners themselves. The token is expected to go live later this year, and its perceived impact on stablecoin incumbents was immediately felt, with Circle's stock closing down nearly 18% on the day.

Open USD’s design upends the economics that made Tether and Circle so profitable. Stablecoin issuers tend to keep a large portion, if not most of, the yield on the treasuries backing their tokens, while the exchanges, wallets, processors, and platforms that actually put those tokens into circulation have historically captured little of it. Open USD hands that float to its distributors, turning idle stablecoin balances into a revenue line for anyone moving money at scale and giving the industry's largest distribution channels a direct incentive to prefer OUSD over the incumbents. Coinbase's participation is notable here, given the company co-founded USDC alongside Circle and reportedly earned over $900 million from its distribution in 2024. It’s telling that even the ecosystem's best-compensated distributor is keeping its options open (while, perhaps not coincidentally, gaining leverage ahead of the reported renewal of its Circle agreement in August).

The move to launch OUSD can also be read as a course correction for Stripe’s Bridge. Since launching Open Issuance last fall, Bridge has helped partners like Phantom, MetaMask, MoneyGram, and others spin up their own branded stablecoins, with a similar pitch of letting businesses own their economics. Those stablecoins let each partner benefit from its own float but gave them little in the way of shared liquidity. As we noted in our April 13th update about Polymarket’s stablecoin, app specific stablecoins create fragmentation, which dilutes network effects and imposes a challenge for their adoption compared to incumbents. Open USD suggests Bridge has concluded that fragmentation was becoming a major hurdle for its Open Issuance approach, so the partners are now pooling distribution behind a single token while keeping Open Issuance coins swappable into OUSD one for one, leaving the branded stablecoins as storefronts and OUSD as the shared settlement asset behind them.

