GSR Weekly Update - June 29th, 2026

BTC: $59,627 (-7.1%) | ETH: $1,568 (-9.3%) | BTC Dom: 55.7% | Global Cap: $2.15T

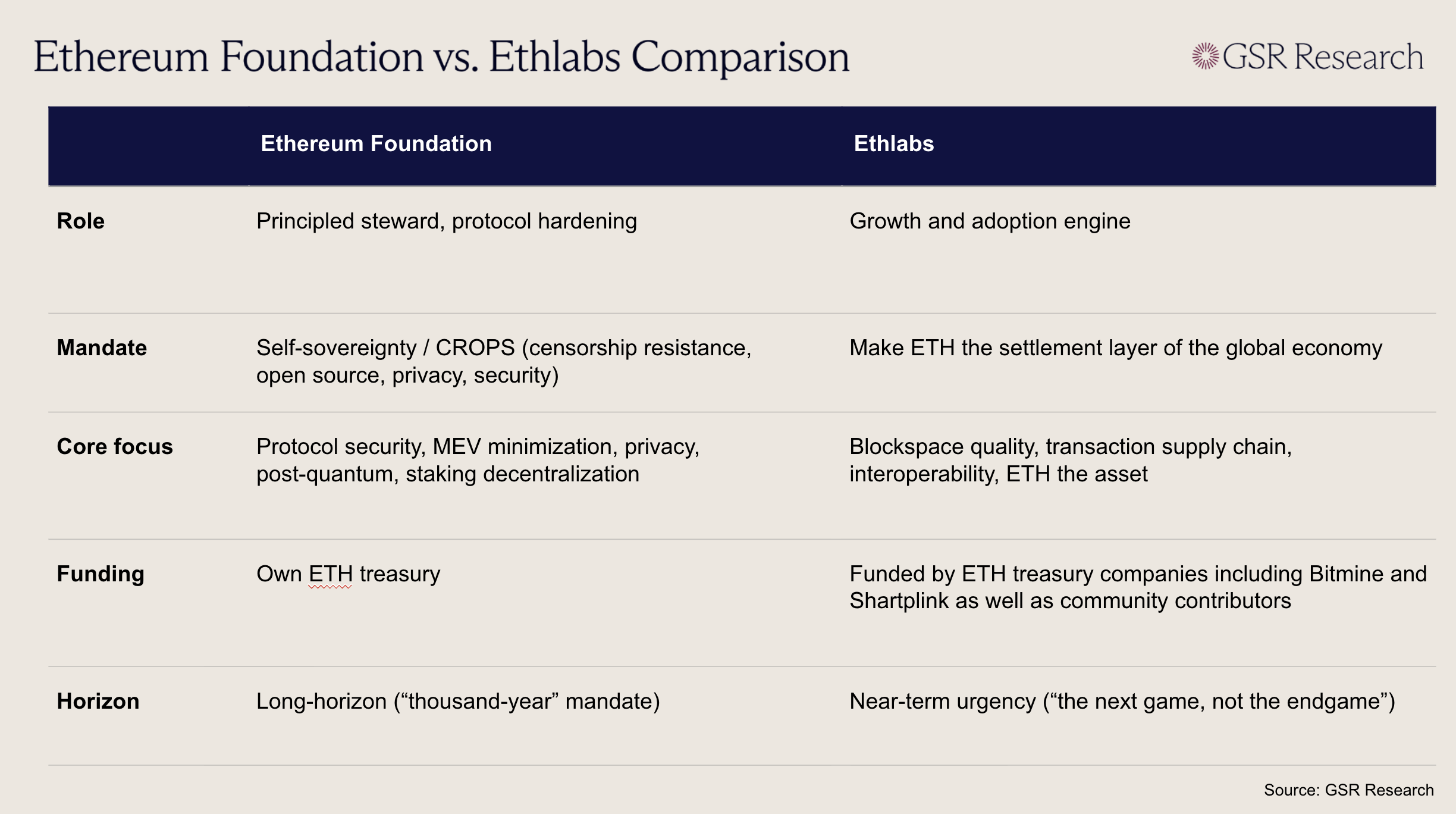

Ethereum's leadership question got two long-awaited answers last week, both on the same day. On June 23, the Ethereum Foundation wrapped up a months-long restructuring, cutting 54 people, around 20% of its staff, and reorganizing the rest into five clusters focused on hardening the protocol's core self-sovereignty properties. Within hours, five researchers who had recently left the EF, among them Barnabé Monnot and Julian Ma, announced Ethlabs, an independent non-profit R&D lab whose stated mission is to make Ethereum the settlement layer of the global economy. Notably, Ethlabs is funded by BitMine and SharpLink, two of the largest ETH treasury companies, alongside Consensys founder Joseph Lubin. Together, the two announcements begin to answer many of the questions we raised in "Ethereum's Identity Crisis."

The picture that emerges is one of specialization. In our previous piece we described an EF narrowing toward credible neutrality and shedding the growth and adoption work it was criticized for neglecting, which the restructuring confirms. The Foundation now states plainly that its protocol work "does not exist to make Ethereum more marketable or focused on short-term interests." Ethlabs picks up much of what the EF set down, concentrating on blockspace quality, the transaction supply chain, and the ETH-centric growth work closest to adoption. Both share the same values, what they call CROPS, but differ in culture and the time horizon they’re focused on, with Monnot framing his work as playing for the next game rather than the thousand-year endgame the EF's mandate implies.

There's a reasonable case to be made that this is healthier than what came before, since one organization trying to be both Ethereum's principled steward and its growth engine was much of what tore the EF apart, and splitting those roles lets each pursue its mandate without undermining the other. The division of labor may give the Ethereum Foundation the necessary space to focus on protecting the values it deeply cares about, while allowing a dedicated development organization to focus on adoption and the growth of ETH the asset itself. The funding sources are telling. As we mentioned in our previous piece, former EF researcher Dankrad Feist had called for a billion-dollar organization economically aligned with Ethereum. A lab bankrolled by treasury companies whose balance sheets rise and fall with ETH is about as close as the ecosystem is likely to get. The EF, encouragingly, seems to welcome the shift, framing a "multi-node future" in which Ethlabs joins a growing roster of independent organizations.

The ecosystem will have to wait and see, however, whether greater fragmentation simply relocates Ethereum's tensions rather than resolving them. That strain, once internal to the EF, now plays out across several organizations. The founders are candid about it, with Monnot invoking the "price of anarchy" of uncoordinated efforts. The sharpest test will be the core protocol roadmap, since Ethlabs means to keep working on core development, not just applications, leaving both organizations overlapping on some of the same areas. The transaction pipeline is a good example, an area the EF treats as a self-sovereignty problem of minimizing toxic MEV, while Ethlabs is likelier to see a question of performance and blockspace quality. Those framings can coexist for now but will not always converge, and the EF has surrendered much of the central authority that once settled such disputes.

Ultimately, while the multi-node model could prove a more resilient and pluralistic way of building Ethereum, it also raises the risk of slower and messier coordination at a time when the protocol can ill afford it. For now the tone across these organizations is collaborative, and we're inclined to read the reshuffle as a sign of the ecosystem maturing rather than fracturing. The real test will come the first time these well-funded, increasingly independent camps seriously disagree on Ethereum's direction.