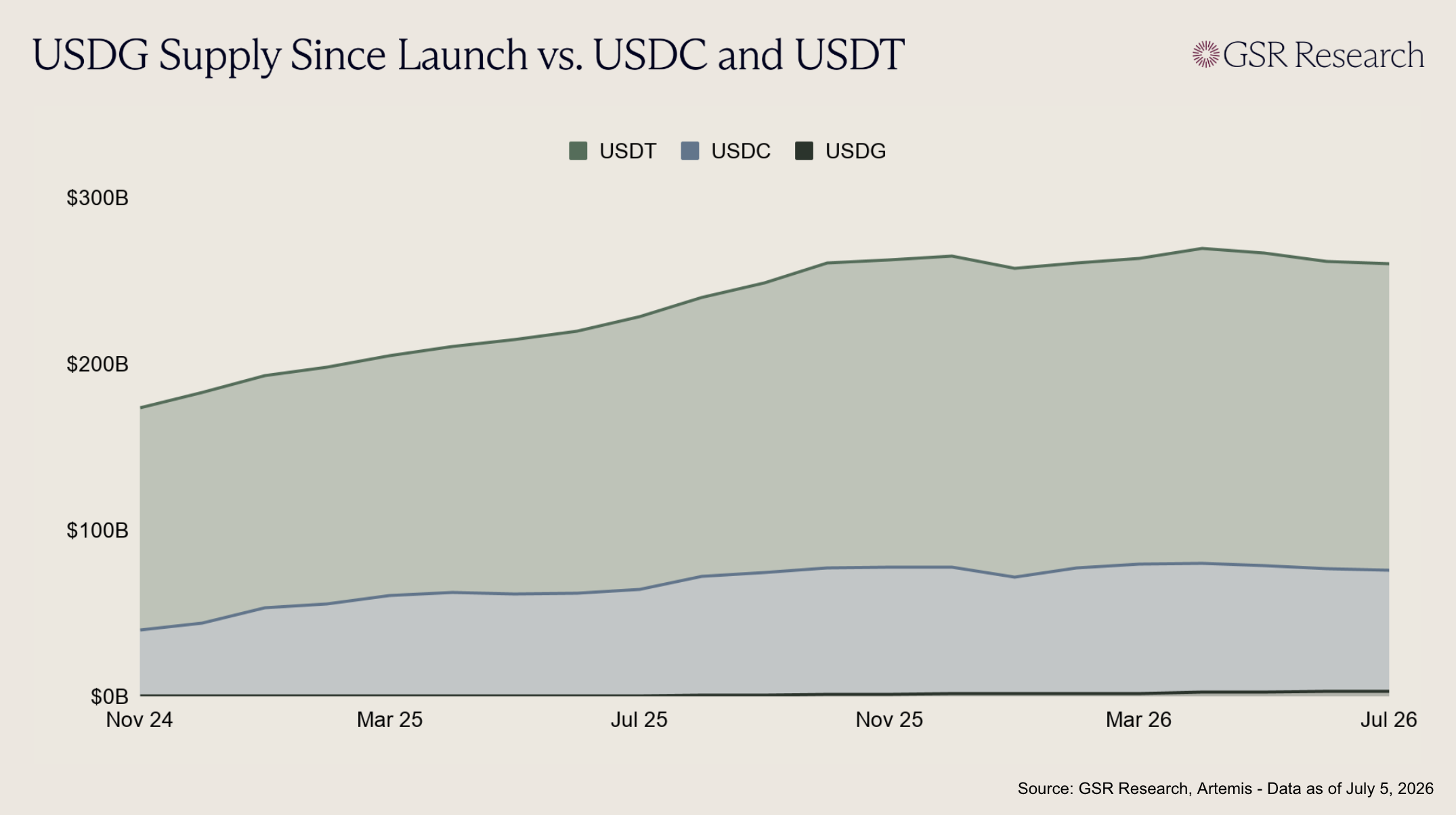

Despite the apparent strengths of the Open USD approach, it’s still an open question whether a committee of 140 can actually take share from Tether and Circle. The precedent here provides some reason for caution. Paxos launched the Global Dollar Network in late 2024 with a similar revenue-sharing pitch and partners including Mastercard, Kraken, and Robinhood, yet USDG has grown to only around $3 billion against roughly $73 billion for USDC and $184 billion for USDT. Open USD's roster is broader and its economics more aggressive, but its members bring different regulatory postures, existing stablecoin relationships, and outright rivalries to the table, and key details around ownership, licensing, and how reserve income will actually be divided remain undisclosed. Even so, the announcement arguably already settles one debate, in that value in stablecoins is migrating from issuance toward distribution, leaving liquidity and integrations as the incumbents' main moat. It remains to be seen whether Open USD’s aggressive distribution challenge is enough to overcome the moat that USDT and USDC have built, but it is surely the most formidable attempt to date.

At its July 1st “World is Flat” event in London, Robinhood announced one of its most aggressive crypto product expansions to date. The headline items were the public mainnet launch of Robinhood Chain, an Ethereum-compatible Layer 2 built on Arbitrum specifically for tokenized real-world assets, a new generation of Stock Tokens available in 120+ countries, and Robinhood Earn, the first decentralized lending product offered directly inside the main Robinhood app at an estimated 7% APY on USDG. The company also added perpetual futures through Lighter inside Robinhood Wallet, expanded EU perps beyond crypto into commodities, ETFs, and FX, introduced maker/taker fees as low as 0% for US crypto traders, launched in Canada, secured a Singapore capital markets license, confirmed a planned UK crypto launch, and previewed Agentic Accounts for crypto. While some of the products will not go live for months, the holistic picture is clear: Robinhood is no longer treating crypto as an add-on, but slowly recreating its entire brokerage experience onchain.

The most immediately relevant product for U.S. users is Robinhood Earn, an onchain lending product that lets eligible users lend USDG through a self-custody wallet inside the Robinhood app for an estimated 7% APY. The lending infrastructure is powered by Morpho, with Steakhouse curating the vault and Ethena, Spark, and Maple supporting the yield stack. While 7% is the initial target yield, the rate is ultimately variable based on borrower demand, vault allocation, collateral quality, and broader crypto credit conditions.

How then is Robinhood achieving 7%, a rate materially above baseline rates, especially as comparable Steakhouse-curated Morpho vaults have recently yielded in the mid-3% range? The answer is a combination of borrower interest, USDG TBill reserve yield, 0 vault fees, and a 1yr target rate Merkl campaign that pays the delta between the organic yield and the target. Minus the Merkl campaign, this is a very similar playbook to what Morpho and Steakhouse used for their high yield USDC vault on Coinbase launched in June (we covered that here), where borrowers pay a premium to borrow dollars against assets like Ethena's sUSDe and Maple's syrupUSDC.