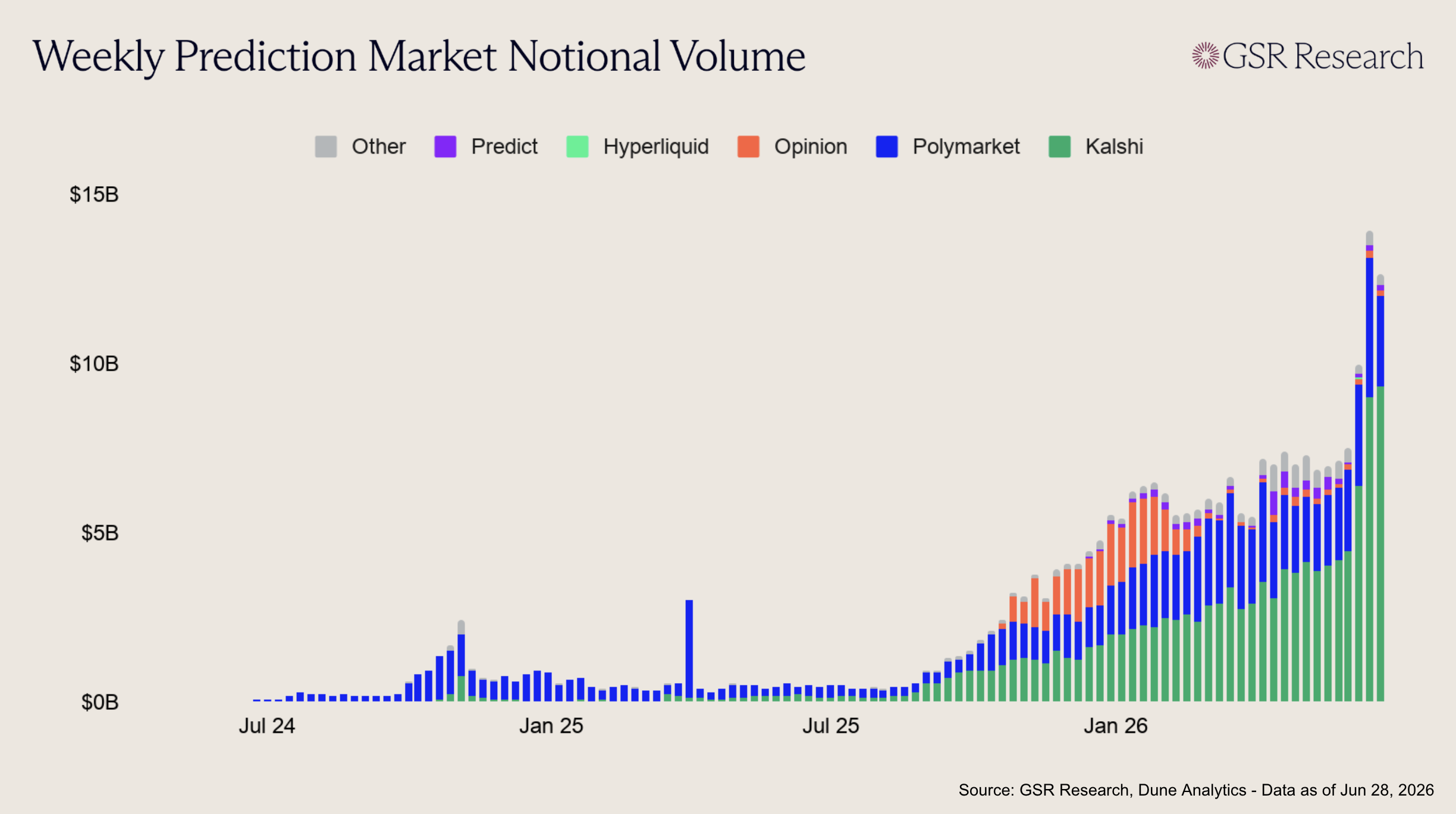

It’s been a landmark week for prediction markets, marked by 3 major developments. Kalshi is reportedly in talks to raise fresh capital at a $40B valuation, nearly double the $22B valuation it reached in its May Series F. At the same time, Mark Zuckerberg has reportedly instructed a small Meta team to build a standalone prediction-market app called Arena. Finally, the sector just posted its 3 largest weeks ever, breaking $10B in notional trading volume within each week. It is now more evident than ever that prediction markets have transcended their identities as crypto-native products to become consumer engagement platforms, regulated exchange infrastructure, and new financial markets for event risk.

According to reports, Arena will be a standalone app modeled after Polymarket and Kalshi, but without real-money wagering at launch. Users would instead bet with points, allowing Meta to test the core behavior while avoiding the regulatory thicket currently surrounding real-money event contracts. The app would be independent from Facebook and Instagram, with Meta reportedly planning to route users toward it from its existing platforms, giving Arena a nearly unbeatable distribution advantage.

Even though Arena is likely to launch as a play-money product, it would train hundreds of millions of users to interact with markets as a social layer. The strategic logic is obvious, as Meta excels at turning attention into structured engagement. Prediction markets are more than gambling-adjacent products, and can act as high-frequency social feeds where users express views on sports, politics, markets, culture, and news in real time. Meta is less concerned about the short-term profits associated with turning their prediction markets into a regulated financial product, and more focused on whether prediction market based interaction is a legitimate consumer format worth owning.

Prediction markets hit $10.8B in weekly trading volume during the week ending June 15th, which was the largest weekly total ever recorded for the category until the following 2 weeks blew it out of the water. During the week of the 22nd, prediction markets would handle over $13.9B in notional trading volume, driven by recent attention around a cluster of tradable events. Coming off the SpaceX IPO, a U.S.-Iran peace deal, and the NBA Finals, prediction market users turned their attention to the World Cup and made nearly 80M transactions in just 7 days. While the record breaking numbers dominated headlines, the more important metric is the change in baseline activity. A year ago, a normal week was roughly $500M and even the busiest weeks remained below $1B. The floor climbed past $1B last fall, past $4B by winter, and has grown into the $6B to $7B range this spring. This underscores the recent records, making them less of a one-off spike and more of a signal that prediction markets continue to exhibit the characteristics of durable trading venues. Open interest also reached a substantial $1.8B during this period.

Kalshi's reported $40B fundraising target suggests that investors are willing to support a higher valuation on the back of these volume gains. Kalshi raised $1B at a $22B valuation in May, led by Coatue, with participation from Sequoia, a16z, IVP, Paradigm, Morgan Stanley, and ARK. In the 2 months that followed, Kalshi hit $100B in lifetime volume, became the first platform to offer regulated perpetuals within the United States, and crossed $1B in open interest.

While milestones are being hit left and right, regulation remains a major caveat for Kalshi. The platform’s growth has been heavily tied to sports-related event contracts, which are still being challenged by states that argue they are effectively unlicensed gambling products. Kalshi recently won an important preliminary ruling in the Third Circuit, when the court held that New Jersey could not enforce state gambling laws against Kalshi’s sports contracts as the Commodity Exchange Act likely preempts state regulation on CFTC-registered designated contract markets. While this is a major victory for Kalshi, it was only a preliminary injunction, not a final nationwide resolution, and parallel cases remain active and ongoing. Given this, Kalshi investors are betting on more than just user growth, as federally regulated event markets will need to survive state-level challenges to justify their valuations.