Ultimately, the 7% rate is plausible, but not necessarily durable. Once the Merkl campaign ends and if leverage demand falls, collateral demand weakens, or the vault shifts toward safer assets, yields should compress. Robinhood has added insurance through Lloyd’s of London and RELM for certain cyber and smart contract losses, but that does not cover ordinary lending losses, liquidity issues, or weak strategy performance. At least for the first year, this will allow Robinhood Earn to remain competitive with new savings products like X money, which is targeting a 6% yield with the added bonus of FDIC insured deposits.

The new Stock Tokens are a meaningful upgrade over Robinhood's first tokenization effort, which has been rebranded as Classic Stock Tokens. Classic tokens are derivative contracts between the user and Robinhood Europe that track underlying prices, cannot be moved to outside wallets, grant no rights to the underlying securities, and trade 24/5 across 2,000+ symbols. The new tokens are tokenized debt securities issued by Robinhood Assets (Jersey) Limited, backed 1:1 by underlying shares held with a US custodian, with dividends reinvested into additional backing shares through a multiplier mechanism rather than paid out in cash. Redemption runs through the issuer and an insolvency scenario relies on an independent security agent selling the backing shares. That is a stronger backstop than a pure synthetic, but holders are still not shareholders of record, meaning Robinhood has made tokenized stocks more useful without making them more stock-like in a legal sense. Coverage is currently limited to 94 names, but the tokens trade 24/7, live in self-custody wallets, and can be swapped on DEXs like Uniswap, deployed into lending pools, or posted as collateral across DeFi. The tradeoff is breadth for utility, and utility is clearly the point, as Robinhood Chain is marketed as the blockchain for Stock Tokens and the design goal is equities as composable DeFi assets rather than synthetic exposure trapped inside a brokerage app.

However, eligibility remains a serious constraint. The tokens are available to eligible users across 120+ countries, but are explicitly unavailable to US persons, along with Canada, the UK, Switzerland, and the UAE. There is no announced US launch date, and the gating factor is legal structure rather than product readiness, as the tokens are not registered under US securities laws and cannot simply be turned on for American users without a different wrapper or a specific regulatory path. US availability is therefore an open question rather than a delayed launch.

Robinhood and Coinbase are now converging on the same end state from opposite starting points. Robinhood began as a retail brokerage and is pushing into crypto through self-custody wallets, Robinhood Chain, tokenized equities, onchain lending, perpetuals, and agentic trading. Coinbase began as a crypto exchange and is moving toward brokerage by adding tokenized stocks for non-U.S. users, stock and crypto options, crypto-backed lending, Morpho-powered yield products, Base, agentic execution, and a broader “everything exchange” strategy.

The overlap is becoming impossible to ignore. Robinhood has Robinhood Chain, Coinbase has Base. Robinhood has Earn, Coinbase has Morpho-powered lending and yield products. Robinhood is adding wallet-based perps through Lighter and expanding EU perpetuals into traditional assets, while Coinbase continues to build out international derivatives and recently absorbed Deribit. The sharpest collision is tokenized stocks, as Coinbase recently announced that it would be launching tokenized equities for non-US customers this month (we covered that here), which Coinbase marketed as true ownership with dividend payouts and full shareholder rights, a more ambitious rights package than Robinhood's debt wrapper. Each side is leaning on its native advantage, with Robinhood bringing brokerage packaging and nearly 28M customers while Coinbase brings exchange liquidity, Base, and institutional rails. We expect to see a strategic war between these two titans play out over the next few years, with the winner ultimately becoming a major player in global retail finance.

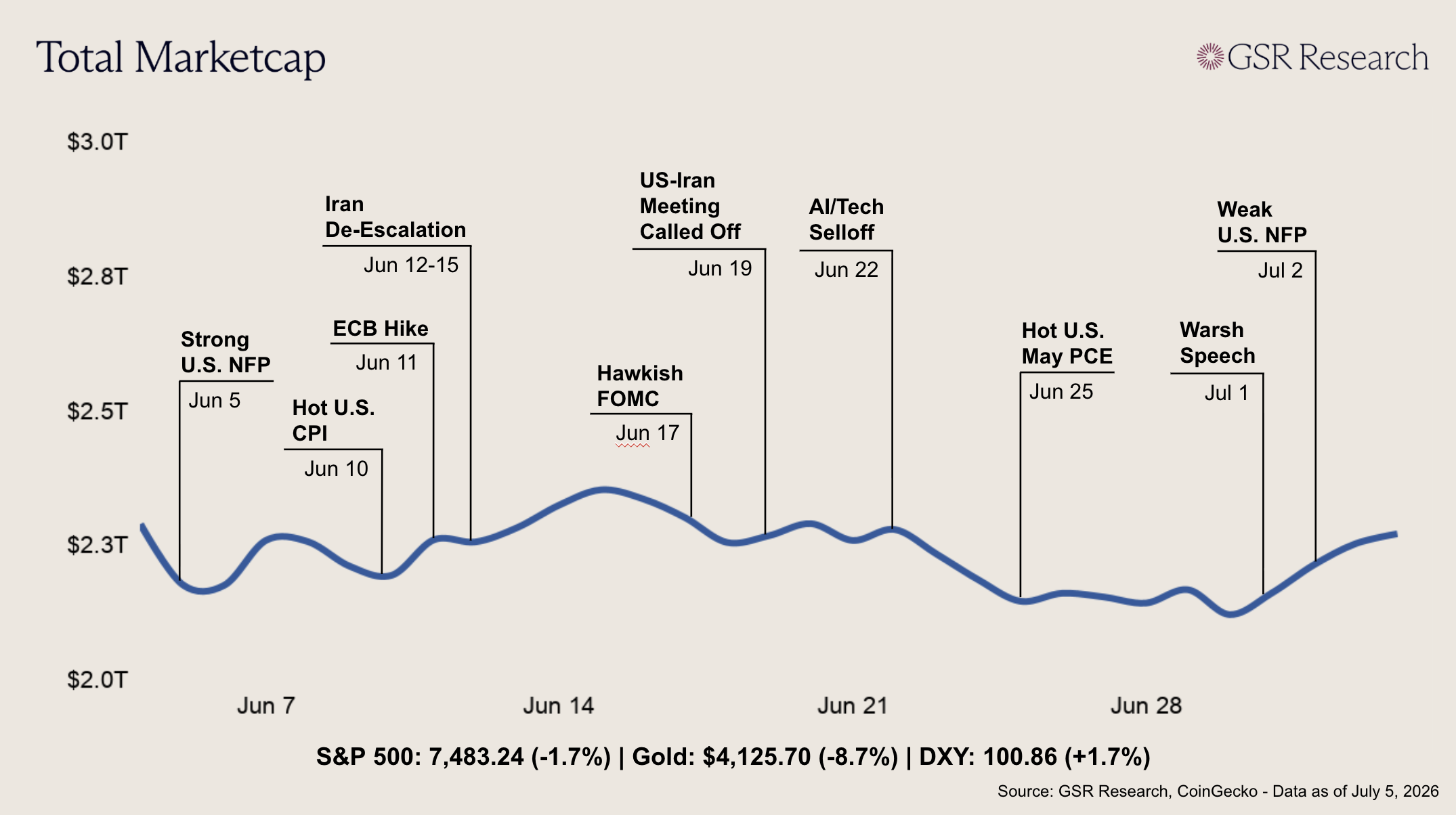

Crypto markets rebounded this week, recovering much of the ground lost in the late-June selloff as the outlook for U.S. rates softened. Bitcoin started near $59,600, retook $60,000 on Wednesday, climbed above $61,800 after Thursday's payrolls report, and briefly reclaimed $63,000 over the holiday weekend before settling around $62,574, a gain of roughly 5% on the week. Ether outperformed, rising from about $1,570 to $1,769, close to 13%, with the higher-beta parts of the market rallying hardest and lifting total market cap back toward $2.3T. Even after the bounce, Bitcoin sat just shy of where it traded in mid-June.

Two developments reset the rate picture that had weighed on crypto through June. On Wednesday, Fed Chair Kevin Warsh told the ECB's forum in Sintra that inflation risks had eased in recent weeks, and while he gave no signal on the timing of the next move, markets read the absence of hawkish language as room for a more patient Fed. The bigger catalyst came Thursday, when the June jobs report, published a day early ahead of the Independence Day close, showed just 57,000 new jobs against forecasts near 115,000. Prior months were revised lower, and a temporary World Cup hiring bump flattered even that soft number, leaving underlying growth closer to 17,000. As recently as late June, sticky inflation and firmer data had pushed parts of the Street to pencil in additional hikes this year, so the weak print carried real weight. Short-term Treasury yields fell, gold snapped a multi-week slide, and Bitcoin climbed alongside them.