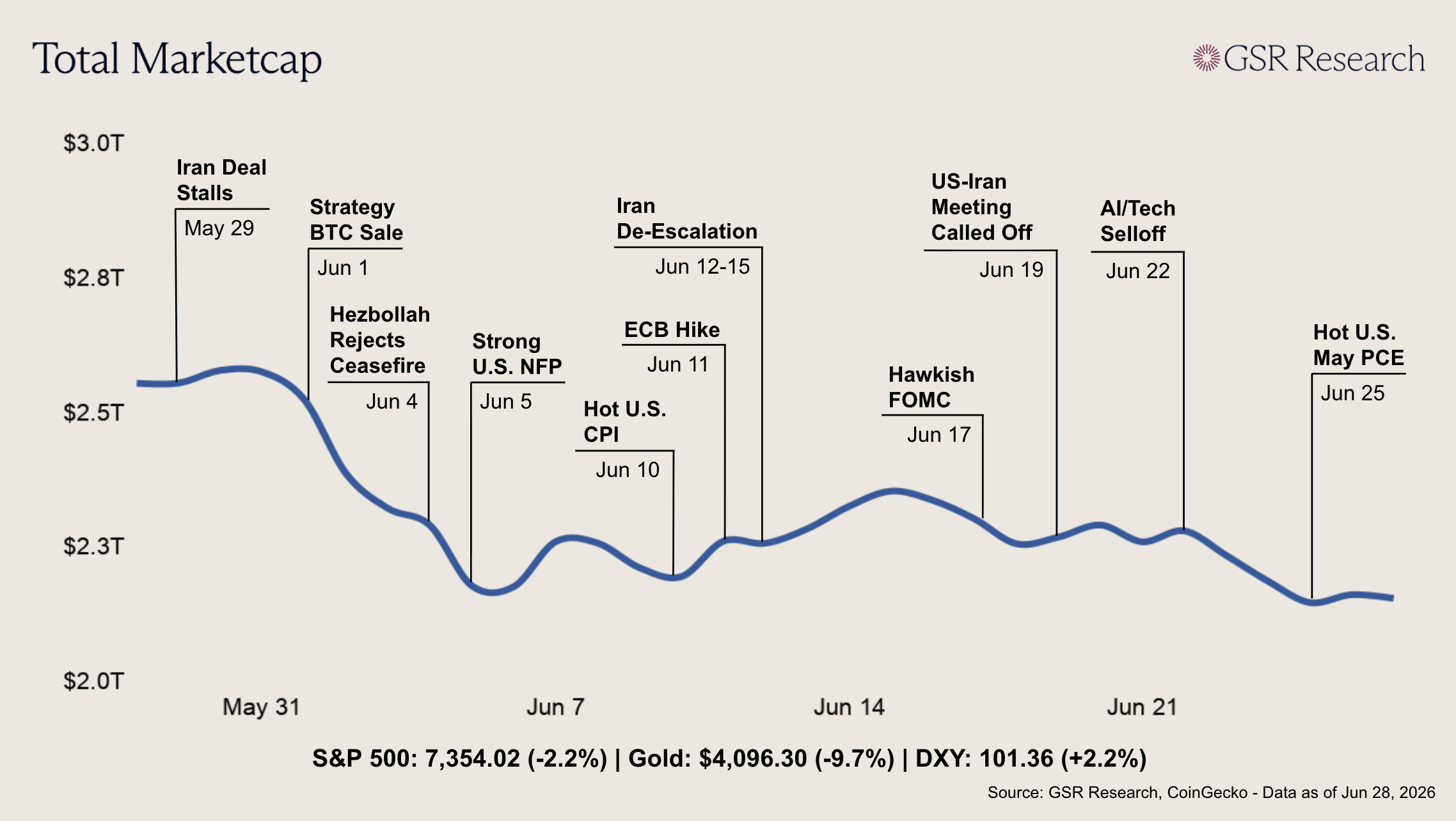

Crypto spent the week grinding steadily lower, as a drop in AI stocks, a hot inflation reading, and a renewed flare-up between the U.S. and Iran all pulled in the same direction. Total market cap opened near $2.28T and worked its way down to around $2.05T, with Bitcoin starting just above $64,000, losing the $60,000 level on Thursday after the inflation data, and falling as far as $58,000, its weakest since late 2024, before steadying near $59,500. ETH had a rougher time, sliding from about $1,723 to roughly $1,565 (down around 9% on the week), and once again digital assets traded as the high-beta end of the risk trade.

The macro backdrop had the biggest impact. The week opened with a heavy selloff in semiconductor and other AI names that dragged the Nasdaq through several losing sessions and spread to global markets, with Korea's Kospi down more than 9%, and crypto fell in step as investors questioned whether the vast spending on AI will pay off. The bigger blow came Thursday, when headline PCE came in at 4.1%, a three-year high, with the core index at 3.4%, and while that was close to expectations, it confirmed inflation has settled above target and reinforced the hawkish turn from Kevin Warsh's first Fed meeting. With rate cuts off the table and markets leaning toward a hike before year-end, the dollar held near a one-year high, yields pushed up, and gold slipped to a multi-month low, all of which weighed on non-yielding assets like Bitcoin. BTC further had an idiosyncratic factor affecting sentiment, with Strategy’s STRC preferred still below par and doubts lingering over whether it can keep paying dividends without selling Bitcoin, a worry that resurfaces whenever the price falls.

Geopolitics stayed in the background, even as the headlines turned alarming. The 60-day U.S.-Iran ceasefire struck only the previous Monday began to unravel, as Iran hit commercial ships in the Strait of Hormuz and the U.S. answered with strikes on Iranian military and drone sites on Friday and Saturday. Markets took it in stride, since oil actually fell to around $72 a barrel, its lowest since February, as tankers resumed transit through the strait. Friday brought one more source of pressure, as a roughly $10.5 billion Bitcoin options expiry landed on a market already running high leverage, with around $1 billion liquidated over the week. With that out of the way, attention turns to next week's U.S. jobs report and whether the Gulf standoff stays contained.