Oil, which was the main force behind June's inflation scare, stayed quiet even as tensions flickered again. A weekend flare-up in the U.S.-Iran standoff briefly raised doubts about traffic through the Strait of Hormuz, but crude held in the low $70s and the market moved on quickly. Steadier energy prices also support the case that last month's inflation spike has passed its peak. The bounce had a technical element as well, since the prior week's selloff had left positioning light, and the recovery forced short sellers to cover into the move. From here, the June CPI print in mid-July and the Fed's July 28 to 29 meeting will show whether the rate-hike risk behind the selloff is genuinely receding.

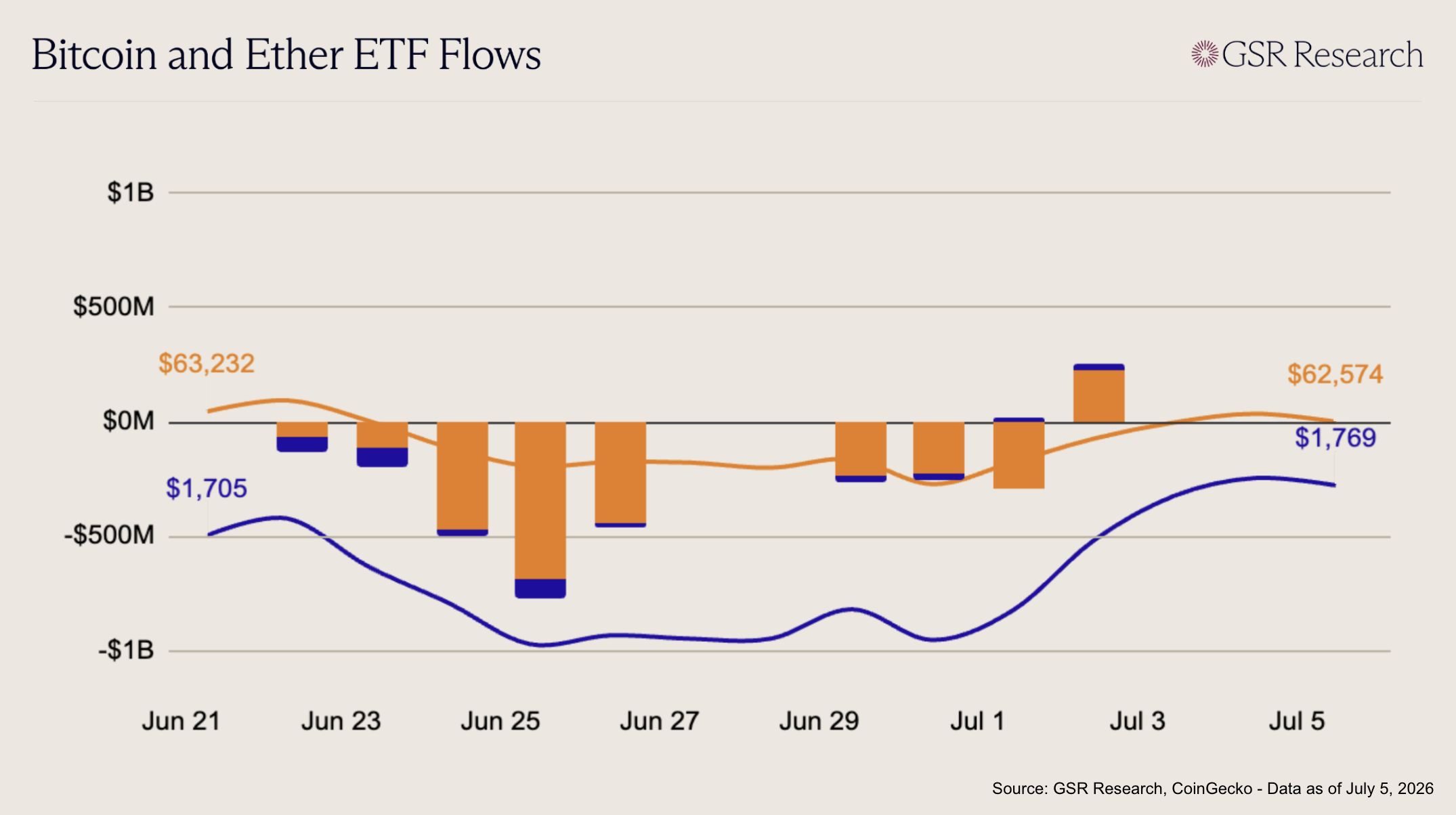

Bitcoin ETFs remained primarily negative this week, but the flow profile showed a clear improvement from the prior week’s heavy redemption wave. The week opened with three consecutive outflow sessions: -$231M on Jun 29, -$223M on Jun 30, and -$296M on Jul 1, driven primarily by continued withdrawals from IBIT, which lost roughly $732M across those first three sessions. FBTC and GBTC also added to the drag on Jul 1, with outflows of -$51M and -$63M, respectively. However, the tone shifted meaningfully on Jul 2, with a strong positive print of +$224M led by FBTC (+$166M) and ARKB (+$92M), while IBIT outflows slowed to -$40M. Across the four trading sessions, BTC ETFs lost roughly $526M, indicating demand remains fragile, but no broad-based institutional de-risking as seen in the prior week.

Ether ETFs showed a more constructive flow profile, breaking from the prior week’s all-negative pattern and finishing modestly negative overall. The week began with outflows on Jun 29 (-$30M) and Jun 30 (-$28M), led mainly by ETHB and ETHA, but flows turned positive into July. ETH ETFs saw a small inflow on Jul 1 (+$15M), followed by a stronger Jul 2 print (+$29M), supported primarily by ETHA and modest contributions from FETH and ETHV. Across the four sessions, ETH ETFs lost roughly -$14M, a significant improvement from the prior week’s $274M drawdown. While the recovery remains tentative, the return of positive flow days suggests that ETH demand is stabilizing faster than BTC, even if institutional appetite has not yet fully normalized.

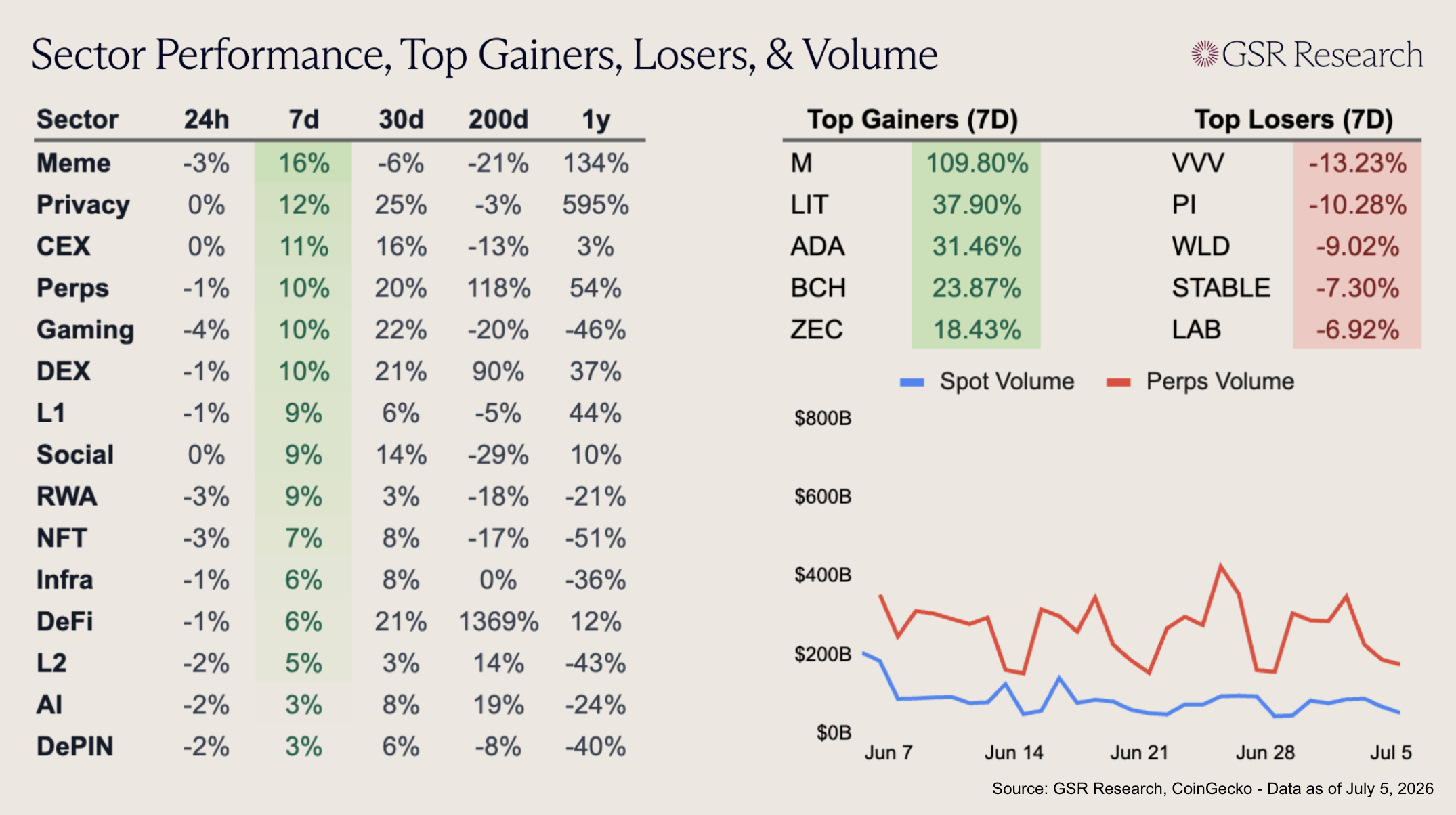

Alts rebounded this week, with every sector finishing in the green and Meme, Privacy, CEX, Perps, Gaming, and DEX all posting double-digit gains. Meme led the board, up 16%, as MemeCore’s M (+109.80%) more than doubled after the Foundation announced a $10m strategic buyback following last week’s sharp crash. Privacy followed, up 12%, as ZEC (+18.43%) recovered ahead of Zcash’s Ironwood upgrade, which is scheduled for later this month and is intended to restore confidence after the Orchard vulnerability disclosure. Perps gained 10%, helped by LIT (+37.90%) after Robinhood Wallet added access to Lighter perpetual futures as part of its Robinhood Chain rollout, while CEX rose 11% as WBT extended its rally on exchange promotions, an expanded FC Barcelona partnership, and rising open interest. L1 also outperformed, up 9%, as ADA (+31.46%) rebounded on renewed wallet growth and BCH (+23.87%) rallied with the broader market recovery.

The loser board was more idiosyncratic and did little to offset the broader sector performance. VVV (-13.23%) was the week’s biggest loser as Venice’s recent $65m raise sparked debate over whether equity-level fundraising benefits token holders, adding to already-negative sentiment around the token structure. PI (-10.28%) also fell after Pi2Day product updates failed to offset weak demand and a large near-term unlock schedule, while WLD (-9.02%) continued to slide despite its upcoming emissions reduction as traders took profits after its prior rebound. STABLE (-7.30%) retraced after a brief volume-led spike, and LAB (-6.92%) gave back some of its recovery as upcoming July unlocks, tokenomics concerns, and lingering transparency questions kept pressure on the name.

This material is provided by GSR (the “Firm”) solely for informational purposes. It is not intended to be advice or a recommendation to buy, sell or hold any investment mentioned. Investors should form their own views in relation to any proposed investment.