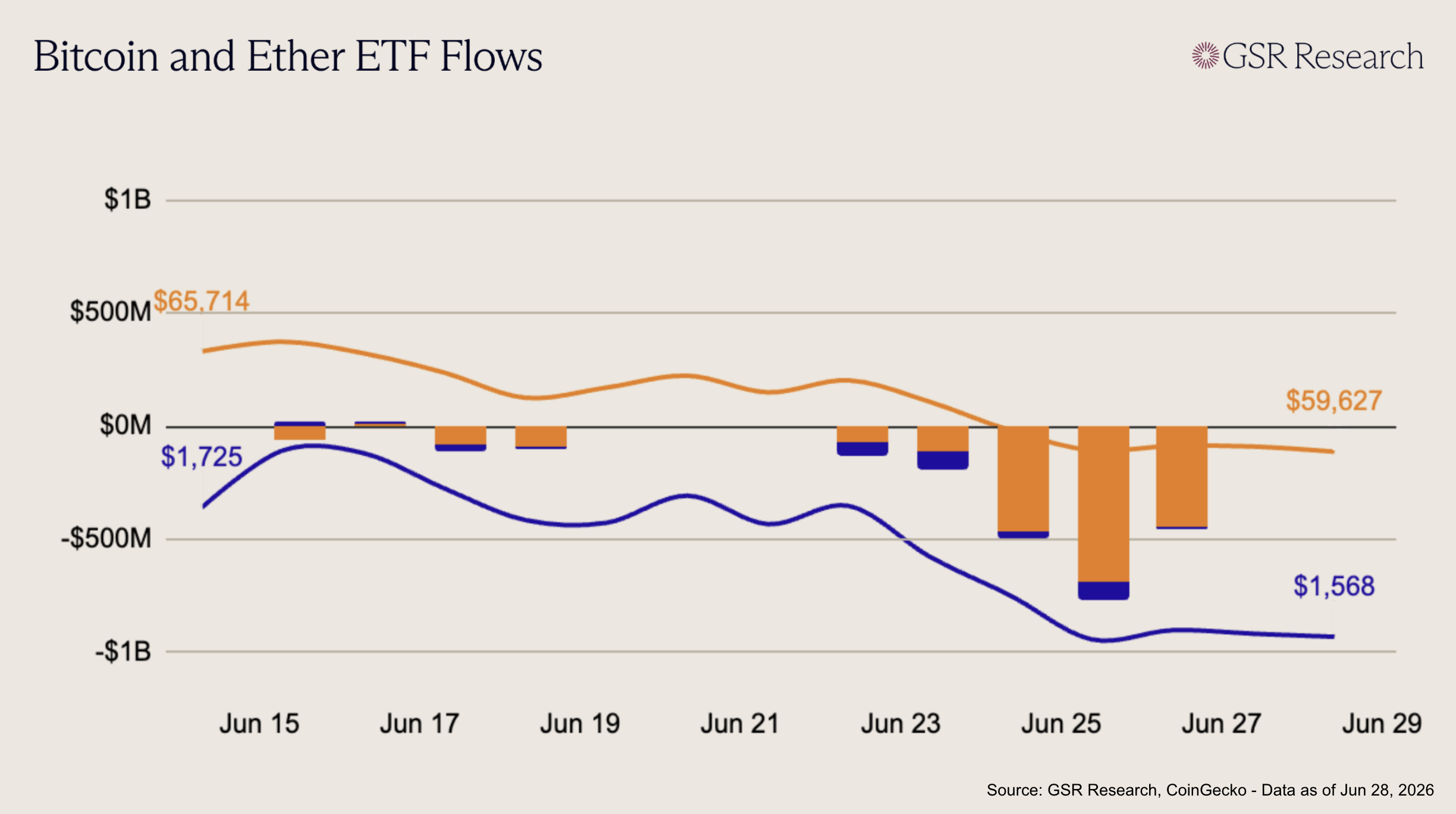

Bitcoin ETFs saw a sharp deterioration this week, with every session closing with net outflows and selling accelerating into the back half. The week opened with moderate redemptions on Jun 22 (-$68M) and Jun 23 (-$114M), but pressure intensified meaningfully on Jun 24 (-$469M), Jun 25 (-$692M), and Jun 26 (-$445M). The drawdown was driven primarily by IBIT, which lost roughly -$1.30B across the five sessions, while FBTC added another -$315M of outflows and GBTC contributed -$135M. Some secondary products provided limited offset, including BTC (+$72M) and MSBT (+$26M), but this was far too small to counter the broad redemption wave. Across the week, BTC ETFs lost roughly -$1.79B, marking a clear re-acceleration in de-risking after the prior week’s partial stabilization.