It is intended only for sophisticated, institutional investors and does not constitute an offer or commitment, a solicitation of an offer or commitment, or any advice or recommendation, to enter into or conclude any transaction (whether on the terms shown or otherwise), or to provide investment services in any state or country where such an offer or solicitation or provision would be illegal. The Firm is not and does not act as an advisor or fiduciary in providing this material.

This material is not an independent research report, and has not been prepared in accordance with any legal requirements by any regulator (including the FCA, FINRA or CFTC) designed to promote the independence of investment research.

This material is not independent of the Firm’s proprietary interests, which may conflict with the interests of any counterparty of the Firm. The Firm may trade investments discussed in this material for its own account, may trade contrary to the views expressed in this material, and may have positions in other related instruments. The Firm is not subject to any prohibition on dealing ahead of the dissemination of this material.

Information contained herein is based on sources considered to be reliable, but is not guaranteed to be accurate or complete. Any opinions or estimates expressed herein reflect a judgment made by the author(s) as of the date of publication, and are subject to change without notice. The Firm does not plan to update this information.

Trading and investing in digital assets involves significant risks including price volatility and illiquidity and may not be suitable for all investors. The Firm is not liable whatsoever for any direct or consequential loss arising from the use of this material. Copyright of this material belongs to GSR. Neither this material nor any copy thereof may be taken, reproduced or redistributed, directly or indirectly, without prior written permission of GSR.

Please see here for additional Regulatory Legal Notices relevant to US, UK and Singapore.