Ether ETFs followed the same all-negative pattern, with outflows persisting across every session. Redemptions began on Jun 22 (-$66M) and Jun 23 (-$82M), moderated slightly on Jun 24 (-$30M), then deepened again on Jun 25 (-$82M) before easing into Jun 26 (-$13M). Selling was concentrated heavily in ETHA, which lost roughly -$236M across the week, while ETH, ETHE, ETHB, and FETH added smaller drags. Unlike prior weeks where ETH saw brief positive sessions that hinted at stabilization, this week offered no meaningful inflow relief. Across the five sessions, ETH ETFs lost roughly -$274M.

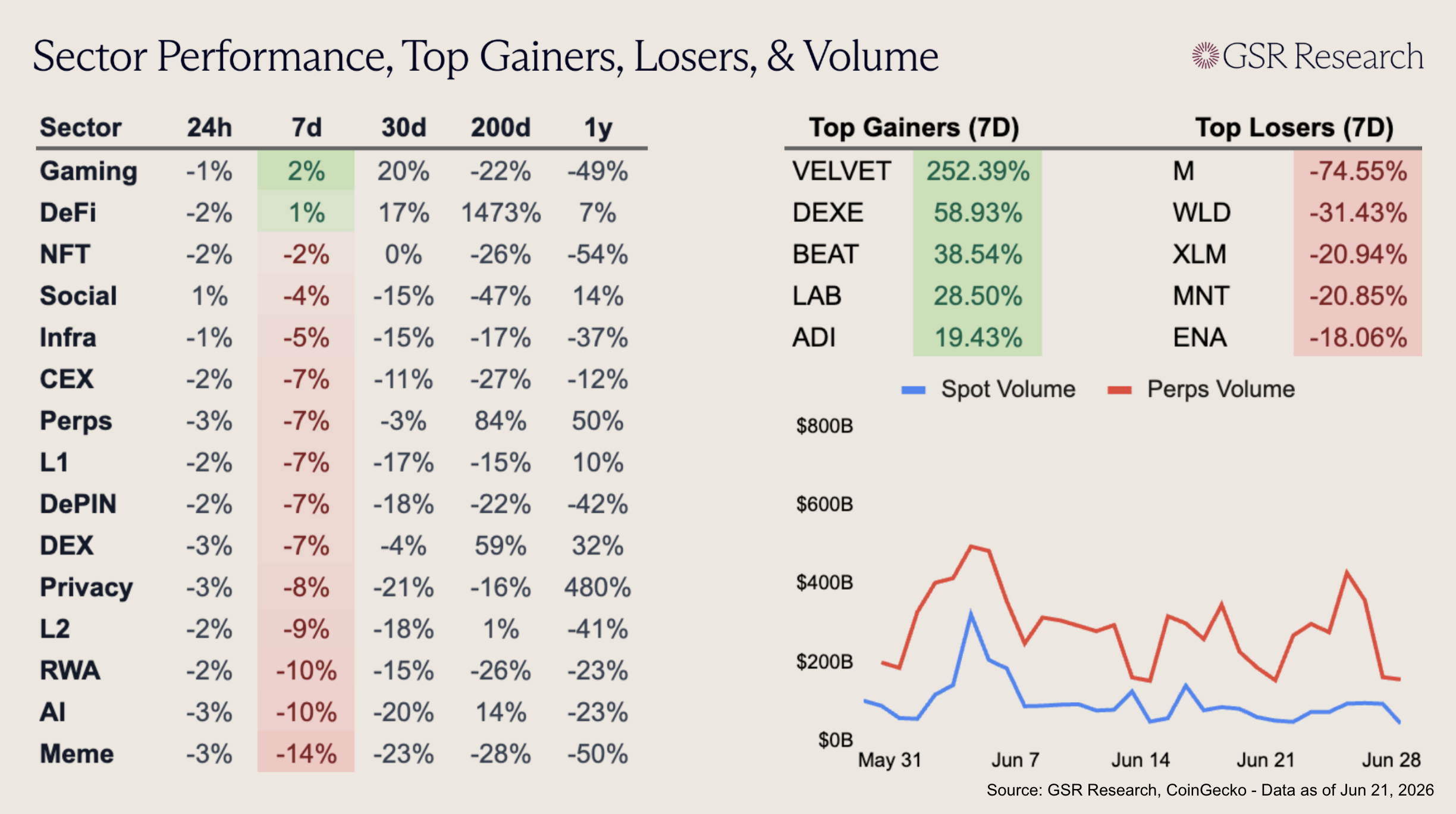

Only Gaming and DeFi finished in the green this week, up 2% and 1%, respectively, as strength remained concentrated in a small group of high-beta names. Gaming was supported by BEAT (+38.54%), which continued to trade on Audiera’s revenue-funded buyback-and-burn narrative after its earlier parabolic move. DeFi held up thanks to AAVE (+19.12%), which rallied after Standard Chartered initiated coverage with a $3,500 2030 price target and reports surfaced that Kraken was exploring a 15% stake in Aave Group. LAB (+28.50%) also contributed, while VELVET (+252.39%) was the week’s biggest gainer, rebounding sharply on renewed demand for its Trade.xyz/pre-IPO market access narrative and a short squeeze after the token’s mid-June drawdown. DEXE (+58.93%) also outperformed on record whale activity and short covering, while ADI (+19.43%) gained as LetsExchange listed the institutional RWA and stablecoin-focused L2 token.

The rest of the board was weak, with Meme (-14%), AI (-10%), and RWA (-10%) the biggest sector laggards. Meme was dragged lower by M (-74.55%), which collapsed without a clear project-level trigger and revived concerns around insider-supported price action after earlier ZachXBT warnings. AI weakness was driven by NEAR (-15.2%) and TAO (-12.6%), with NEAR continuing to fade after its early-June AI rally stalled near resistance and TAO remaining pressured by the Root Reborn governance debate. RWA underperformed as Stellar’s XLM (-17.4%) gave back more of its DTCC-driven rally, with DTC-tokenized assets not expected to be available on Stellar until 1H27. WLD (-31.43%) also sold off sharply as its late-June breakout failed and sentiment remained fragile after Arthur Hayes and Maelstrom publicly exited their positions, while MNT (-20.85%) and ENA (-18.06%) fell despite positive ecosystem headlines as traders weighed liquidity, value capture, and unlock risk.

This material is provided by GSR (the “Firm”) solely for informational purposes. It is not intended to be advice or a recommendation to buy, sell or hold any investment mentioned. Investors should form their own views in relation to any proposed investment.

It is intended only for sophisticated, institutional investors and does not constitute an offer or commitment, a solicitation of an offer or commitment, or any advice or recommendation, to enter into or conclude any transaction (whether on the terms shown or otherwise), or to provide investment services in any state or country where such an offer or solicitation or provision would be illegal. The Firm is not and does not act as an advisor or fiduciary in providing this material.

This material is not an independent research report, and has not been prepared in accordance with any legal requirements by any regulator (including the FCA, FINRA or CFTC) designed to promote the independence of investment research.

This material is not independent of the Firm’s proprietary interests, which may conflict with the interests of any counterparty of the Firm. The Firm may trade investments discussed in this material for its own account, may trade contrary to the views expressed in this material, and may have positions in other related instruments. The Firm is not subject to any prohibition on dealing ahead of the dissemination of this material.

Information contained herein is based on sources considered to be reliable, but is not guaranteed to be accurate or complete. Any opinions or estimates expressed herein reflect a judgment made by the author(s) as of the date of publication, and are subject to change without notice. The Firm does not plan to update this information.

Trading and investing in digital assets involves significant risks including price volatility and illiquidity and may not be suitable for all investors. The Firm is not liable whatsoever for any direct or consequential loss arising from the use of this material. Copyright of this material belongs to GSR. Neither this material nor any copy thereof may be taken, reproduced or redistributed, directly or indirectly, without prior written permission of GSR.

Please see here for additional Regulatory Legal Notices relevant to US, UK and Singapore.